This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Implemented as part of Reg NMS in 2005, the US order protection rule mandates that orders be executed on exchanges that show the best price. Orders are re-routed to other competing venues if it cannot be executed at what is considered the best price. The return of VWAP crossing? The rule change put a stop to exchanges plans in Europe.

My wife and I purchased the business in 2005. Interesting that my father tried to sell the business without a broker (circa 2005) and was very frustrated. We received multiple offers and negotiated the best one. Describe your business? KCS provides varied commercial HVAC services in the Greater Chicagoland area.

For example, if the buyer discovers something in diligence that warrants negotiation of enhanced rights and remedies, it may also negotiate for a separate escrow, apart from the standard general indemnity escrow, to ensure funds are available if any of the enhanced remedies are triggered. Reproduced with permission from Bloomberg Law.

Market Trends: What You Need to Know “Sandbagging” concepts are often the subject of intense negotiation in M&A transactions. Looking at prior ABA studies, the number of deals with pro-sandbagging provisions dropped from a high of 56% in the 2005 study to a low of 29% in the current, 2021 study.

Specifically, including constructive knowledge has steadily increased over the nine ABA studies— from 52% of reviewed deals in the 2005 ABA study to 81% in the most recent 2021 study (down slightly from 86% in the 2019 study). The parties must still negotiate the scope of the seller's knowledge.

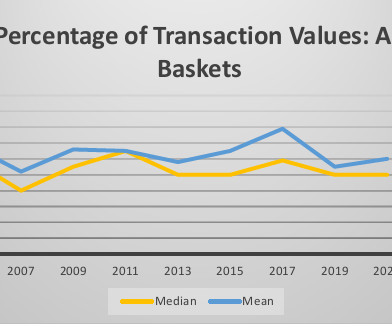

This article examines how buyers and sellers are negotiating indemnity baskets in private company M&A transactions, as shown in the American Bar Association's private target deal points studies. The ABA studies examine purchase agreements of publicly available transactions involving private companies.

The scope and detail of these representations and warranties are often heavily negotiated and tailored to reflect not only the nature of the target and its business, financial condition, and operations, but also the relative negotiating strength of the buyer and seller. Observations. ” Observations. ” Observations. .”

For example, if the buyer discovers something in diligence that warrants negotiation of enhanced rights and remedies, it may also negotiate for a separate escrow, apart from the standard general indemnity escrow, to ensure funds are available if any of the enhanced remedies are triggered.

In addition to the general indemnities, the parties to M&A agreements often negotiate separate “stand-alone” indemnities that cover specific topics outside the general indemnities, usually without reference to an underlying breach of the representations, warranties, or covenants.

Transaction parties negotiated expanded or new representations to address the effect of Covid-19 on the target business, as well as the policies and protocols for dealing with those effects. The Covid-19 virus underscored this aspect of M&A practice.

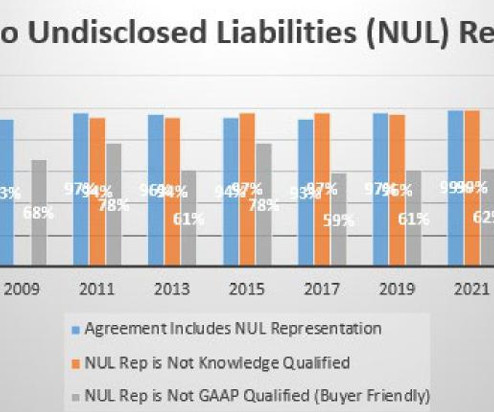

Thus, in deal negotiations, NUL representations are often described – – particularly if broad in scope – – by sellers as redundant or duplicative. Counsel on both sides of an M&A transaction should consider these issues carefully when negotiating an NUL representation. 800-372-1033) [link].

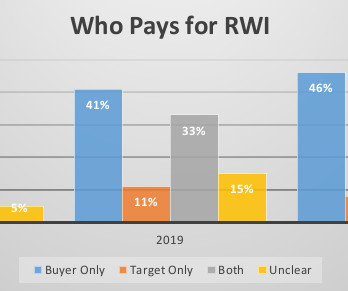

Every other year since 2005 the ABA has released its Private Target Mergers and Acquisitions Deal Points Studies (the “ABA studies”). Market Trends: What You Need to Know RWI is an increasingly important feature of private company merger and acquisition transactions.

From the outset the Bridges and Innovate teams had a good rapport, and we talked a lot together before entering into detailed negotiations. Initially I acquired the business from its founders in 2005 with a partner. We stayed in touch and, following various meetings, both parties were keen to pursue the opportunity.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content