This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

Insurance agency valuation is a critical component of running an M&A deal, but executing this multi-step process well requires a great deal of specialized education and experience. In addition, getting the valuation process started demands a hefty bill and entails poring over extensive documentation for several weeks.

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

This differentiation helps identify a company’s profitabilityProfitabilityProfitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs. It is measured using specific ratios such as gross profit margin, EBITDA, and net profit margin.

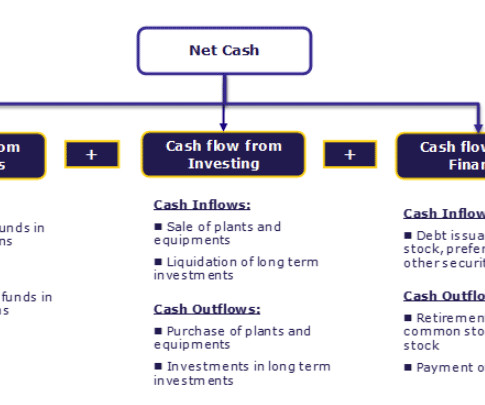

Determine EBITDA Earnings before interest, taxes, depreciation, and amortization (EBITDA) is used as a measure of the profitability of an insurance agency while adding back interest, taxes, depreciation, and amortization - all of which will vary depending on the circumstances of the new owner.

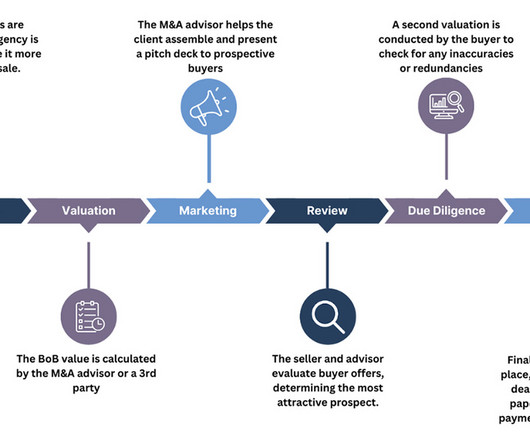

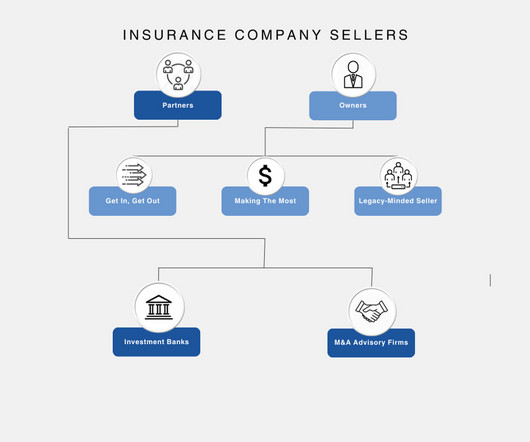

Who Performs A Valuation? RIA valuations are typically performed by one of three parties: The M&A Advisor A Third-Party Specialist The Seller Themselves Although many sellers attempt to perform their own valuations, we strongly recommend against this.

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. The table below contains a few recommendations to make your business more profitable. Why Sell Just the Book?

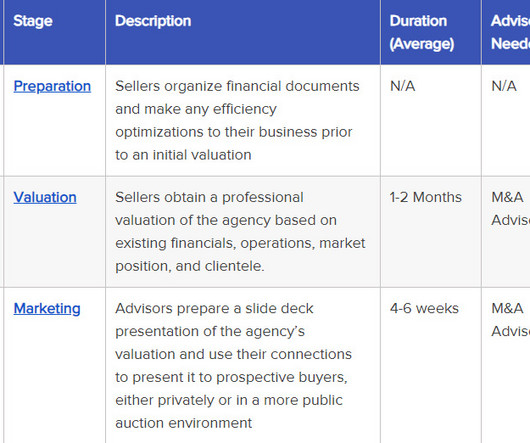

While we’ve already written extensively on the process of insurance agency valuation , the following sections focus on what to look for in the earliest stages of considering a sale - in other words, what deciding factors to look for to determine whether you should sell your agency. What Documents Do I Need? Indicators of Scalability.

Buyers want to acquire your agency and intend to sell it after several years for a profit, typically as part of a larger portfolio of purchased companies (e.g., Valuation For a more in-depth examination of the valuation process, consult our previous article on the subject here. Valuation is a process in and of itself.

essentially boils down to three major steps: Determine your insurance agency’s EBITDA Determine the standard valuation multiple for an agency of your size Multiply your EBITDA by the multiple to determine your expected payout (i.e., Interest, taxes, depreciation, and amortization are then added to this number.

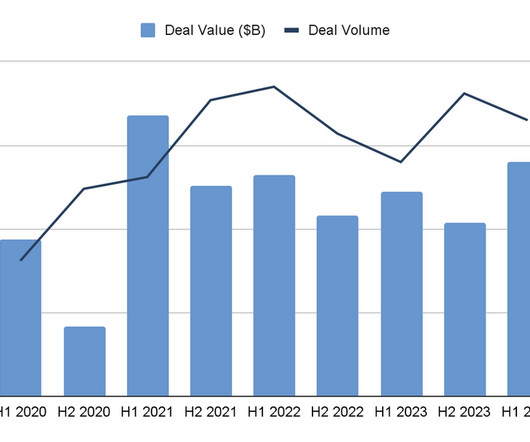

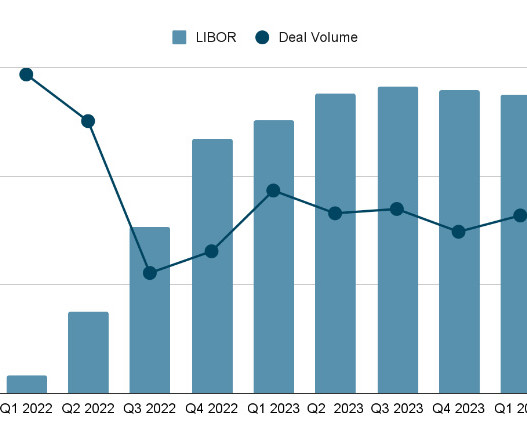

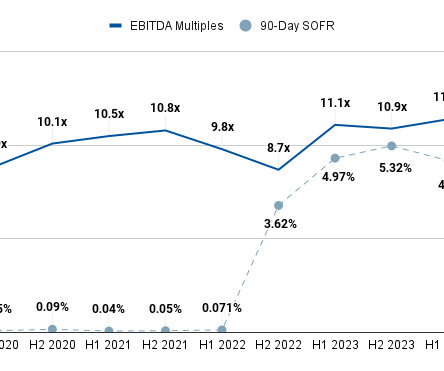

Starting in H2 2022, the insurance M&A market has seen a notably difficult 18-month period, afflicted with high interest rates, lowered deal volumes, and lowered valuations. If they do, then we can expect to see valuations and, by extent, EBITDA multiples for insurance agencies rise. Learn more at , ,, SicaFletcher.com.

Changes in the Valuation Process Valuation is the first formal step in the M&A deal process, taking place once the seller has gathered all their preliminary documents and made any necessary changes to the company's internal structure to make it more profitable. Family-specific financial arrangements.

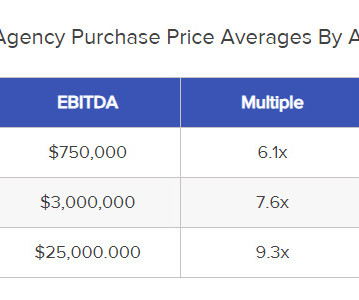

Insurance M&A Deal Valuation, 2024 Starting out in 2024, EBITDA and revenue multiples are in a good place, experiencing modest YoY growth despite the economic downturn of the last 18 months. In deals with the highest earnout, business owners turn to a specialized M&A advisory firm to handle negotiations and oversee valuations.

Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest. Effectively, this means that, for the first time , buyers are purchasing insurance agencies at a loss for themselves in order to capitalize on what they see as profitable long-term investments.

The network has invested in 43 healthcare and life sciences start-ups since its inception in 2014, investing a total of £14m. The network is part of MedCity, a not-for-profit organisation set up by the Mayor of London in 2014 to encourage growth and investment in the sector.

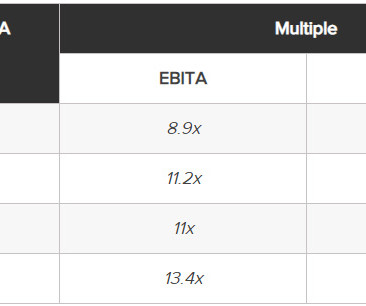

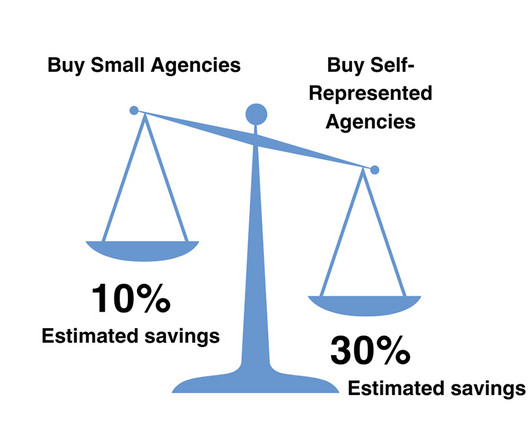

With such a high level of competition, they face the double-edged sword of higher overall valuations vs. a relatively smaller initial payout as equity becomes an increasingly larger percentage of buyer offers. This has led to very high valuation multiples (~11.5x Learn more at SicaFletcher.com.

Insurance Brokerage M&A Multiples, 2024 The following sections offer additional context for the data in the table above by outlining the current insurance brokerage M&A market and providing insights from our team to make selling your brokerage smoother and more profitable once you get started. Learn more at SicaFletcher.com.

Although the seller’s goal does impact how each M&A transaction is conducted, it does not affect whether or not they need to improve their brokerage prior to the initial valuation. boost your profits, cut your bottom line), doing so with a brokerage requires paying special attention to the diversity of your policy portfolio.

However, the specific question here is who profits from these features, not which users benefit the most. Again, these are all perfectly viable and profitable businesses, but they don’t have the same margin or valuation profile as true SaaS companies. vs. how much money it makes.

Your agency valuation will play a large role in influencing how buyers perceive your agency’s worth. Take time before bringing your agency to market to optimize your daily operations, thus increasing the likelihood of a higher valuation. Pay close attention to the multiple being offered. Learn more at SicaFletcher.com.

Despite investment in the first half of 2023 dropping to £4.6bn from 2022’s £10.8bn as a result of rising interest rates, high inflation, a decrease in valuations and geopolitical tensions globally, UK fintechs are still attracting more VC investment than all other EMEA fintechs combined, with a significant percentage coming from US investors.

In 2014-2015, we decided to take our impact to the next level. Their growth – getting new investors and earning higher valuations, expanding their footprint and stakeholders – gives us valuable confirmation that our approach is working. We understand that the positive impact of our investments goes well beyond profit margins.

Christopher Majdi, Director of Valuation & FMV Services at Premier, Inc. While hospitals can profit from alignment with physician practices, some argue that physician practices also benefit from this relationship given the greater resources and income generating opportunities available to them [17]. 2014, March 25).

According to Reuters , consumer/retail deals accounted for 15% of private equity deal volume between ~2004 and ~2014 but fell to only 7% between ~2014 and ~2024. The closest comparable here is probably industrials private equity , based on the deal volume and accounting/valuation skills required. are unprofitable.

Most facilities are owned by private sector businesses while other community hospitals are either non-profit, for-profit, or government owned. How do business valuations differ in Healthcare and across its subsectors? However, Medtronic’s valuation is significantly lower than the sector average (Collins).

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content