This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you're interested in breaking into finance, check out our , Private Equity Course and , InvestmentBanking Course , which help thousands of candidates land top jobs every year. UBC ranks #7 on our Canadian investmentbanking target school list , earning itself a designation as a Canadian semi-target school.

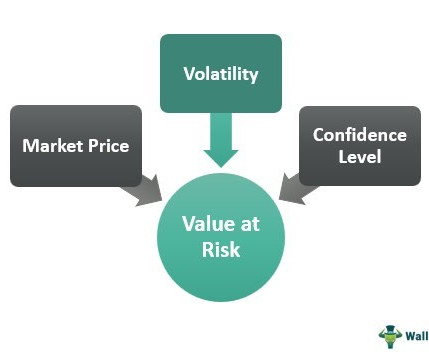

Example: During the 2008 Financial Crisis, many financial models based on parametric VaR underpredicted potential losses, causing significant challenges. If you're interested in breaking into finance, check out our , Private Equity Course and , InvestmentBanking Course , which help thousands of candidates land top jobs every year.

According to Coalition Greenwich, the top dozen investmentbanks offering prime services saw revenues rise to a record $20.4 The bank also highlights to us how “as a global multi-asset class prime broker, we are structured to deliver the widest range of services regardless of strategy type or product complexity”. “At

The interest rate swap works as an amazing portfoliomanagement tool. In the case of fund managers who want to work on a long-duration strategy, the long-dated interest rate swaps help increase the portfolio’s overall duration. This was when many fixed-income players started actively participating in the market.

The mean-variance optimization model is used to calculate the expected return and risk (as standard deviation) of a portfolio, based on the returns and risks of the individual assets it contains, and the correlations among them. Criticisms and Limitations of Modern Portfolio Theory MPT is not without its critics.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content