This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Therefore, the process of portfoliomanagement involves balancing these two factors based on an investor's financial goals and risk tolerance. For instance, the 2008 recession hit financial companies hard, but technology companies like Apple and Amazon weathered the storm relatively well.

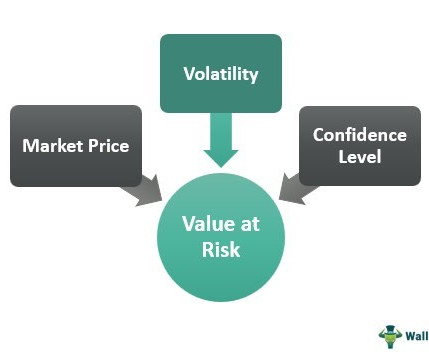

Example: During the 2008 Financial Crisis, many financial models based on parametric VaR underpredicted potential losses, causing significant challenges. As a Regulatory Tool: After the 2008 crisis, regulatory bodies in both the U.S. Parametric VaR Uses statistical techniques based on the normal distribution of returns.

For example, a portfolio has cash flows that match put options in the market. Replicating Portfolio Approach Explained Replicating portfolio involves the pooling of assets in a manner that allows portfoliomanagers to easily hedge the risks of these assets and balance the risk-return of the target asset.

UBC also offers the elite PortfolioManagement Foundation (PMF) program, which gives students practical investing experience and dedicated alumni support. We examined profiles of professionals who worked in investment banking between 2008 and 2023. We have created a U.S.

During the 2008 financial crisis , put options (which give the holder the right to sell at a specific price) on mortgage-backed securities and major stock indexes increased in value dramatically as the market plummeted. Role of Derivatives in PortfolioManagement Derivatives play a crucial role in modern portfoliomanagement.

The requirements align the US with Basel III standards which were agreed following the 2008 crisis with capital, leverage and liquidity requirements rolled out in the ensuing years, as the latest reforms look to end the reliance on internal models in the US for estimating risk and introduce standardised frameworks.

We started to see a little bit of what I imagined was going to be the evolution of that market, which is a number of strong portfoliomanagers from those multi manager platforms coming out, launching their own funds. And we’ve seen some significant launches this year in that space.

The interest rate swap works as an amazing portfoliomanagement tool. In the case of fund managers who want to work on a long-duration strategy, the long-dated interest rate swaps help increase the portfolio’s overall duration. This was when many fixed-income players started actively participating in the market.

The mean-variance optimization model is used to calculate the expected return and risk (as standard deviation) of a portfolio, based on the returns and risks of the individual assets it contains, and the correlations among them. Conclusion In the intricate world of finance, understanding and leveraging effective strategies is crucial.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content