This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sica | Fletcher is pleased to announce that we’ve topped the S&P Global rankings for the third consecutive year. In 2019, we closed the largest number of transactions ever for our firm, reflecting the increasingly robust M&A market for insurance brokers driven mainly by privateequity sponsored brokerages.

PrivateEquity-backed buyers retain their stronghold on M&A activity with 87% of Q1 2024 Index transactions, even as the interest rate environment and strategic acquisitions continue to slow down a handful of platforms. billion in insurance agency and brokerage transactions since 2014. Learn more at SicaFletcher.com.

For the better part of the last decade, physician practices have seen a wave of consolidation by hospitals and privateequity with 2018 being no exception [1]. In fact, acquisitions by hospitals and privateequity in provider services broke records last year according to Bain & Co’s 2019 global healthcare report.

PrivateEquity-backed buyers maintain a dominant position in M&A activity, accounting for 87% of YTD June 2024 Index transactions. The firm was founded in 2014 by Michael Fletcher and Al Sica, two of the industry's leading dealmakers who have advised on over $17.5

PrivateEquity-backed buyers maintain a dominant position in M&A activity, accounting for 87% of YTD June 2024 Index transactions. The firm was founded in 2014 by Michael Fletcher and Al Sica, two of the industry's leading dealmakers who have advised on over $17.5

PrivateEquity-backed firms have dominated the space consistently for several years in terms of the number of transactions and represent over 89% of SF Index transactions during 2023. . ### About Sica | Fletcher: Sica | Fletcher is a strategic and financial advisory firm focused exclusively on the insurance industry.

The quarterly report emphasizes the ever-growing presence of privateequity-backed firms in insurance brokerage M&A. About 91% of SF Index transactions were executed by privateequity-backed firms through YTD June 2023, continuing the trend observed year over year. Learn more at , SicaFletcher.com.

I started my career in 2014 as an investment banking analyst in an oil & gas coverage group. In June of 2014, when I finished training and first hit the desk, the price of oil was $105 per barrel (West Texas Intermediate, or WTI). investment banking, privateequity , VC, etc.) and how our process works.

The late 2010s, however, saw an explosion of privateequity activity that has dramatically increased that pool from 5 to more than 50. Privateequity firms make up approximately 92% of the current buyer pool, making them the most common type of buyer that sellers will likely run into.

Founded in 2014, they have consistently ranked at the top of the S&P Global Data's rankings for investment banks, totaling an average of 100 deals per year. Their size also provides a hidden value for prospective clients in that it ensures that the firm's principals touch on every deal that they handle.

PrivateEquity-backed firms have dominated the space consistently for several years in terms of the number of transactions and represent over 89% of SF Index transactions during YTD September 2023. Broadstreet leads the group in number of deals at 45, followed by Hub International at 42 and Assured Partners at 34.

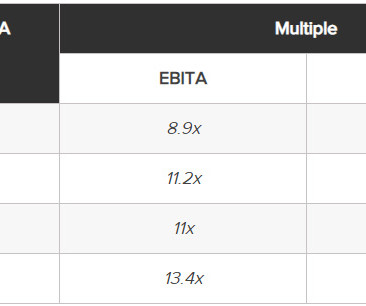

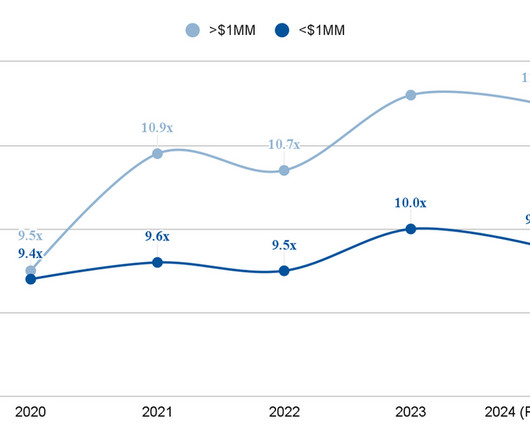

EBITDA Multiples for Insurance Agencies, 2018-2024 (Projected) M&A Deal Volume for Insurance Agencies, 2018-2024 (Projected) *S&P Global Data taken from ,,, “Insurance Brokers and Servicers Sector View 2024” The most important news this data offers is that insurance M&A is not actually in the tailspin that many “experts” claim it to be.

Equity Over Time in Insurance M&A Transactions Modern capital structures, however, have also changed significantly in the last several years, including various types and classes for categorizing equity, all of which determine who gets paid in what order. Changes in the buyer pool.

Founders Michael Fletcher and Al Sica are two of the industry's leading dealmakers who have advised on over $16 billion in insurance agency and brokerage transactions since 2014. According to S&P Global, Sica | Fletcher ranked as the #1 advisor to the insurance industry for 2017-2023 YTD in terms of total deals advised on.

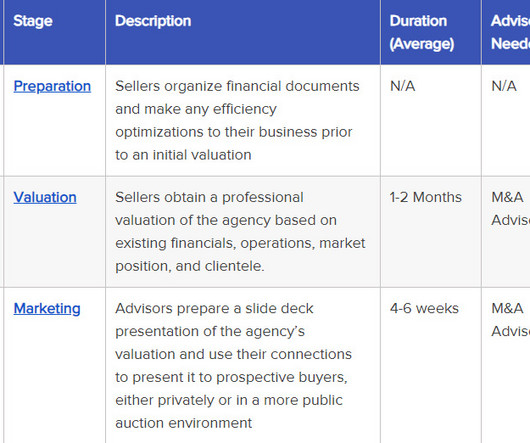

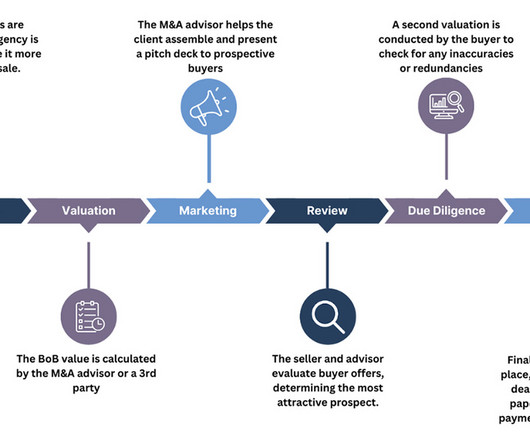

privateequity firms, investment banks, individual investors). For example, a privateequity firm LOI might state that it plans to roll up your agency with others and resell them all several years later. Valuation For a more in-depth examination of the valuation process, consult our previous article on the subject here.

The History of PrivateEquity in Insurance One of the primary forces differentiating the insurance M&A market in 2024 from those of decades past is the presence and dominance of privateequity (PE) firms in the buyer space.

Common Insurance Agency Book of Business Payment Structures Insurance agency M&A transactions are typically going to happen through a financial buyer, which is almost always a privateequity company. Financing options offered by the seller, based on the book's performance over time. Much rarer in BoB sales.

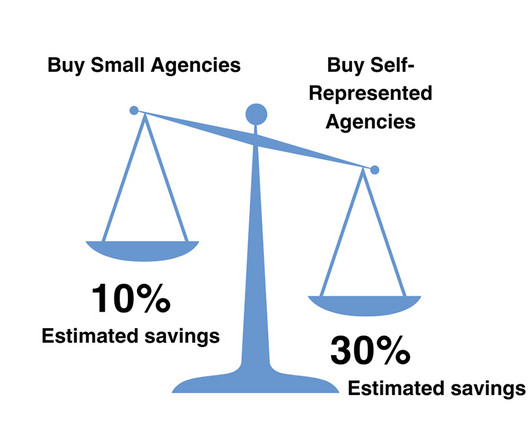

For the most part, the market consists of many small to midsize agencies that make prime candidates for roll-up deals, especially as privateequity firms have played an increasingly larger role in the market over the last decade. There are surprisingly few large insurance brokerages. Learn more at , ,, SicaFletcher.com.

EQUITY Prior to the advent of COVID-19, equity markets were poised to extend a decade-long surge that saw a 270% increase in the number of privateequity deals between the low point of 2009 through 2019 [2]. The initial shock gave both buyers and sellers cold feet, resulting in a general market freeze.

Being in your country’s top ~5% of earners will make a FAR bigger difference than fancy strategies, day trading, or finding the occasional meme coin that goes up by 100x. Investing Principles: Why a High Income Trumps Everything Else Between 2009 and 2014, I did not have a traditional portfolio via a brokerage firm.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content