This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

” Laplanche is referring to the BNPL-style product that Upgrade launched in October 2021, which lets users pay down their debt over six to 36 months with a fixed interest rate. million users to the platform, and comes as Upgrade weighs an IPO. The purchase of Uplift effectively doubles Upgrade’s customer base, adding 3.3

However, one common point across all the verticals is that IPOs are not common because there aren’t that many publicly traded sports teams, stadiums, or arenas. SPAC IPOs for esports companies were “hot” for a short period in 2021, but they seem to have died off by now.

In the UK, a downward trend for tech IPOs continued, with volumes falling to their lowest level last year in a decade. Global tech exits — through both IPOs and M&A — remain stagnant, with $21bn in value so far this year, compared to a peak of $177bn in 2020 and $166bn in 2021.

Despite everyone’s efforts in 2021, including the rollout of vaccines and varying rounds of lockdowns and work-from-home mandates, a true “return to normal” for M&A dealmakers was foiled anew by COVID-19 and its variants. trillion during 2021 – an increase of 71% compared to 2020 – and accounted for 20% of the $5.9

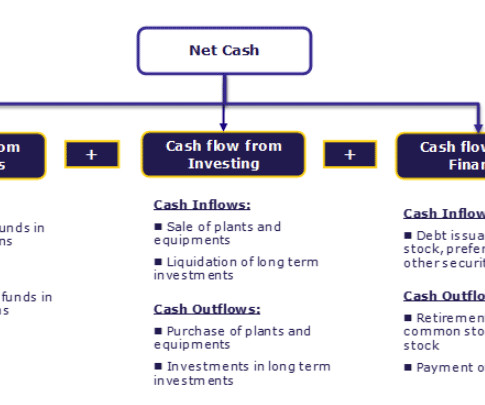

Statement of Cash Flows Definition A Statement of Cash Flow is an accounting document that tracks the incoming and outgoing cash and cash equivalents from a business. It helps identify the availability of liquid funds with the organization in a particular accounting period.

Others would counter that growth equity’s rapid ascent was mostly due to the easy money that persisted between 2008 and 2021. This style is about purchasing minority stakes in cash-flow-negative-but-high-growth companies that want to scale and eventually go public or sell (think: Uber or Airbnb before their IPOs).

According to Nasdaq , in 2015, SPACs made up approximately 12% of the IPO market, but by 2020, that number had risen to approximately 53%. SPACs are predicted to be an even higher percentage of the 2021 market share, with SPACs representing 79% of the January IPOs.

Helpfully, the SBA issued a procedural notice in October 2020 outlining what constitutes a “change of ownership,” allowing deal parties to structure a transaction to eliminate the need for SBA consent by submitting a loan forgiveness application and placing the loan proceeds into an escrow account established by the PPP lender in advance of closing.

Underwriting Services Merchant banks also provide underwriting services for initial public offerings (IPOs), private placements, follow-on public offerings (FPOs) and rights issues. It is an accounting and banking platform that fills the gap between advanced banking solutions and finance professionals.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements.

2020 was also the year of the SPACraze , with SPAC IPOs raising more than $75 billion in gross proceeds, a 525% increase compared to 2019. This may signal a promising development for early-stage life sciences companies seeking to go public in 2021. Life Sciences Enters the SPAC Party, But Will Reverse Merger Suitors Join In?

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. More than 50% of the SPACs that went public in 2020 and 2021 are incorporated in Delaware, giving particular significance to SPAC litigation filed in Delaware courts.

Per FTI Consulting , solar, wind, and “portfolio” (mixed asset) deals account for 60% of renewable M&A activity in the U.S.: For growth-stage companies, you will see plenty of equity offerings: IPOs , SPACs , PIPEs, and follow-on issuances. What Do You Do as an Analyst or Associate?

We have reviewed the bylaws of a number of corporations that have gone public through a deSPAC or traditional IPO process. We suggest that companies going public through a traditional IPO or deSPAC transaction draft the advance notice bylaws to account for the first annual meeting. 13, 2021). [4] 1, 8 (1972). [2]

The vital role of angel investing in growing the start-up ecosystem in the UK was equally recognised in Chancellor Rishi Sunak’s 2021 Autumn Budget with announcements of £150m in further funding for a regional angel investing programme.

Although the COVID-19 pandemic that defined 2020 continued to shape much of the life sciences industry in 2021, the way that it did was markedly different. 2] Examples of this strategy coming to bear in 2021 included Thermo Fisher Scientific’s acquisition of PPD for $17.4 driven assets. term average of approximately 35%.

For example, in 2021, the NBA started allowing institutional investors to own up to 20% of single teams, which led Arctos to invest 5% in the Golden State Warriors (they later increased this stake to 13%). The MLB started allowing PE ownership in 2019, and the NHL followed suit in 2021.

However, unlike the go-go era of 2021, tech deals in 2023 tended to be bolt-on rather than transformative, took longer to get done, and required more creativity and bespoke structures. Private equity activity accounted for only 27% of tech M&A in 2023, a six-year low (and a substantial decrease from the 2021 record of 36%).

billion, a 36% decrease from 2021’s record high of $1.1 2] Despite the downtrend, global tech M&A activity in 2022 remained strong relative to pre-pandemic levels and accounted for a record 20% of all global M&A activity. Deal volumes dropped from $531.13 billion [1] during the first half of 2022 to $189.17 trillion. [2]

Growth Equity Interview Questions: Markets & Investments These questions could span a huge range because they could ask you about anything from the current fundraising environment to the IPO and M&A markets to specific markets their portfolio companies operate in. Q: Pitch me a growth company that we should invest in.

The tech deal floodgates still havent opened, as persistent valuation mismatches, a still (mostly) closed tech IPO market, stiff competition and worldwide regulatory scrutiny continue to weigh on activity, particularly for VC-backed exits and mega deals. billion acquisition of Altair, IBMs pending $6.4 So is tech M&A back?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content