This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Overview - The year 2022 started strong but proved to be a mixed year for M&A in what could be described as a return to earth after the record-setting year that was 2021. M&A market alone exceeded $2 trillion in 2021 – a staggering figure that crushed (by nearly 30%) the then-existing record established in 2015.

Our report provides context for private companies to better understand factors influencing their valuations and evaluate how they can position themselves within a changing marketplace. This post will examine the current state of public SaaS company valuations and what it means for private companies. from 2021 by the end of the year.

Discussion Highlights Valuation Multiples in the COVID Era While the initial economic slowdown caused by COVID-19 sidelined many active transactions for a quarter or two, we have seen M&A activity (especially in the lower-middle market) recover in recent months.

2024 is poised to be another strong year for employee stock ownership plan (ESOP) transactions, with deal volume expected to eclipse 2023’s (reaching toward the highly favorable dynamics of 2021 and 2022), thanks to four key underlying drivers that should push through any economic or political uncertainty: Succession plans for countless businesses (..)

Packaging Trends Q1 M&A Update Valuations continue to remain strong across the packaging industry, despite economic uncertainty, looming economic questions, and evidence of a slight slow down in dealmaking; as a result, companies with solid fundamentals can attract premium valuations Private equity was responsible for much of the transaction volume (..)

Direct-to-consumer businesses, darlings of the investor community in 2021, saw their techlike valuations plummet. “As the economic outlook stabilizes and the [Federal Reserve] moderates some of its [rate hikes], that will drive more transaction activity,” she said. portfolio company Birkenstock GmbH & Co.

After the unprecedented market highs of 2020 into 2021, it’s natural for founders in this environment to wonder if they’ve missed the boat. Median EV/TTM Revenue Multiple Down from 2021’s high of 7.3x, 2022’s median EV/Revenue multiple of 5.6x After the market exuberance of 2020 and 2021, peaking at 8.0x in 2021 to 40.5%

By Kirstie McDermott on Growth Business - Your gateway to entrepreneurial success The last decade of UK tech has been “unprecedented”, according to Tech Nation report, saying “the positive economic impact created by founders has been almost unimaginable”.

In this article, well unpack the key valuation drivers, explore current market multiples, and offer practical steps to help you assess and enhance the value of your software business. Understanding the Core Valuation Framework At its core, the valuation of a software company is typically based on a multiple of earnings or revenue.

We ended 2021 having survived another year of the pandemic, with equity markets at or near all-time highs, interest rates near historic lows, and technology M&A activity at record levels. As public market valuations fell, SPACs evaporated and other buyers began to reevaluate the need to pay nose-bleed multiples.

Disclaimers: [link] In what seems to be a trend of shareholders contesting go-privates based on concerns over valuation ( Vista – Pluralsight , Alta Fox / Pembroke / etc. The deal is valued at ~$1 billion and expected to close by the first quarter of 2021 [2]. On January 11, 2021, T. On January 19, 2021, CKH responds to T.

Insurance M&A Deal Valuation, 2024 Starting out in 2024, EBITDA and revenue multiples are in a good place, experiencing modest YoY growth despite the economic downturn of the last 18 months. Granted, these numbers are not quite at pre-pandemic levels yet (although they are close), and they are nowhere near the M&A boom of 2021.

Today’s volatile economic environment has many business owners wondering if it is possible to sell their company now and achieve a good outcome. The Bad News Is Not So Bad Rising interest rates and economic uncertainty have tamped down the M&A frenzy that peaked in 2021.

While many of the elements that define attractive investment opportunities remain somewhat consistent, buyers and investors do tend to place more emphasis on certain criteria depending on the broader economic conditions. These are a set of criteria that lead to recession-proof businesses. Is it integral to operations?

billion in 2021. “These businesses, regardless of economic cycle, are able to deliver meaningful return on investments to the end user,” Osman said. Mubadala co-invested with Vista Equity Partners LLC in the $8.4 billion buyout of tax compliance software maker Avalara Inc. and the $2.3 billion, both in 2022.

Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest. This not only increases the revenue flow for the brokerage but also illustrates the industry’s resiliency against the economic turbulence that took place over the same period of time.

Components of the Accounting Equation Assets are resources owned by a company that has economic value and can be converted into cash or provide future benefits. billion as of September 2021. Accurate valuation of assets, such as real estate, can significantly impact a company's financial position and performance.

This brief downturn was largely attributed to temporary economic disruptions. Economic Forecasts and Future Projections Looking ahead, several factors indicate a promising landscape for SaaS M&A activity. These positive indicators suggest that the current market conditions are favorable for SaaS founders considering an exit.

They took action early on, initiating a remarkable series of rate hikes in 2021 that continued until early 2023. This swift action helped them witness falling core inflation over the last five months, giving them a head start in managing this economic challenge compared to the developed world.

Although 2022 saw a general decline in M&A activity in the life sciences industry compared to 2021’s frenetic pace (when deal volume was up 52% from 2020 ), life sciences deal flow in 2022 on balance remained strong despite the headwinds. Let’s dig in.

In September 2020, the National Bureau of Economic Research released a working paper including an industry survey citing 900+ VC firms; this paper revealed a consensus that many portfolio companies were performing quite well in the face of Covid-19 and less than 10% were performing at levels that would raise significant concerns [3] [10].

There is the risk for the consolidated financial statements that the calculation of impairment loss allowances is not carried out in an appropriate manner or is based on inappropriate assumptions, an inappropriate database or inappropriate application of the valuation model and, as a result, the impairment loss is reported in an incorrect amount.

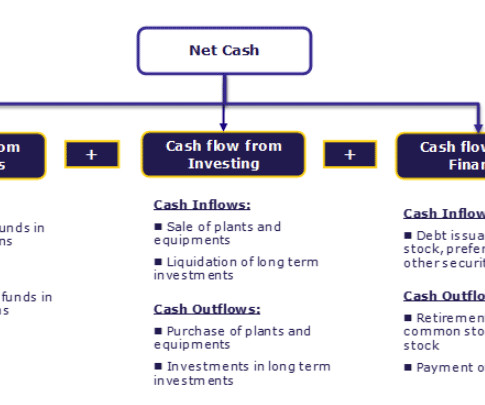

Further, statement of cash flow analysis is essential for corporate planning in the short run Short Run A Short Run in economics refers to a manufacturing planning period in which a business tries to meet the market demand by keeping one or more production inputs fixed while changing others. Example #1 ABC Inc. from 2014 to 2017.

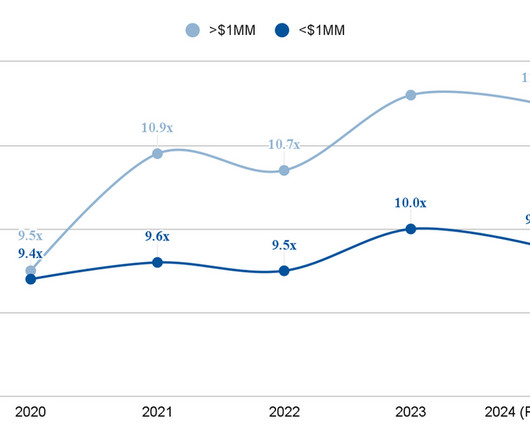

2) our team noted unexpected increases in the valuation multiples offered for insurance agencies, as depicted below. Despite years of evidence suggesting that M&A activity decreases in times of economic uncertainty, it appears that the market has evolved to meet the needs of the times.

Despite investment in the first half of 2023 dropping to £4.6bn from 2022’s £10.8bn as a result of rising interest rates, high inflation, a decrease in valuations and geopolitical tensions globally, UK fintechs are still attracting more VC investment than all other EMEA fintechs combined, with a significant percentage coming from US investors.

Interestingly, throughout 2021 and 2022, there were no U.S. Investment Themes In our prior letter, we reviewed investment themes including deglobalization, the end of zero-interest-rate policies, tepid economic growth, and the end of the current rate-hiking cycle. Its economic effect will also be deflationary. bank failures.

The recent economic volatility has also seen an increase in the use of alternatives to one-time cash purchases in the context of M&A deals , including earnouts and working capital adjustments. As of February 11, 2021, the OSC gave the green light for the first publicly traded bitcoin exchange-traded funds in North America.

Our journey reached new heights with the launch of Beyond Capital Ventures, our second fund, in April 2021. It invests in companies that prioritize serving the lower-to-middle-income consumer class, addressing the economic disparities in these markets with a gender conscious focus through the business model. million lives, including 3.4

No matter the economic climate, you can always bet on sports fans to show up for their favorite teams. This sector is the most different in terms of valuation and technical analysis because of nuances around licensing, player salaries, and different revenue streams.

2] By early 2021, Limelight had pursued a number of turnaround initiatives (including hiring a new CEO, implementing a turnaround plan and retaining a consultant), but these measures were unsuccessful. 20] In so holding, the Court was confronted with two prior Delaware Supreme Court decisions, Stroud v. Grace [21] and Williams v.

Looking ahead, we believe history will regard the 2007-2021 time period as anomalous. We believe many of these counter balances are nearing an end, and the economic impacts of the Fed’s policy, which are always felt on a lagged basis, will begin to manifest on Main Street soon. Several factors are driving this move, including the U.S.

“Under her leadership, Bravo has introduced the industry’s first AI predictive pricing tool for secondhand retailers, enabling accurate and optimized pricing for merchandise, including future valuation of inventory. This is part of a large move towards leveraging pricing for community good.”

“Under her leadership, Bravo has introduced the industry’s first AI predictive pricing tool for secondhand retailers, enabling accurate and optimized pricing for merchandise, including future valuation of inventory. This is part of a large move towards leveraging pricing for community good.”

“Under her leadership, Bravo has introduced the industry’s first AI predictive pricing tool for secondhand retailers, enabling accurate and optimized pricing for merchandise, including future valuation of inventory. This is part of a large move towards leveraging pricing for community good.”

Debt Markets Prior to COVID-19, some analysts and debt underwriters encouraged debt issuers to exercise caution after the tenth straight year of economic expansion [1]. Simultaneously, other special situation funds ballooned as institutions sought to hedge against losses amid the new market and economic turmoil.

This strong push in November and December ended the long stretch of losses that fixed-income investors have endured since 2021. Contributing to that growth were two significant happenings: America helped rebuild Europe and Japan, triggering economic benefits for our nation, and the largest generation in U.S. history was born.

Despite dealmaking anxieties in the first half of the year, valuations remained strong, and discount opportunities were few and far between. The US government implemented a number of economic stimulus measures that rippled across the M&A landscape. 2] Global deal value in the technology sector was up 47.3% Buyer…Seller…PPP Lender?

By mandating banks to hold more capital in reserve, Basel III’s goal is to improve the stability and solvency of financial institutions, alongside reducing the possibility of bank failures during periods of economic turmoil. The regulation also led to changes in risk management practices and valuation methodologies for financial institutions.

Although the COVID-19 pandemic that defined 2020 continued to shape much of the life sciences industry in 2021, the way that it did was markedly different. 2] Examples of this strategy coming to bear in 2021 included Thermo Fisher Scientific’s acquisition of PPD for $17.4 driven assets. term average of approximately 35%.

However, unlike the go-go era of 2021, tech deals in 2023 tended to be bolt-on rather than transformative, took longer to get done, and required more creativity and bespoke structures. Private equity activity accounted for only 27% of tech M&A in 2023, a six-year low (and a substantial decrease from the 2021 record of 36%).

Divestitures, often achieved through asset sales, were also popular in 2020 as large pharmaceutical companies and biotechnology companies sought to divest noncore assets and focus on core businesses in the wake of economic uncertainty created by the pandemic. Looking Ahead to 2021. Earnouts Remain Popular – and Difficult.

To add a growth equity spin, you can talk about wanting to understand operations and unit economics to evaluate companies. Reference any deals you’ve worked on that required analysis of these points and talk about how they affected the valuation or client’s decisions (this is more grounded than just saying, “I like high-growth companies!”).

Many shop owners had been contemplating selling because valuations remain at healthy levels, albeit off the 2021-22 peak, fed by the post-pandemic rebound and private equity’s desire to put their capital to work. Company valuations can change significantly even if the overall business grows, and we saw this in 2023.

The healthcare sector in the United States is a large driver of economic output. The key issue is that most businesses in this subsector started off as one-product companies and raised large amounts of capital without considering clinical utility and economic benefits. Curran Aiyer and Jonas Kurihara contributed to this report.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content