This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

TKO Miller Debt CapitalMarket Analysis Leverage multiples have pulled back significantly in M&A transactions from their 2021 peaks due to a tightening of the lending environment, Sr. in 2021 to 3.5x Debt remains most available in the lower middlemarket sector. Debt / EBITDA, decreased from 4.0x

Roundtable Overview During a recent virtual roundtable hosted by GF Data, SDR’s Scott Mitchell joined fellow M&A professionals to discuss the state of lower-middlemarket M&A and private capitalmarkets. Overall, 2021 appears to be headed for a significant surge in deal activity at strong valuations.

Some argue that GE offers the best of both worlds: the opportunity to fund innovation and growth – as in venture capital – plus the ability to limit downside risk and invest in proven companies – as in private equity. Others would counter that growth equity’s rapid ascent was mostly due to the easy money that persisted between 2008 and 2021.

based Harbor Beach Capital LLC in 2019, has seen competition tick up over the past couple of years. Meanwhile, barriers to entry due to capital requirements for equipment and skilled worker training haven’t stopped new investors as federal infrastructure funding and an abundance of dry powder have led PE into new investment categories.

Following a record-setting 2021 for lower middlemarket software M&A, the Software Top 50 highlights the most active software-focused dealmakers on the Axial platform. “Public market software company valuations have been battered starting in November of 2021. March 11, 2022 – Solganick & Co.

Thriving US MiddleMarket Fundraising and Resilient Private Equity Regarding Global M&A Private Equity Trends, looking at the positive news, the US middle-market fundraising landscape remained stable throughout 2022, with 156 funds closing at an aggregate value of $133.5

Periculum Capital Company, LLC (“Periculum”) is pleased to announce it has completed the sale of Central States Enterprises, LLC’s (“CSE” or “Company”) Feed and Bagging Operations located in Lake City, Florida (“Lake City”) to Furst-McNess Company. Periculum represented the Company in the sale of its grain operations to ADM in 2021.

Two-thirds of the UK’s fintech start-ups are in in the city, and in 2020, the capital attracted 94 per cent of the country’s total fintech venture capital. Beringea Beringea is a transatlantic venture capital firm with more than $800m under management across its funds in the UK and the US.

based roles at large banks as of early 2022, along with total compensation from 2021. Before you leave an angry comment to say that you or your friend earned above or below these numbers, I want to offer a quick explanation: Investment Banker Salary Changes vs. 2021 and 2020. Up until 2021, these numbers hadn’t changed much in years.

The recent purchase of Riverbed Technology LLC reflects a burgeoning niche for middle-market technology turnaround investor Vector Capital Management LP: buying companies from lenders who converted debt to equity through reorganizations. which Vector Capital acquired and sold. billion in 2015.

After a disappointing 2023 in middle-market M&A, both the U.S. economy and the market for closely held companies are off to good starts in 2024. Eaton Square is an international M&A and capital service provider whose network encompasses Europe, North America, Australia/New Zealand, and the Pacific Rim.

In 24 hours, it went from “We’re fine, but we took some losses and need additional capital” to “The FDIC is taking over, the government has guaranteed uninsured deposits, and there might be additional bank runs and a financial crisis or three.” And the impact on the banking industry , venture capital, and startups. But the U.S.

Periculum Capital Company, LLC (“Periculum”) is pleased to announce three promotions. Since joining Periculum in 2021, Taylor has supported client engagements across all service areas. The firm’s primary services include M&A, capitalmarkets, and restructuring advisory, as well as specialized merchant banking services.

This downward trend is expected to persist in the second half of the year as the industry grapples with ongoing macroeconomic challenges such as inflation, higher interest rates, and increased capital pressures. Giorgio Andonian is a Managing Director in FOCUS Investment Banking’s Auto Aftermarket Group.

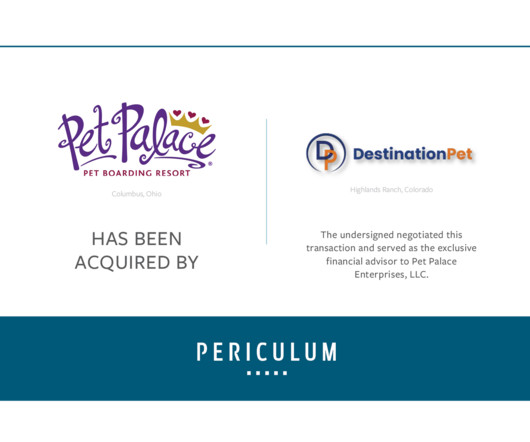

Periculum Capital Company, LLC (“Periculum”) is pleased to announce it advised Pet Palace Enterprises, LLC (“Pet Palace” or the “Company”), a Columbus, OH based provider of pet boarding, daycare, and grooming services, in its sale to Destination Pet. in its Sale to Destination Pet appeared first on Periculum Capital.

He discusses the unique approach and methodologies of Peterson Acquisitions, including their focus on effective sell-side brokerage, buy-side advisory, education, and capital investment. rn The company offers buy-side advisory services, helping buyers find off-market deals. 2021, March 10). Retrieved from [link] rn Craig, D.

Periculum Capital Company, LLC (“Periculum”) is pleased to announce it has advised Select Home Health Services, Inc. SHHS” “Company”), a leading home healthcare service provider, in its sale to Fortis Home Health and Hospice, LLC (“Fortis”), a portfolio company of Grant Avenue Capital, LLC (“Grant Avenue”).

As another example, some argue that UBS should not be a bulge bracket bank because it has focused on wealth management and areas outside the capitalmarkets. I’m still listing it because it was #9 by global IB revenue in 2021 and 2022, but I would not be surprised if it fell off this list eventually.

Intrepid Investment Bankers A Rollercoaster Ride for Software Markets It has been a disconcerting journey through the first three quarters of 2022. We ended 2021 having survived another year of the pandemic, with equity markets at or near all-time highs, interest rates near historic lows, and technology M&A activity at record levels.

While macroeconomic conditions dampened investor sentiment for risk and large-scale M&A transactions, the lower middlemarket remained healthy and robust, particularly in the global knowledge sector.

Given the size of the platform, Helmitin’s advisers are expected to market the business largely to strategics as an add-on, though sources said private equity firms with experience in adhesives and specialty chemicals will likely be invited to participate. SK Capital Partners LP and Dominus Capital LP, among several others.

Technology Private Equity Definition: A tech private equity firm raises capital from outside investors (Limited Partners), acquires minority or majority stakes in software, internet, hardware, and IT services companies, and grows and sell these stakes within 3 – 7 years to realize a return on their investment.

Soon after, the activist, Blackwells Capital LLC, settled with the combining REITs. And as Blackwells pulled back, Orange Capital Venture LP on June 15 rushed in , arguing that the activist fund was “complicit in this value destroying merger,” by receiving a large share position as part of its settlement.

“While a select few lenders have maintained their hold size parameters, the overwhelming majority of lenders have significantly reduced their check size in response to the drop off in redemptions and repayments in their portfolios,” said Joseph Weissglass , managing director at middlemarket investment bank Configure Partners LLC.

Market Trends: What You Need to Know As shown in the American Bar Association's Private Target Mergers and Acquisitions Deal Point Studies: The use of separate escrows for purchase price adjustments has been increasing on a fairly steady basis since 2007 (with a slight dip in 2021 from a 2019 high).

There’s an oversupply of capital that would like to invest in MSP assets,” said Abe Garver, managing director and MSP team leader and FOCUS Investment Banking. “We The company was purchased in 2020 by Kian Capital Partners and ParkSouth Ventures. years, according to market sources. Kaseya is an investment of Insight Venture.

Since equity deals are highly dependent on market conditions, deal flow tends to be much more uneven than in asset-level M&A. A good example is the 2020 – 2021 period, when SPAC activity went vertical, and plenty of renewable energy companies used SPACs to go public. but they are less consistent than those above.

But that timeline crept up over time, slowing down only in “crisis periods,” such as in 2009 (financial crisis aftermath) and 2020 – 2021 (COVID). based candidates in New York aiming for PE roles at mega-funds and upper-middle-market funds. On-cycle recruiting is primarily an issue for U.S.-based

A liquidity crisis slammed businesses across the board, and COVID-19 added a new layer of complexity for companies who tried to obtain capital to weather the storm. Simultaneously, other special situation funds ballooned as institutions sought to hedge against losses amid the new market and economic turmoil.

In Europe, 35% of football clubs have been funded via capital from PE/VC firms, sovereign wealth funds, or private consortiums. A great example is how many European football clubs became distressed during COVID and were forced to seek private capital. The MLB started allowing PE ownership in 2019, and the NHL followed suit in 2021.

Capital LLC aftermarket automotive chemical consumables platform Recochem Inc. Sponsors including American Industrial Partners LP , Odyssey Investment Partners LLC , Sentinel Capital Partners LLC and TJC LP , formerly the Jordan Co. acquired Recochem from Swander Pace Capital LLC in September 2018 for an undisclosed sum.

However, unlike the go-go era of 2021, tech deals in 2023 tended to be bolt-on rather than transformative, took longer to get done, and required more creativity and bespoke structures. Private equity activity accounted for only 27% of tech M&A in 2023, a six-year low (and a substantial decrease from the 2021 record of 36%).

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content