This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

After a SPAC frenzy in 2020 which then slowed by 2022, SPACs seem to appear to be popular again; Dunaevsky says these transactions still offer a good alternative to IPOs when conducted correctly, and that she expects a. By: Lowenstein Sandler LLP

Founded in 2019, Okay participated in Y Combinator’s Winter 2020 cohort before going on to raise a total of $6.6 They were u sually companies in the pre-IPO phase with hundreds to thousands of engineers where the manager wanted to start tracking what others are doing, and looking for tools to help with decision-making.”

One could likely dedicate an entire history book to all that has happened in 2020. This new world has forced many new adaptations and innovations, but what has this meant for those in VC who circled themselves around new trends and innovations long before 2020? According to analysis from PwC and CB Insights, Q2 2020 showed a 9.6%

Market volatility, a low interest rate environment and disillusionment with the IPO process, have made SPACs an attractive alternative for private companies looking to go public in recent months. According to Odeon Capital Group research, as of December 2, 2020, 210 SPAC IPOs had been completed representing gross proceeds of ~$72 billion.

In that environment, very few firms sought IPOs, and there was a major slowdown in overall exits, whether private or public. And will that mean that some of the privately held management consulting firms or other professional services companies will choose an IPO this year? But those companies have been public for more than 20 years.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders.

SPAC activity continued to slow in the first half of 2022, a sharp decline from the number of deals and IPOs in the same period in 2021. In addition, only 69 SPAC IPOs were priced in the first half of 2022, compared to 362 SPAC IPOs priced in the first half of 2021. [1]. Key Points.

The proposal arrives in the context of calls from various corners, including from SEC Chair Gary Gensler and former Acting Corp Fin Director John Coates, to treat SPACs as an alternative method of conducting an IPO under the SEC’s policy framework. (See See this PubCo post , this PubCo post and this PubCo post.) See this PubCo post.)

There were more SPAC IPOs in 2020 than traditional IPOs. The market for SPAC IPOs and so-called “de-SPAC” transactions, by which private companies become public companies by combining with a SPAC, is as hot as ever.

Chan joined HKEX as head of listing in January 2020 and currently serves as co-chief operating officer of HKEX. Prior to that, she served as the head of IPO transactions, listing division, HKEX from 2007 to 2010.

In the UK, a downward trend for tech IPOs continued, with volumes falling to their lowest level last year in a decade. Global tech exits — through both IPOs and M&A — remain stagnant, with $21bn in value so far this year, compared to a peak of $177bn in 2020 and $166bn in 2021.

When Covid shut down the IPO market in 2020, SPACs were the only game in town, and the market went from sleepy to red hot to burnt out. While many market observers have written their obituaries for SPACs, Ellenoff said that there will always be a need for IPO alternatives and that SPACs and those who invest in them are here to stay.

I’ll cover all those points here, but I want to start with some context first: A Long Time Ago in a Stock Market Far, Far Away To understand the premise of Dumb Money , you need to return to late 2020 and early 2021, which now seem like a lifetime ago: There was a global pandemic. I wrote many articles about it. Dumb Money has none of this.

is the increased frequency at which SPAC IPOs are occurring. As reflected in Chart 1 , 102 SPAC IPOs have been announced this year as of September 18, 2020—almost double the number of SPAC IPOs in all of last year (and more than double the number of SPAC IPOs in 2018). SPAC vs. IPO. Fewer Redemptions.

The data supports this theory, as during the period from March 13, 2020 (when the US declared Covid-19 a national emergency) until August 21, 2020, Zoom had a negative beta of -0.39. since its IPO in April 2019 until the end of 2019. This was a dramatic change from its pre-pandemic days when it had a positive beta of 1.81

SC Ventures Founded: 2018 Sector focus: Fintech Ticket size: $1m – $10m Current investments: 22 Exits: N/A Bio: SC Ventures by Standard Chartered invests in disruptive fintech across Series B to pre-IPO stages which can be integrated into the company’s product and service offerings.

billion IPO last year, which was led by JPMorgan Securities LLC; Goldman, Sachs & Co.; GE), rising to general counsel of GE Capital before joining Angelo Gordon in 2020, while TPG’s Berenson was senior counsel for litigation and legal policy at GE before moving to TPG in 2017. Eisenberg, Parness and Weil’s Michael B.

According to Nasdaq , in 2015, SPACs made up approximately 12% of the IPO market, but by 2020, that number had risen to approximately 53%. SPACs are predicted to be an even higher percentage of the 2021 market share, with SPACs representing 79% of the January IPOs.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements.

Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank. During the hold period, the private equity firm can improve operations, management structure, and financial strategies to optimize the business.

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. More than 50% of the SPACs that went public in 2020 and 2021 are incorporated in Delaware, giving particular significance to SPAC litigation filed in Delaware courts.

It is interested in companies at pre-Series A through to pre-IPO stage. ITV AdVentures Founded: 2020 Sector focus: Digital, consumer Ticket size: Up to £5m in advertising Current investments: 9 Exits: N/A Bio: ITV AdVentures offers TV advertising to high-growth digital-first companies at all stages of development.

Since their split at the start of 2020, Europe and the UK have been focused on emerging as the victor of Brexit with home of the European financial hub to be in either the City of London or Paris. Unlike the US and Asia, Europe has produced stagnant volumes year on year, driven by several macroeconomic factors and a suffering IPO market.

Although 2022 saw a general decline in M&A activity in the life sciences industry compared to 2021’s frenetic pace (when deal volume was up 52% from 2020 ), life sciences deal flow in 2022 on balance remained strong despite the headwinds. Let’s dig in.

For growth-stage companies, you will see plenty of equity offerings: IPOs , SPACs , PIPEs, and follow-on issuances. A good example is the 2020 – 2021 period, when SPAC activity went vertical, and plenty of renewable energy companies used SPACs to go public.

3) Aquis Stock Exchange Aquis Stock Exchange , run by NEX, allows businesses to raise capital through Initial Public Offerings (IPOs). >See >See also: Here’s how you undertake an IPO in the UK in the best way It’s a stock market which provides primary and secondary markets for equity and debt products.

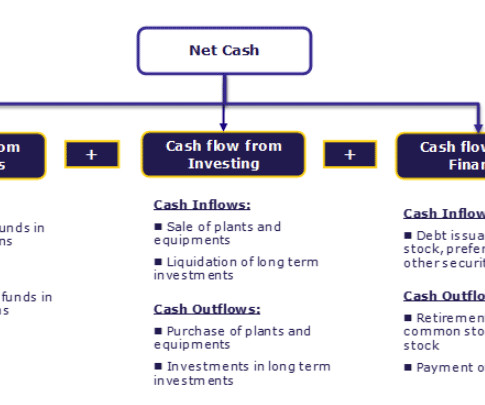

Thus, we can say that by the end of the accounting year 2020-2021, ABC Inc. In 2015, Box came up with its IPO. Before its IPO, Private Equity Investors financed Box Inc. Example #1 ABC Inc. is left with $1,774,000 as cash and cash equivalents. Now, moving on to a real-world example, let us discuss the cash flows of Box Inc.

It’s a tech business that we finally launched in the middle of the Covid pandemic in September 2020. When I left parliament, I decided to focus on investing in and mentoring pre-revenue businesses primarily run by young entrepreneurs. The business has grown spectacularly since then and is an 80-fold (to date) return on my initial investment.

Indeed, tech start-ups in London alone raised a record $26bn (£19bn) in funding in 2021, more than double the total in 2020. of investments each year: Typically 8-10 companies per year (based on 2019 and year to date 2020) Previous companies invested in: 165, including ContactEngine, Improbable and Sprout.ai. Contact: enquiries@sep.co.uk

While we continue to absorb and understand the worldwide pandemic shockwaves of 2020, trying to encapsulate the vicissitudes of the past year in an annual recap is daunting. 1] The robust momentum in the second half of the year nearly made up for early pandemic effects as 2020 deal value was down only 6.6% A Tale of Two Years.

trillion during 2021 – an increase of 71% compared to 2020 – and accounted for 20% of the $5.9 For industry experts questioning whether the SPAC momentum that gained traction in 2020 could be sustained, 2021 provided a mixed response. Tech M&A surged to a staggering $1.1 trillion(!) in the year’s global M&A deal value.

If 2019 was the year of life sciences mega-deals, 2020 was the year of COVID-19, as the global pandemic permeated every aspect of the dealmaking landscape, with the life sciences sector being no exception. Also impacted was Thermo Fisher’s attempted acquisition of Qiagen through a tender offer launched on March 3, 2020.

However, if it can keep the team’s revenue growing at 15 – 25% per year and exit at a 4x revenue multiple, it could still earn a ~15% IRR over 5 years: It’s unclear how well this will work because Arctos was only founded in 2020.

The start of 2025 has seen an uptick in special purpose acquisition company (SPAC) initial public offering (IPO) activity in the United States as the broader market grapples with political and economic volatility and traditional IPOs remain on hold.

Private equity slowed but not stopped by financing environment Despite record amounts of dry powder accumulating for sponsors, high financing costs, persistent valuation gaps and a closed tech IPO market led to a significant decrease in private equity M&A activity in 2023. Despite some isolated bright spots – such as Thoma Bravo’s $10.7

Although the COVID-19 pandemic that defined 2020 continued to shape much of the life sciences industry in 2021, the way that it did was markedly different. A healthy 90 biopharma M&A transactions were announced in 2021 (compared to 69 in 2020 and 70 in 2019, the most transactions since 2016). As we noted in our 2020 year?end

Beginning in 2020, there was a wave of announcements for private equity firms entering the car wash industry. Public Markets: It is possible that a few of the car wash platforms with strong growth and financial performance pursue an initial public offering (IPO).

Growth Equity Interview Questions: Markets & Investments These questions could span a huge range because they could ask you about anything from the current fundraising environment to the IPO and M&A markets to specific markets their portfolio companies operate in. Q: Pitch me a growth company that we should invest in.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content