This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders.

Direct-to-consumer businesses, darlings of the investor community in 2021, saw their techlike valuations plummet. Public markets, however, have been tepid, with the much-awaited IPO of L Catterton Management Ltd. Public markets, however, have been tepid, with the much-awaited IPO of L Catterton Management Ltd.

In September 2020, the National Bureau of Economic Research released a working paper including an industry survey citing 900+ VC firms; this paper revealed a consensus that many portfolio companies were performing quite well in the face of Covid-19 and less than 10% were performing at levels that would raise significant concerns [3] [10].

Although 2022 saw a general decline in M&A activity in the life sciences industry compared to 2021’s frenetic pace (when deal volume was up 52% from 2020 ), life sciences deal flow in 2022 on balance remained strong despite the headwinds. Let’s dig in.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements.

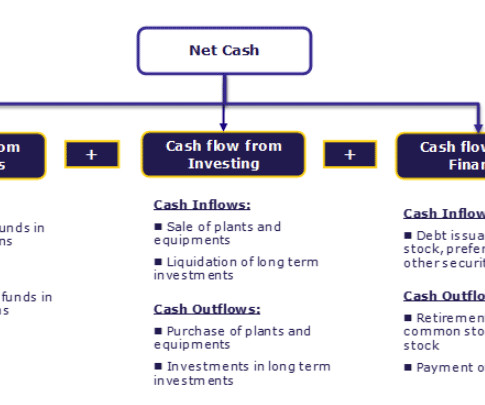

Further, statement of cash flow analysis is essential for corporate planning in the short run Short Run A Short Run in economics refers to a manufacturing planning period in which a business tries to meet the market demand by keeping one or more production inputs fixed while changing others. In 2015, Box came up with its IPO.

No matter the economic climate, you can always bet on sports fans to show up for their favorite teams. However, one common point across all the verticals is that IPOs are not common because there aren’t that many publicly traded sports teams, stadiums, or arenas.

While the decision was case-specific, we were all reminded of (i) the high bar of the MAE, particularly when changes are attributable to a systemic risk and (ii) the increasingly important role that covenants play with respect to deal certainty, particularly in periods of market and economic uncertainty. Buyer…Seller…PPP Lender?

Although the COVID-19 pandemic that defined 2020 continued to shape much of the life sciences industry in 2021, the way that it did was markedly different. 2] Examples of this strategy coming to bear in 2021 included Thermo Fisher Scientific’s acquisition of PPD for $17.4 driven assets. term average of approximately 35%.

However, unlike the go-go era of 2021, tech deals in 2023 tended to be bolt-on rather than transformative, took longer to get done, and required more creativity and bespoke structures. Private equity activity accounted for only 27% of tech M&A in 2023, a six-year low (and a substantial decrease from the 2021 record of 36%).

Divestitures, often achieved through asset sales, were also popular in 2020 as large pharmaceutical companies and biotechnology companies sought to divest noncore assets and focus on core businesses in the wake of economic uncertainty created by the pandemic. Life Sciences Enters the SPAC Party, But Will Reverse Merger Suitors Join In?

After a boom in 2020 and 2021 that saw record-breaking volumes, the market cooled considerably in 2022 and 2023. The Basics At its core, a SPAC is a shell company with no commercial operations, formed solely to raise capital through an Initial Public Offering (IPO) with the express purpose of acquiring an existing private company.

To add a growth equity spin, you can talk about wanting to understand operations and unit economics to evaluate companies. A: You like industries such as tech and healthcare, you like to understand markets, unit economics, and operations, and you want to invest in high-growth companies that need capital. Q: Why growth equity?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content