This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Uplift had raised nearly $700 million in equity and debt, securing $123 million at a reported $195 million valuation in its Series C round alone. ” Laplanche is referring to the BNPL-style product that Upgrade launched in October 2021, which lets users pay down their debt over six to 36 months with a fixed interest rate.

middle market valuation multiples and deal volume are down slightly through Q2 of 2023. this year through June 2023, but middle market valuations are down approximately 8% based on the TKO Miller analysis. Paperboard prices have also come down significantly from their peak in late 2022. Packaging Trends Q2 M&A Update U.S.

Although 2022 saw a general decline in M&A activity in the life sciences industry compared to 2021’s frenetic pace (when deal volume was up 52% from 2020 ), life sciences deal flow in 2022 on balance remained strong despite the headwinds. Let’s dig in. Let’s dig in.

For buyers, who rely heavily on debt financing to fund acquisitions, a rate cut—especially one larger than expected—creates immediate opportunities. Here’s how: Lower Cost of Debt Private equity firms typically use leverage (borrowed capital) to finance a significant portion of their acquisitions.

Inflation, supply chain disruptions and the rising cost of debt stopped consumer companies in their tracks last year. Direct-to-consumer businesses, darlings of the investor community in 2021, saw their techlike valuations plummet.

2 – Starling Bank Since the start of 2022, Starling Bank has increased its headcount by 20 per cent to over 2,000 employees, and the neobank has no plans to slow down. And it’s fair to say that for a while some private market valuations became inflated, with predictable consequences for some. Starling, though, is different.

Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest. PE Cost of Debt vs. RoR, H1 2020 - H2 2023 This inverse spread indicates one of the strongest seller’s markets we’ve seen in the insurance M&A market to date. for insurance agencies.

On September 28, 2022, Cooley sponsored the third virtual event in Axios’ Dealmakers series: A Conversation on M&A in Today’s Market. In their discussion, Leigh and Drumond surveyed 2022’s volatile deal flow, market outlook and impacts on various deal participants.

In 2023 the primary market for global convertibles was more than double since 2022, with volumes reaching USD 78Bn via 115 new issues. Financial Times published an article stating that US companies dive into convertible debt to hold down interest costs.

Intrepid Investment Bankers A Rollercoaster Ride for Software Markets It has been a disconcerting journey through the first three quarters of 2022. 2022 has seen rising inflation and interest rates, twin global disruptions in Ukraine (invasion) and China (shutdowns), and an overall economic slowdown.

It has taken two years to return to those levels, after 2022 and 2023 were burdened with interest rate hikes and fears of a recession. While the company generated over $260 million in revenues through the first three quarters of 2023, its stock price is trading under a dollar a share, as the company is burdened with substantial debt.

Starting in H2 2022, the insurance M&A market has seen a notably difficult 18-month period, afflicted with high interest rates, lowered deal volumes, and lowered valuations. If they do, then we can expect to see valuations and, by extent, EBITDA multiples for insurance agencies rise.

Other times, they are hoping to use their share of the sale to alleviate personal debt. Once you get into the valuation stage (which is usually done by your M&A advisor or a 3rd party valuation agency), you will need a large swath of documentation. Manageable Debt. Are looking for a career change.

In the US, it is common to adjust the purchase price for cash, any excess or deficit of net working capital relative to a required level of net working capital, unpaid debt, and unpaid transaction expenses of the target business as of the closing, with an adjustment done at closing based on estimates and followed by a post-closing true-up.

While the cost of debt has increased to the point that buyers often acquire brokerages at an initial loss, insurance brokerage M&A multiples have not only held steady but are actually seeing all-time highs. Equity used to consist of senior debt (i.e., the amount all common shareholders invest in the brokerage).

SVB’s deposits grew from ~$62 billion at the end of 2019 to $173 billion at the end of 2022, and its loan-to-deposit ratio went completely out of whack: Tech startups were flush with cash due to a ridiculous fundraising environment in 2020 – 2021, and they put the money they raised in the bank. to back them.

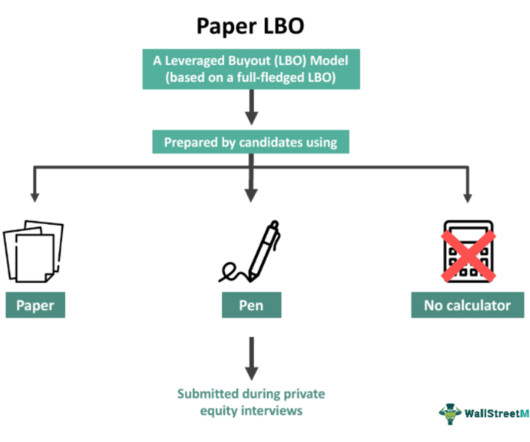

A candidate’s acumen and agility in tackling unfamiliar situations determine their grasp on subjects like valuation, forecasting, cash flow, and even the Rule of 72. This is usually calculated by multiplying the purchase multiple, a common valuation metric, by the company’s EBITDA. After this, deduct applicable expenses.

The Inflation Reduction Act imposes a 1% excise tax on certain repurchases of stock of publicly traded US corporations (“Covered Corporations”) effected after December 31, 2022 (the “Excise Tax”). [1] because SPAC sponsor shares are forfeited and not entitled to receive any distributions upon liquidation).

Bullet bonds issued by other than the government carry higher interest payments due to the credit risk Credit Risk Credit risk is the probability of a loss owing to the borrower's failure to repay the loan or meet debt obligations. The bonds mature on 31st Dec 2022. read more associated with any other issuer other than the government.

Since H2 2022, industries across the board (including insurance) have seen declines in deal volume as prospective buyers have withheld their funds for more favorable conditions in which the cost of debt is not so high. It is possible that deal durations may decrease if interest rates are lowered; however, this is no guarantee.

Financial Modeling & Valuation Courses Bundle (25+ Hours Video Series) –>> If you want to learn Financial Modeling & Valuation professionally , then do check this Financial Modeling & Valuation Course Bundle ( 25+ hours of video tutorials with step by step McDonald’s Financial Model ).

The primary sources of LMM companies are primarily different forms of debt and credit line lending systems. 3 – Mezzanine debt LLM firms mostly use it at the time of acquisitions as it uses equity in some form or another; the main advantages of it are negligible or no dilution, mostly favoring family-run enterprises.

Despite investment in the first half of 2023 dropping to £4.6bn from 2022’s £10.8bn as a result of rising interest rates, high inflation, a decrease in valuations and geopolitical tensions globally, UK fintechs are still attracting more VC investment than all other EMEA fintechs combined, with a significant percentage coming from US investors.

This chart of PE deal activity from 2001 to 2022 in the Bain Capital Healthcare Private Equity report sums up the market quite well: In short, healthcare had never been a huge sector for private equity, but activity ramped up in the late 2010s into the early 2020s, and it’s now one of the top industries by dollar volume (right after tech).

Interestingly, throughout 2021 and 2022, there were no U.S. As we wrote in our Q4 2022 newsletter, we believe that the Fed will stop raising rates during the second quarter of 2023. If you missed our previous coverage, you can read our Q4 2022 newsletter here: [link].) SVB is the second-largest bank failure in U.S.

The elevated inflationary period experienced in 2022, combined with challenging demographics faced by our nation, have contributed to this uptick. budget deficit and its upcoming substantial debt repayment, which will require refinancing in the next three years and expand the size of current Treasury auctions.

Capital is available, valuations have started to normalise and the debt markets are still supportive – albeit with greater scrutiny and higher costs. The data below from Statista shows the volume of UK private equity deals between 2017 and 2022. They helped to build trust, mutual respect and a shared vision of the future.

rn rn rn Article: rn Thriving in the E-Commerce M&A Space: Strategies for Buyers and Sellers rn Navigating the intricate world of buying and selling businesses requires a nuanced understanding of market trends, valuation practices, and strategic negotiation. Great investment." No one wants to buy that."

Although the aggregate global M&A deal value dropped significantly in 2023, the number of deals consummated only decreased by 6% compared to 2022. Activists did not hesitate to target foreign private issuers listed in the US, announcing 62 campaigns in 2023, as compared to 42 campaigns and 15 campaigns in 2022 and 2021, respectively.

The regulation also led to changes in risk management practices and valuation methodologies for financial institutions. The regulation entered its final phase in September 2022 , bringing its six-year implementation journey to an end.

2023’s much-discussed downturn in mergers & acquisitions – with global M&A volume and value down 6% and 17%, respectively, from 2022 – was largely driven by the slowdown in the tech sector, with global tech M&A volumes down 51% year over year, while other sectors saw marked increases. [1]

Tech M&A in 2022 was a tale of two halves. billion [1] during the first half of 2022 to $189.17 billion in the second half, resulting in total 2022 volume of $720.3 billion [1] during the first half of 2022 to $189.17 billion in the second half, resulting in total 2022 volume of $720.3 trillion. [2] trillion.

11 filing’s that membership revenue is “over two-thirds” of total revenue Total revenue is approximately $350 million based on 260 units Estimated to be approximately 11% of revenue; same % as Mister Car Wash If the estimated $146 million of EBITDA at peak is true, raising $650 million of debt doesnt seem off base.

Over the course of the year, many of the headwinds that have slowed tech M&A activity since 2022 began to abate as interest rates moderated, the acquisition financing market returned and equity markets reached new highs. billion acquisition of Altair, IBMs pending $6.4 billion acquisition of HashiCorp and a Permira-led consortiums $6.9

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content