This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

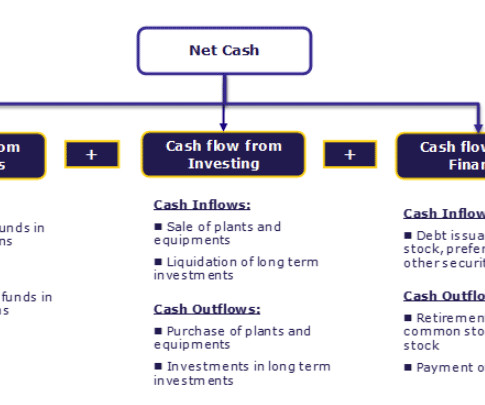

The investing activities comprise the long-term asset purchase or sale. Add to it all the incoming cash from various sources like cash sale of goods or services, proceeds from the sale of assets or investments, the funds acquired by the issue of shares or through bank loans, etc. read more like salaries, taxes, etc.

According to Nasdaq , in 2015, SPACs made up approximately 12% of the IPO market, but by 2020, that number had risen to approximately 53%. SPACs are predicted to be an even higher percentage of the 2021 market share, with SPACs representing 79% of the January IPOs.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Voting agreements in public M&A transactions.

3) Revenue Growth – Besides ticket and merchandise sales, sports teams can grow revenue with broadcast/licensing deals, partnerships, and newer routes like augmented reality (AR) / virtual reality (VR) experiences and e-gaming. The Top Sports Private Equity Firms The list of sports PE firms was short in 2015, but it has exploded over time.

Private equity slowed but not stopped by financing environment Despite record amounts of dry powder accumulating for sponsors, high financing costs, persistent valuation gaps and a closed tech IPO market led to a significant decrease in private equity M&A activity in 2023. Despite some isolated bright spots – such as Thoma Bravo’s $10.7

Traditional terminal exit routes for private equity-backed companies are to larger strategic acquirers (often public companies) and IPOs, where a private company becomes publicly traded. It is also likely that IPOs will come to PPM, perhaps first to those specialties with the largest assets (e.g.,

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content