This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On the surface, things looked rough: the Dow Jones, S&P 500, and the NASDAQ all finished the year with significant losses, with tech stocks hit particularly hard. After the unprecedented market highs of 2020 into 2021, it’s natural for founders in this environment to wonder if they’ve missed the boat. 4Q22’s multiple of 5.6x

It is also important to have an accurate valuation of the business and to be aware of any liabilities or assets that could affect the sale. By 2021, the median deal size had increased to $1.8 Without accurate financials, it’s impossible to get an accurate evaluation of the business. Transferability is also key.

Insurance M&A Deal Valuation, 2024 Starting out in 2024, EBITDA and revenue multiples are in a good place, experiencing modest YoY growth despite the economic downturn of the last 18 months. Granted, these numbers are not quite at pre-pandemic levels yet (although they are close), and they are nowhere near the M&A boom of 2021.

which in 2021 was acquired by a group of investors led by BayPine LP. and has been since 2021. According to S&P Global, the monetary value of dry powder reached $2.59 Incidentally, S&P Global estimates that Leonard Green & Partners alone was sitting on $15.3 based dealership in 2020.

WiMi Hologram Cloud (NASDAQ: WIMI ) was the first IPO after the S&P 500, NASDAQ, NYSE and Dow Jones Industrial Average reached their respective 52-week lows on March 20, 2020, but this proved only the beginning of IPOs in the Covid-era portion of 2020 [14]. billion in pre-valuation at the time of their IPO, a new record [11].

The S&P 500 has recently traded near 4800, close to its record at the end of 2021. He advises business owners on sell-side and buy-side transactions, valuation analysis, corporate finance and equity and debt financing. As 2024 starts, the U.S. stock markets are at or near their all-time highs.

Possible Changes in Tax Law May Drive Transactions H2 2021 specifically saw a small surge in deal volume because of expected increases to the laws surrounding capital gains taxes. Consult data sources like S&P Global data to get an idea of a firm’s activity within the industry. Are you meeting the firm’s principals?

PE firms rely on leveraged buyouts (LBOs) for the lion's share of their deals, which often involve using the acquired company’s assets as collateral to insure the loan used to purchase it. Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest.

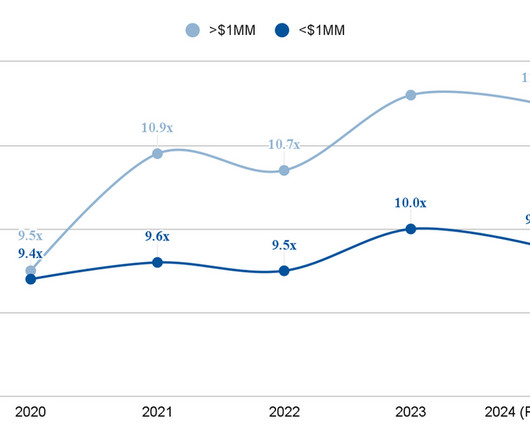

2) our team noted unexpected increases in the valuation multiples offered for insurance agencies, as depicted below. Both are already rising as of Q2 2024 , with annual numbers expected to exceed those of last year, despite falling short of the highs of 2021. When we remove this element, deal volume actually held steady.

Equities and the S&P 500 At the onset of each new year, like clockwork, we’re asked for our near-term view. benchmark equity index, the S&P 500. Consequently, by the end of July 2023, the S&P was up more than 20% for the year. This year was no different.

This sector is the most different in terms of valuation and technical analysis because of nuances around licensing, player salaries, and different revenue streams. Be prepared to discuss a recent sports deal (ideally involving a team or league) and have a rough idea of the trends, drivers, and valuation differences (see below).

This strong push in November and December ended the long stretch of losses that fixed-income investors have endured since 2021. The equity market also noted the Fed’s comments as investors piled back into equities and the S&P 500 finished the year up more than 26%. in the rising rate period and 11.8%

This happened for a few reasons: 1) Soaring Valuations – Many sources say that sports team valuations “outperformed” the S&P 500 over the past 20 years, which is a polite way of saying that many teams are now valued at extremely high multiples. only a handful a decade ago).

Though to a significantly lesser degree than in the early months of COVID, look into the rest of 2021 and beyond features continued uncertainty in the debt market. COVID-19’s impact on M&A activity varied across industries, with some reaping the benefits and others not being so lucky. So where do we go from here?

Although the COVID-19 pandemic that defined 2020 continued to shape much of the life sciences industry in 2021, the way that it did was markedly different. 2] Examples of this strategy coming to bear in 2021 included Thermo Fisher Scientific’s acquisition of PPD for $17.4 driven assets. term average of approximately 35%.

2023’s much-discussed downturn in mergers & acquisitions – with global M&A volume and value down 6% and 17%, respectively, from 2022 – was largely driven by the slowdown in the tech sector, with global tech M&A volumes down 51% year over year, while other sectors saw marked increases. [1] billion leading the pack.

New addition Biagini joins from S&P Global where he most recently served as head of data, valuations and risk analytics. Lefferts has been with LSEG since 2021, currently serving as group head of sales and account management and has been a member of the executive committee since 2023.

Government funded programs include Medicare, Medicaid, Children’s Health Insurance Program, and the Veterans Health Administration. Over the last year, the biotech industry has seen considerable growth compared to the S&P 500. How do business valuations differ in Healthcare and across its subsectors?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content