This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Accounting firm mergers and acquisitions (“M&A”) are blossoming due to strong recurring revenue models, a great record of organic growth over three decades, light asset investment requirements, and economic recoveries and growth worldwide following the pandemic. These factors have created the opportunity for industry consolidation.

The core element of M&A is company valuation. Strategy, due diligence, financing, purchase price, and buyer-seller alignment all revolve around valuation and the enterprise value for the buyer and the seller. Valuation focuses on two questions: 1. Do they have the cash of debt/equity capacity to bid aggressively?

Thus far, we have covered four popular valuation methods in M&A (DCF, Comparable Company, Precedent Transaction, and LBO) and one less known one that is making its way out of the academic realm into the business world (Dividend Discount Method, DDM). The 2nd valuation method for today is the Liquidation Value method.

Working in private equity is highly attractive for many reasons, and many finance professionals who are not already in the field often look for ways to break in. One of the primary ways to do so is by landing an internship at a private equity firm you might want to work at.

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Essentially, it is a way to value a company based on cash generated from operation, taking into account all major expenses.

Thus far, we have discussed three common valuation methods that most strategic and financial acquirers use when valuing a company for acquisitions or investments. This current post about Leveraged Buy Out (LBO) is about a valuation method used by a very specific type of financial acquirer: private equity (PE) firms.

Private equity firms play a vital role in the broader investment landscape, and their success relies heavily on their ability to execute deals effectively. Simply put, any private equity associate course must focus on developing and refining these skills. We understand that, as a junior in the finance industry, time is of the essence.

To pick up where we last left off with valuation, I will cover the topic of a Merger Relative Valuation in this blog post and move on to other non-valuation topics from here. Negative equity balance. For the accounting professionals out there, earnings manipulation is a matter of concern. Working Capital deficit.

In the pursuit of attractive equity returns, private equity firms have developed numerous innovative strategies beyond typical leveraged buyouts and take-private transactions. As it happens, this is an industry that has experienced a significant amount of private equity-backed roll-up activity.

Thus far, we have discussed five valuation methods: DCF, Comparable Company, Precedent Transaction, LBO, and Dividend Discount Model (DDM). So, a good valuation model has to take into account the possibilities of a variable having multiple values along with each value’s probability of occurring.

The private equity industry has experienced significant growth in recent years, leading to a highly competitive job market for aspiring professionals, particularly at the associate level. Below, I will provide a comprehensive guide on how to stand out in the competitive private equity associate job market.

Private equity consulting firms play a crucial role in the success of portfolio companies by providing specialized expertise and strategic guidance. Private equity consulting firms go beyond traditional advisory services by providing value-added services to their clients.

The paper LBO is one of the most commonly used and intimidating interview techniques for private equity. Many candidates dread the paper LBO, but simply put, it is one of the most definitive “weeder” techniques used by many private equity firms and investment banking to lower the applicant pool.

The objectives you set for the business will dictate the type of finance you should raise: the two key options being equity (selling shares in your company) and debt (borrowing from a bank or financial institution). If growth and sale are not part of your plan, then an equity raise is not the right choice for you.

The accounting equation is a fundamental concept in finance that every private equity professional, investment banker, and corporate , finance expert should be familiar with. In this article, we will explore the components of the accounting equation, its importance in finance, and real-world examples that illustrate its significance.

Over the past few decades, growth equity (GE) has gone from an afterthought to a major asset class for huge investment firms. Some argue that GE offers the best of both worlds: the opportunity to fund innovation and growth – as in venture capital – plus the ability to limit downside risk and invest in proven companies – as in private equity.

b' E159: Building an Empire - Businesses, Private Equity, And M&A - With Adam Coffey - Watch Here rn rn _ rn Sponsor: rn rn Reconciled provides industry-leading virtual bookkeeping and accounting services for busy business owners and entrepreneurs across the US.

Private equity value creation came on my radar a few years ago when I noticed something: Even though traditional PE deal roles were not doing well, “operational” or “value creation” teams still seemed to be recruiting. What Does the Private Equity Value Creation Team Do in Real Life? Why is PE Value Creation Suddenly “Hot”?

Corporate finance jobs at normal companies are bad … …if you’re using them to break into a deal-based field, such as investment banking , private equity , or venture capital , or as a “Plan B” if you interview around but do not get into one of these. You may have more options in certain groups, such as Treasury.

The Verdict is In on the Sell Side: Business Valuation Basics By Brian Goodhart Valuation is a fundamental aspect of the complex and intricate world of mergers and acquisitions. Today, we will delve into the intricate art and science of valuation, exploring its various components and purposes.

As with investment banking in Hong Kong , I can summarize private equity in China in one sentence: “If you’re not Chinese, don’t even think about it, and even if you are Chinese, it’s best if you have great connections within the CCP and want to stay in China long-term.”

Accurate and appropriate valuation is one of the pillars of maximizing the profits from a business sale. However, company valuation isn’t as simple as slapping a price on your business. It’s a delicate balancing act, as inaccurate valuations have polarizing consequences.

If you don’t have an account already, create a free account here and purchase our Buyside Starter Kit with the code BUYSIDESTARTER here. If you’ve ever thought that Buyside might be for you — whether it be Growth Equity, Private Equity, Hedge Funds, Corporate Development, Venture Capital, etc.

Uplift had raised nearly $700 million in equity and debt, securing $123 million at a reported $195 million valuation in its Series C round alone. Klarna , once Europe’s most valuable VC-backed company, suffered an 85% valuation cut, from $45.6 billion to just $6.7 billion in July 2022 following an $800 million round.

wallstreetmojo.com) Balance Sheet The Balance Sheet A balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the company at a specific point in time. How to Read Balance Sheet Equity? How to Read Balance Sheet Liabilities? How to Analyze the Balance Sheet?

Sales Return in terms of payroll journal entry can be defined as the one which shall be used to account for the customer returns in the books of account or to account for when there is a return of goods sold by the customer due to defective goods sold, or misfit in requirement of the customer, etc. read more is tallied.

For private equity investors who have been monitoring the situation around inflation for the last few months to a year, many have been disappointed to see the slow trajectory with which inflation has been coming down from highs. Explore the role of private equity now. Currently, inflation in the U.S.

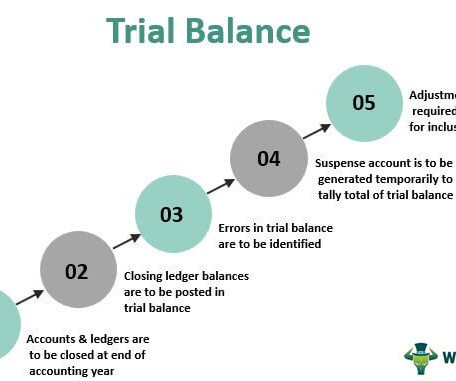

Trial Balance Meaning Trial Balance is the report of accounting in which ending balances of a different general ledger of the company are and is presented into the debit/credit column as per their balances, where debit amounts are listed on the debit column, and credit amounts are listed on the credit column.

As you meticulously evaluate financial statements, assess market conditions, and fine-tune your pitch, it’s crucial not to overlook the less conspicuous elements that can significantly influence your business’s valuation in mergers and acquisitions (M&A).

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

Ever since the 2008 financial crisis, there has been massive hype about both private equity and technology. Over the past few decades, technology private equity has gone from “barely existing” to representing the largest single sector in PE by both deal value and deal count. Why Did PE Firms Start Buying Tech Companies?

Having spent time in technology growth equity and VC in college, I realized quickly that my passions and career goals didn’t align with RX or the exit opps from MM banking to MM private equity. Fortunate enough to be one of the “lucky ones”, I landed my first banking role at an MM shop on the Restructuring team. Knowledge is Power.

Thriving US Middle Market Fundraising and Resilient Private Equity Regarding Global M&A Private Equity Trends, looking at the positive news, the US middle-market fundraising landscape remained stable throughout 2022, with 156 funds closing at an aggregate value of $133.5 While average valuations in the U.S.

Software Equity Group closely monitors M&A activity, historical trends, and insights from the investor and strategic buyer community to paint a more complete picture of what’s happening. Here’s a closer look at what the future looks like for the SaaS M&A market and its valuation multiples.

Advisory Panel Members: – Private Equity Investors – Investment Bankers – M&A Accounting Professionals – M&A Legal Firms To watch GF Data’s full coverage of the roundtable event, click here. Overall, 2021 appears to be headed for a significant surge in deal activity at strong valuations.

You may have heard the term “business valuation” in the context of selling a company. But a business valuation is much more than a tool to assess how much a buyer might pay for the company you have spent years building. At any stage of your business’ lifecycle, a valuation can create a competitive advantage.

Navigating M&A valuations with precision is paramount for informed decision-making. Our guide equips you with step-by-step instructions on employing the Enterprise Value Calculator effectively, complete with insights into optimal practices for precision valuations. Let’s dive into the intricacies of this invaluable resource.

Accrued interest Accrued Interest Accrued Interest is the unsettled interest amount which is either earned by the company or which is payable by the company within the same accounting period. Still, the same is not received or paid in the same accounting period. The maximum amount to be invested in the scheme is Rs 1 50,000 a year.

Going to keep today rather simple — we want to celebrate and kick off the second half of the year with a simple offer for the first 10 people that take advantage of the below — PE Platform Access for $225 OFF = $74 out of pocket for lifetime access Our flagship program has placed mentees into most major private equity firms since launching in 2020.

When you hear the words “healthcare private equity,” two thoughts probably come to mind: Wait a minute, isn’t healthcare a risky/growth-oriented sector? Before delving into these nuances, we should take a step back and define the sector: Definitions: What is a Healthcare Private Equity Firm? Why do PE firms operate there?

When You Need to Return Cash in order to Raise More original article sourced by Ryan Gould, Bloomberg, sourced link above The world’s private equity firms have cash to burn. Private equity players have to face reality at some point,” said Per Franzen, head of private capital for Europe and North America at EQT AB.

The difference pays off in higher valuations: Companies that can retain and grow within their customer bases, particularly in the face of a recession, are rewarded with higher multiples. These factors make high-NRR companies attractive to investors and buyers, often resulting in higher valuation multiples.

By Dom Walbanke on Growth Business - Your gateway to entrepreneurial success Raising private equity funds is seen as the holy grail for businesses who want to grow quickly, simply because the strength of capital opens the door for rapid growth.

For top private equity firms, there’s a lot to like about SaaS. Top Software Private Equity Firms Here is a select list of the most active PE investors in the SaaS and software industry over the past year (data taken from the SEG 2024 Annual SaaS Report ). The firm currently employs 31 professionals. The firm employs 93 professionals.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content