This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For the better part of the last decade, physician practices have seen a wave of consolidation by hospitals and private equity with 2018 being no exception [1]. In fact, acquisitions by hospitals and private equity in provider services broke records last year according to Bain & Co’s 2019 global healthcare report.

EBITDA Multiples for Insurance Agencies, 2018-2024 (Projected) M&A Deal Volume for Insurance Agencies, 2018-2024 (Projected) *S&P Global Data taken from ,,, “Insurance Brokers and Servicers Sector View 2024” The most important news this data offers is that insurance M&A is not actually in the tailspin that many “experts” claim it to be.

The S&P 500 has recently traded near 4800, close to its record at the end of 2021. And Navigant Consulting, a well-known publicly traded company, finished going private in 2019, after first selling its Disputes, Forensics and Legal Technology practice to Ankura in 2018, and then selling its remaining divisions to Guidehouse.

They might have separate teams for specific strategies or markets, but everything is run under a single Profit & Loss statement (P&L). There are very few real “requirements” besides the single PM / single P&L one above and the standard Limited Partner / General Partner structure that all hedge funds use.

Private equity firms continue to drive transaction pace and value. Aggregate Number of Transactions The best source of data we have found for the number of insurance agent and broker M&A transactions for a given period is data aggregated by S&P Market Intelligence on announced transactions.

Now, we are excited to make the SEG SaaS Index available as an interactive tool that will enable software executives, private equity companies, venture capitalists, and others to view and sort key metrics for all companies in the Index and study historical trends. Click here to get started.

Now, we are excited to make the SEG SaaS Index available as an interactive tool that will enable software executives, private equity companies, venture capitalists, and others to view and sort key metrics for all companies in the Index and study historical trends. Click here to get started.

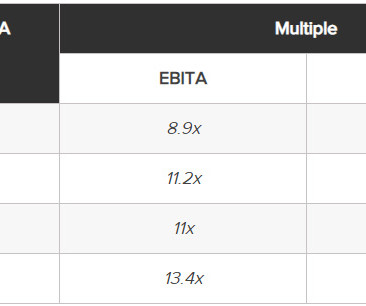

Revenue Revenue multiples are a distant second option for insurance agency valuations, making up about 5% of the recorded deals we observed between 2018 and 2024. Our data has shown a 30% increase in deals that feature equity as a larger portion of the seller payout since 2018. So, what should insurance agencies expect in 2024?

The Seven Indicators Stock Price Momentum : The S&P 500 versus its 125-day moving average. For instance, the 2018 U.S. If you're interested in breaking into finance, check out our Private Equity Course and Investment Banking Course , which help thousands of candidates land top jobs every year.

We discuss with Mark the process of becoming an anti-racist and anti- sexist org anization and how RBF embed s DEI initiatives i nto its culture , its hiring practices, its investing, its endowment, and its partnerships, an d how those can serve as ex ample s to other institutions. MA That’s an interesting question.

While adoption is widespread in equities other asset classes such as fixed income have been slower to adopt these systems given the nuances of the workflows and liquidity landscapes in these markets. They’re typically used in equities given that this asset class trades on exchange unlike fixed income and some foreign exchange assets.

2023’s much-discussed downturn in mergers & acquisitions – with global M&A volume and value down 6% and 17%, respectively, from 2022 – was largely driven by the slowdown in the tech sector, with global tech M&A volumes down 51% year over year, while other sectors saw marked increases. [1] billion leading the pack.

S&P reported that the number of insurance brokerage transactions closed in 2020 slightly exceeded those in 2019. Sica | Fletcher closed 125 transactions in 2020 (our best year ever, and again, , leading the league tables ) in comparison with 92 in 2019 and 79 in 2018.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content