This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Instead, a combination of rising interest rates, inflation, soaring energy prices and geopolitical tensions have hit hedge funds, and subsequently the riskmanagement practices of prime brokers. With the larger banks focusing on larger AUMs and higher revenue clients, there is a battle for new launches and emerging managers.

For example, the Great Recession of 2008–2009 saw significant drops in GDP, widespread unemployment, and a substantial decrease in consumer spending. This phase typically involves increased market volatility and heightened investment risk. GDP decreases, unemployment rates rise, and consumer spending slows.

The advent of derivatives in the 1970s marked a significant milestone in global finance, offering a structured riskmanagement approach and fostering efficient price discovery. These complex instruments enable investors to hedge risks, speculate on future price movements, and exploit arbitrage opportunities.

Commercial Banks: These cater to businesses, providing loans, treasury, and cash management services. The profit-making strategies differ across these banks. Subtracting the $50 paid to you, the bank makes a net profit of $350. Dodd-Frank Wall Street Reform and Consumer Protection Act: Introduced after the 2008 crisis, this U.S.

Headwinds in finance are conditions or events that can impede economic growth or reduce the profitability of an investment. During the 2008 global financial crisis , many sectors, from real estate to banking, experienced significant challenges. Competition intensifies, often leading to reduced prices and profit margins.

it’s starting to feel a lot like 2008. I explained the reasons for Silicon Valley Bank’s failure in last week’s article : incompetent riskmanagement, massive losses on HTM securities, and a run on the bank that created the need to sell securities at a loss and get cash to cover the withdrawals. And the answer was “U.S.

For example, the 2008 financial crisis can be examined through the lens of Natural Law. The Dodd-Frank Wall Street Reform and , Consumer Protection Act passed in the aftermath of the 2008 financial crisis, is a prime example of Positive Law. RiskManagement Natural Law emphasizes understanding and respecting universal truths.

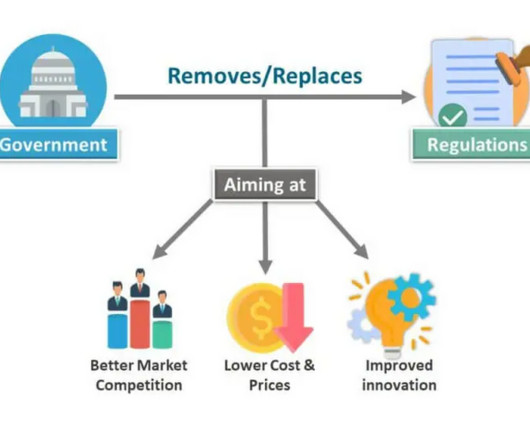

However, it's also spotlighted the need for a balanced approach to regulation, as evidenced by the financial crisis of 2007-2008 , which underscored the potential dangers of overly lax regulatory frameworks. Consumer protection: There's a risk that deregulation might prioritize industry profits over consumer interests.

, Short Selling is an investment strategy where investors sell borrowed shares, anticipating the price will drop and they can buy them back at a lower cost, making a profit from the difference. Short selling can be a profitable strategy, but it's inherently risky as potential losses are theoretically unlimited.

Leveraging derivatives to capture the best results at a given point in time may help portfolio managers achieve closely matching outcomes, in addition to performance monitoring, effective riskmanagement , risk diversification , etc. Insurance companies use this tool for riskmanagement and planning.

It should be noted that in a market which has experienced provider exits, the shedding of less profitable clients and with looming increased capital requirements – don’t underestimate the lure of staying power and commitment to the business. It’s not all sunshine and rainbows in the prime brokerage world, however.

Interest rate swaps are riskmanagement tools, allowing parties to hedge against interest rate fluctuations and achieve desired cash flow structures. It proves to be a prerequisite for analyzing the business’s strength, profitability, & scope for betterment. read more using an interest rate swap. read more.

Over the past two decades, several critical financial market regulations have been implemented globally, particularly in response to the 2008 Global Financial Crisis (GFC). The years following 2008’s GFC experienced continued financial regulatory reform.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content