This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Securities and Exchange Commission (SEC) adopted final rules (the “Final Rules”) related to special purpose acquisition companies (SPACs) and de-SPAC transactions.[1] Securities and Exchange Commission (SEC) adopted final rules (the “Final Rules”) related to special purpose acquisition companies (SPACs) and de-SPAC transactions.[1]

On January 24, 2024, the Securities and Exchange Commission (“SEC”) adopted final rules (the “Final Rules”) to enhance disclosure and investor protection in initial public offerings (“IPOs”) by special purpose acquisition companies (“SPACs”) and in business combination transactions involving shell companies, such as SPACs, and private operating companies (..)

Last week, the SEC announced settled enforcement proceedings against Cantor Fitzgerald for its alleged role in causing two SPACs that it controlled to make misleading statements to investors about the status of their discussions with potential acquisition targets ahead of their initial public offerings (IPOs).

Angel investors include executives from Plaid, Brex and Instacart, along with Stripe CEO Patrick Collison. Financial terms of the deal, which marks Stripe’s first acquisition since it bought card reader provider BBPOS in January of 2022, were not disclosed. Okay had seven employees prior to the acquisition. Sign up here.

For private equity investors, one of the most important considerations for a successful investment is determining the value the firm will receive at exit, which directly impacts fund returns. Private equity investors often have a 5 to 7-year investment horizon and expect a significant return at the end of this hold period.

British tech firm valued at $52.3bn before highly anticipated flotation on Nasdaq by private owner SoftBank The British chip designer Arm has secured a $52.3bn (£41.9bn) valuation in its initial public offering (IPO), before its highly anticipated return to the stock market in New York on Thursday. shares, raising $4.87bn for Softbank.

b' E202: M&A for Entrepreneurs: Leverage Acquisitions to Scale Your Business Faster with Dominic Wells - Watch Here rn rn About the Guest(s): rn Dominic Wells is an accomplished entrepreneur and the CEO of Onfolio, a publicly traded company specializing in the acquisition of online businesses.

However, for private equity investors, this uncertainty represents a unique opportunity to take advantage of investment opportunities in public markets. According to the Institutional Investor, 81% of value in all transactions in 2023 so far were take-private deals (compared to 20% seen in a typical year).

However, for private equity investors, this uncertainty represents a unique opportunity to take advantage of investment opportunities in public markets. According to the Institutional Investor, 81% of value in all transactions in 2023 so far were take-private deals (compared to 20% seen in a typical year).

Many of these causes have their equivalences to the reasons behind the sale of a company (also known as a divestiture): Liquidity: As the equity holding period matured, investors (private equity funds behind companies) will look to sell. What are the recent (less than 5 years old) acquisition activities in this industry segment?

In a conversation with TechCrunch, Renaud Laplanche, Upgrade’s CEO and a co-founder, said that Uplift initially reached out in May to inquire whether Upgrade would be interested in participating in Uplift’s Series D financing as a strategic investor. Changing consumer spending habits likely played a role in scaring investors away.

On November 24th, Burson Cohn & Wolfe (BCW) brought together experts from across financial services to discuss current activity and prospects for special purpose acquisition companies (“SPAC”). According to Odeon Capital Group research, as of December 2, 2020, 210 SPAC IPOs had been completed representing gross proceeds of ~$72 billion.

After raising $100 million at a valuation of over $2 billion last year, the Australian ed-tech startup Go1 is making an acquisition and getting some investment to expand its reach and technology to serve the market of corporate online learning.

It has become a preferred choice for investors seeking attractive returns and diversification from traditional investment options such as stocks and bonds. VC investors provide capital to startups and small businesses in exchange for equity ownership. Venture capital focuses on early-stage companies with high growth potential.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders.

Special purpose acquisition companies (SPACs) have exploded as an increasingly popular way for private companies to go public. There were more SPAC IPOs in 2020 than traditional IPOs. Many leading investors and businesspeople (not to mention a number of celebrities and athletes), are participating in some way in the SPAC boom.

There might be marginal differences, such as Series B1’s round not ending in an investor taking a board seat and B2’s does, for example. It is worth noting that at the pre-seed and seed stage, investors will put much of the spotlight on you and your team. How to pitch to investors: What fundraising collateral do I need?

2) Unleashing Returns Every LBO model is underpinned by the drive to generate lucrative returns for investors. In an LBO scenario, both debt and equity investors commit capital to the target company. Within an LBO framework, investors aim to boost returns by leveraging debt to magnify equity returns.

And with more than 22 years in the field and involvement in more than 700 such vehicles under his belt, he brings a much different perspective on the market than many lawyers that may have recently jumped into special purpose acquisition companies.

In the dynamic world of mergers and acquisitions (M&A), staying ahead of the curve is crucial for success. Investors are also placing greater emphasis on ESG performance as a critical determinant of company valuations and investment decisions.

These include prevailing market sentiment, current appetite for acquisitions in a particular sector and the political and economic environment, all of which can change well within a given transaction timetable. To determine whether a dual-track process is right for your company, consider these six key questions: 1.

Event-driven hedge funds differ from other funds because they rely on specific “hard catalysts,” such as acquisitions and divestitures. Here it is in the investor presentation: We don’t know the planned valuation for CMS in this spin-off, but let’s assume that Jacobs plans to spin it off at an IPO offering price that implies an 11.5x

In a significant move to capitalize on the burgeoning Special Purpose Acquisition Company (SPAC) market, MergersCorp has announced the launch of specialized services tailored specifically for SPACs. The decision to roll out these dedicated services comes as the SPAC market has shown resilience and adaptability amid varying market conditions.

billion of equity raised over the last five years, as well as ranking number one for UK IPOs under £1 billion market capitalisation by deal volume over the same time frame. The deal comes just three months after Deutsche Bank completed the acquisition of institutional broker Numis for £410 million.

Investment banking is a branch of banking that organizes and enables large, complex financial transactions for businesses, like mergers, IPOs or underwriting. Investment Banking Services Initial Public Offering (IPO) When a privately-owned business wants to become a publicly traded company, it goes through an IPO , or Initial Public Offering.

is the increased frequency at which SPAC IPOs are occurring. As reflected in Chart 1 , 102 SPAC IPOs have been announced this year as of September 18, 2020—almost double the number of SPAC IPOs in all of last year (and more than double the number of SPAC IPOs in 2018). A distinct feature of SPAC 3.0 Fewer Redemptions.

As further discussed below, private equity firms raise funds from institutional investors and use these funds to acquire ownership stakes in businesses. Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank.

Renewable Energy Investment Banking Definition: In renewable energy investment banking, bankers advise companies in the solar, wind, biofuel, storage, battery, smart grid, electric vehicle, hydrogen, hydroelectric, and carbon capture verticals on equity and debt issuances, asset deals, and mergers and acquisitions.

Investment Banking: Deals The basic difference is that in “investment banking” groups, such as technology , TMT , healthcare , or consumer retail , you work on various deal types: sell-side and buy-side M&A, leveraged buyouts, IPOs, follow-on offerings, and bond issuances. or debt offerings (investment-grade or high-yield bonds).

First, there’s the ability to raise substantial capital by issuing shares to the public in an initial public offering (IPO), as well as secondary offerings. Lastly, going public is a liquidity event for the founders and early investors, allowing them to cash in on their success. Today, the number of U.S.

As further discussed below, private equity firms raise funds from institutional investors and use these funds to acquire ownership stakes in businesses. Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank.

Before you consider any offers to buy your business, it is important to understand the differences between these private equity acquisition strategies and how each will impact your liquidity at closing and your involvement in the company going forward. This is often called a “buy and build” approach.

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements.

Special purpose acquisition companies (SPACs) are on the rise. According to Nasdaq , in 2015, SPACs made up approximately 12% of the IPO market, but by 2020, that number had risen to approximately 53%. SPACs are predicted to be an even higher percentage of the 2021 market share, with SPACs representing 79% of the January IPOs.

This style is about purchasing minority stakes in cash-flow-negative-but-high-growth companies that want to scale and eventually go public or sell (think: Uber or Airbnb before their IPOs). There’s usually a long list of previous VC investors as well. In the 2010s, startups began to postpone their IPOs, but they still needed funding.

Portfolio Management Merchant banking companies provide portfolio management services to high -net-worth individuals and corporate investors. Underwriting Services Merchant banks also provide underwriting services for initial public offerings (IPOs), private placements, follow-on public offerings (FPOs) and rights issues.

There is a wide variety of early-stage lenders: large institutional investors, boutique specialist lenders, and high-net-worth individuals are common sources of debt financing. You can also sell debt instruments such as bonds, bills, or notes to investors to raise capital.

For public companies with well-performing stocks (or at least for those doing better than their peers) looking for strategic acquisitions, using stock as acquisition consideration will present a viable alternative to cash. the SEC does not shut the door on the use of projections in deSPACs).

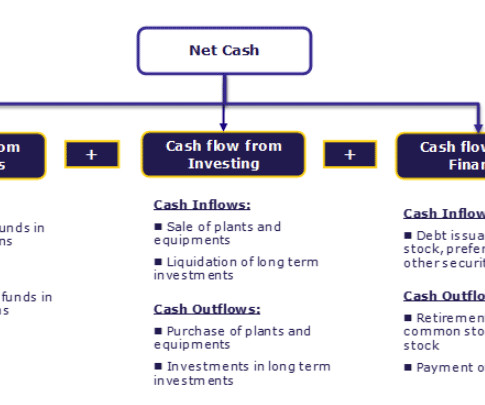

It aids investors in analyzing the company's performance. read more like investors, shareholders Shareholders A shareholder is an individual or an institution that owns one or more shares of stock in a public or a private corporation and, therefore, are the legal owners of the company. read more arising from each activity.

Take a strategic approach by assessing your business’s strengths, weaknesses, opportunities, and threats (SWOT analysis), identifying potential buyers or investors, and determining your desired exit timeline. Start early, ideally years before you intend to exit, to allow sufficient time for preparation and implementation.

The decision between forming a C Corp, S Corp, or LLC can significantly affect your company’s tax obligations, flexibility in ownership, and attractiveness to investors. The flexibility to have multiple stock classes is a major draw for institutional investors. Are S Corps Ideal for Software Companies?

For example, in the biopharma space, AbbVie, Bristol Myers Squibb, AstraZeneca, and Roche each announced multiple big-ticket acquisitions in the fourth quarter – including Abbvie’s acquisition of ImmunoGen for $10.1 billion; Bristol Myer Squibb’s acquisition of RayzeBio for $4.1 billion and Cerevel Therapeutics for $8.7

In the fast-paced world of mergers and acquisitions (M&A), two titans of finance go head-to-head: venture capitalists and private equity firms. From sourcing deals and conducting due diligence to negotiating terms and post-acquisition management, these power players navigate complex landscapes with enormous financial stakes.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content