This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

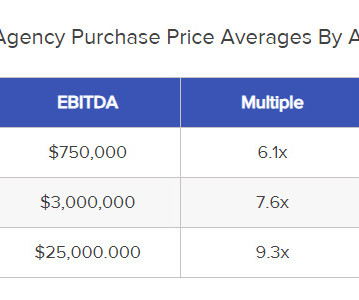

Selecting the Valuation Method Insurance agency valuations typically occur in one of the following four methodologies EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization): A calculation of an insurance agency's profitability calculated by subtracting taxes and operating expenses from its overall revenue.

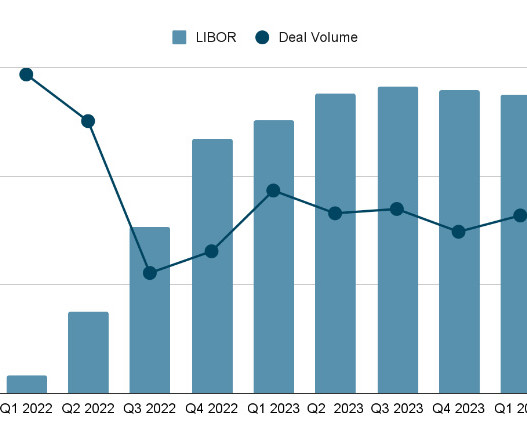

Last year's data saw PE firms acting as buyers in ~90% of all transactions. As long as buyers face higher interest rates, sellers should expect a prolonged deal process contending with complex capital structures and equity-based negotiations. Whereas 2022 saw equity making up nearly 17.5% as of H1 2024.

In addition, third-party M&A institutions like S&P Global Data or Statista can provide more generalized data. Ask an Advisor Not only will an experienced M&A advisor have a better idea of how your insurance agency will be valued, they can also help you negotiate an even better payout when you take it to market.

In deals with the highest earnout, business owners turn to a specialized M&A advisory firm to handle negotiations and oversee valuations. Founders Michael Fletcher and Al Sica are two of the industry's leading dealmakers who have advised on over $16 billion in insurance agency and brokerage transactions since 2014.

Factors Affecting EBITDA Because EBITDA refers to a general assessment of an insurance agency’s profitability, factors affecting it are those that relate to the agency's bottom line. S&P Global Data, PitchBook, PWC) or through M&A indexes provided by M&A advisory firms.

It also opens the door for savvy buyers to talk them out of millions of dollars when it comes time for negotiations. How much higher, however, depends on the marketing process, due diligence, and negotiations as handled by your M&A advisor.

This is why it’s so important to have an experienced partner on your team handling the valuation and all associated negotiations. What qualifies as a non-recurring expense when calculating the adjusted EBITDA for insurance agencies is often enthusiastically negotiated by your team and the buyer’s.

For example, knowing how much equity the buyer has utilized in previous deals can give you a good idea of what to expect when you finally sit down at the negotiating table. Keep a close eye on earnouts, post-closing employment contracts, and how well a buyer supports the seller following the finalized negotiations.

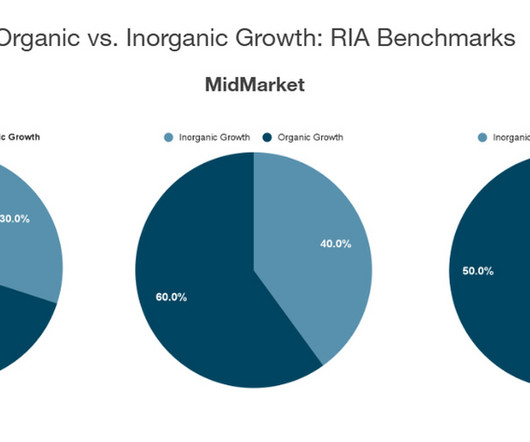

As the Baby Boomer Generation enter their golden years, it's very likely that we will see increased valuations in the coming decade as more and more people seek retirement planning services. We see no reason to believe this trend will change, but robo-advisors will remain on the periphery, pushing RIAs to greater degrees of service.

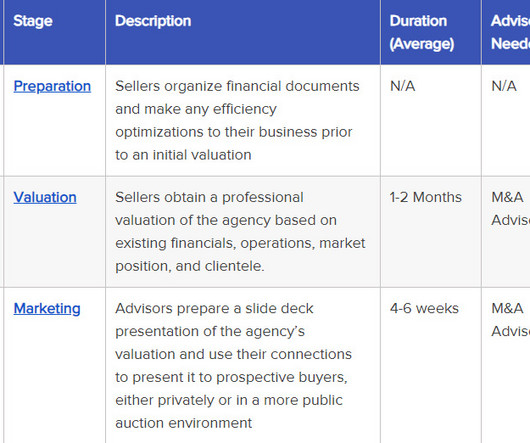

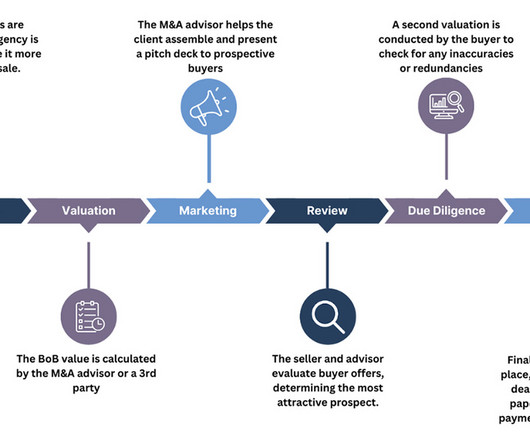

Changes in the Valuation Process Valuation is the first formal step in the M&A deal process, taking place once the seller has gathered all their preliminary documents and made any necessary changes to the company's internal structure to make it more profitable. Think Long-Term.

This means that they often lack the specialized industry knowledge to effectively negotiate your deal. Consult data sources like S&P Global data to get an idea of a firm’s activity within the industry. Are you meeting the firm’s principals?

Due Diligence, Final Negotiations, & Closing Due diligence essentially takes the form of a secondary valuation the buyer conducts to uncover any potential risks in your company that have not already been discussed. Your attorney, in particular, should take the lead on final negotiations. Learn more at , ,, SicaFletcher.com.

Risks When Selling an Insurance Agency Book of Business Once it’s been valued, marketed, and reviewed, the final steps in selling an insurance agency book of business are the final negotiations and closing. Financing options offered by the seller, based on the book's performance over time. Much rarer in BoB sales.

With larger physician networks and access to specialist’s hospitals also gain negotiating leverage with insurers and can participate in alternative payment models, such as capitated and bundled payments, through vertical integration. Is Healthcare’s M&A Trend Softening? 2014, March 25). 2014, September 12).

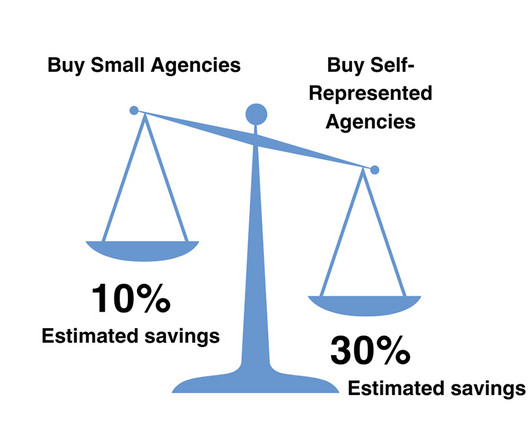

Get an Advisor Having observed the trend of buyers actively looking for self-represented agencies and brokerages, it's important – now more than ever – to ensure you retain adequate representation before taking your company to market. The following sections detail our team’s advice for agency owners considering a transaction.

This has been especially relevant over the last 18 months, with macroeconomic pressures making deals more difficult to negotiate. Founders Michael Fletcher and Al Sica are two of the industry's leading dealmakers who have advised on over $16 billion in insurance agency and brokerage transactions since 2014.

PE firms rely on leveraged buyouts (LBOs) for the lion's share of their deals, which often involve using the acquired company’s assets as collateral to insure the loan used to purchase it. The following subsections detail those strategies as well as actionable insights and suggestions on what to do in the coming year(s).

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content