This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At what point do “discussions” with a friendly merger party become “negotiations” that are required to be publicly disclosed under the tender offer rules in response to a hostile bid? Allergan maintained that no such disclosure needed to be made because it would have jeopardized the deal.

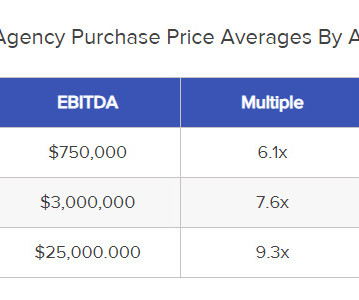

It also opens the door for savvy buyers to talk them out of millions of dollars when it comes time for negotiations. How much higher, however, depends on the marketing process, due diligence, and negotiations as handled by your M&A advisor. For example, let’s take a look at the value of the same small example RIA in today’s market.

The rise of founder-led, venture capital-backed companies in recent years has coincided with a surge of companies implementing dual-class share structures in connection with their initial public offerings. In a small number of cases, a class of common stock is offered to the public that has no voting rights at all.

new technology, active competitors, regulatory/compliance changes) can affect the market shares of all participants. Founders Michael Fletcher and Al Sica are two of the industry's leading dealmakers who have advised on over $16 billion in insurance agency and brokerage transactions since 2014. Interest Rates.

2014) (“MFW”) and its progeny applies in a non- MFW scenario (i.e., Between October 5 th and 11 th , the special committee supervised a price negotiation with iSubscribed, which resulted in an increased offer of $3.68 per share would likely be acceptable to the Company’s board. per share, and the eventual merger price of $3.68

Inter-family loans, unpaid salaries, or shared equity structures may complicate future sales. Changes in Final Negotiations Following the buyer’s due diligence, their teams will meet with your advisors to discuss the contract’s final terms. Family-specific financial arrangements. Think Long-Term. Learn more at SicaFletcher.com.

2459 (2014). Agreements negotiated by labor organizations in the United States are enforced by the National Labor Relations Board (NLRB), which offers alternative dispute resolution as an option for resolving conflicts. Employees should be trained to refrain from opening suspicious emails or sharing passwords.

In September 2014, the European Commission approved CAL-101 as a first-line treatment in combination with another drug for patients with chronic lymphocytic leukemia (CLL) who have a genetic abnormality with respect to chemo-immunotherapy (a sub-population of patients with CLL). for a Hematologic Cancer Indication.” Avoid terms of art.

With larger physician networks and access to specialist’s hospitals also gain negotiating leverage with insurers and can participate in alternative payment models, such as capitated and bundled payments, through vertical integration. 2014, March 25). 2014, September 12). Is Healthcare’s M&A Trend Softening?

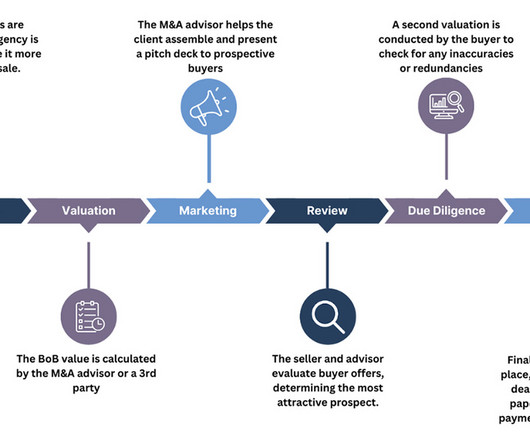

Consider Digitization Focus on Your Unique Selling Points (USP) Improve Client Retention Vet Prospective Clients & Carriers The Steps of Selling an Insurance Agency Book of Business Selling an insurance agency book of business shares all of the major steps of any M&A transaction and often involves the same team members.

PE firms rely on leveraged buyouts (LBOs) for the lion's share of their deals, which often involve using the acquired company’s assets as collateral to insure the loan used to purchase it. Ultimately, this paved the way for PE firms to take an increasingly larger share of the insurance M&A market starting about a decade ago.

It focuses on developing genome sequencing technologies and has raised 106 million in equities since its inception in 2014. They have a bespoke negotiation process, customising equity shares according to each companys specific circumstances and contributions of its founders. per cent), with all of the companies being acquired.

In the first half of 2016, plaintiffs filed suit in only 64% of public deals valued over $100 million, down from 84% in 2015 and over 90% from 2009 to 2014. Negotiating Anti-Reliance Language. As a result, the overall incidence of M&A litigation has declined, particularly in Delaware. The Trump Effect. Appraisal Risks Factor High.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content