This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

Selling an insurance brokerage is not altogether that much different than selling an insurance agency or even an insurance company. specialized regulatory and licensing requirements that are different from those of insurance agencies. That being said, brokerage owners need to consider a.)

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Elements Are Included in Adjusted EBITDA for Insurance Agencies?

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. We’ll also detail some of the factors affecting these calculations.

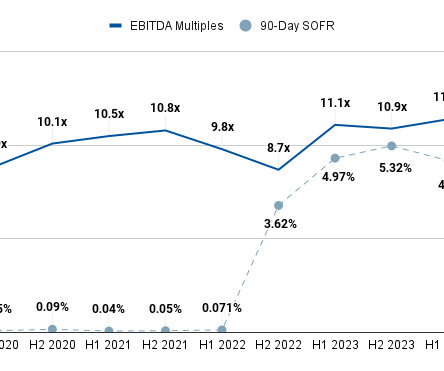

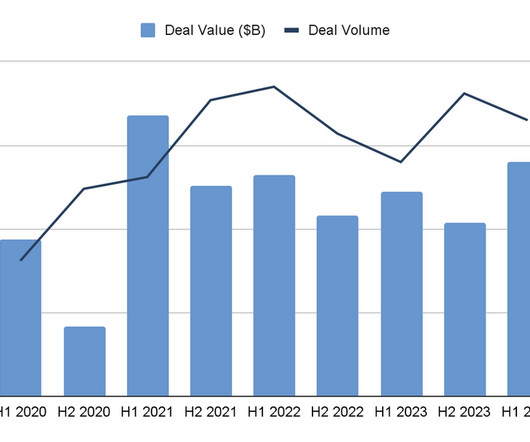

The following report details insurance brokerage M&A multiple averages for H1 2024. Our research team averaged the information using data from our Sica | Fletcher index, which monitors approximately 70% of insurance sector transactions. Because several kinds of insurance are legally required (e.g.,

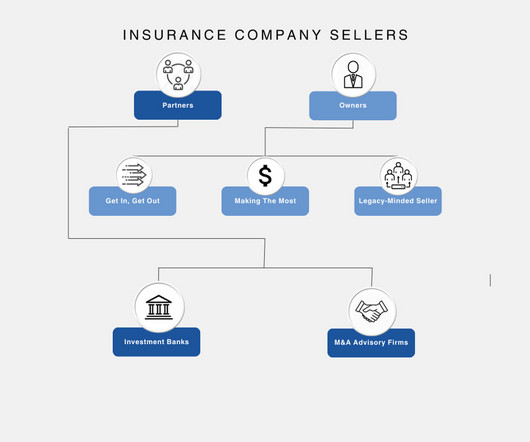

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome.

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. Selling an insurance agency book of business has a few advantages over selling the agency in total. Why Sell Just the Book?

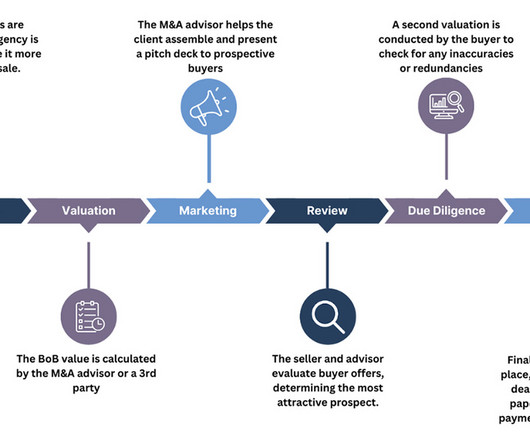

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

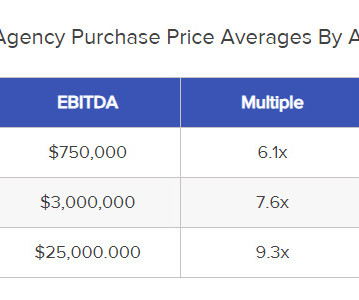

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

For agency owners looking to sell their business in 2024, it’s helpful to know something about the insurance M&A buyer landscape before going in. The following section details the insurance M&A buyer landscape as of Q3 2024. To provide a sense of context for buyers’ current standing, we also include information from 2023.

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Agency vs. Company: Which Is The Better Insurance M&A Deal?

Although insurance agencies are not always family affairs, the 2024 insurance landscape reveals that between 50% and 70% of agencies are family-owned. The valuation process has a few additional considerations when selling a family insurance agency. In particular, sellers should be aware of: Family Reputation as an Asset.

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

Disclaimer: The article below contains a quick and easy method for calculating the ballpark value of an insurance agency using standardized market information. Readers should note that the actual value of your insurance agency may vary considerably from what this estimate might provide.

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. for insurance agencies.

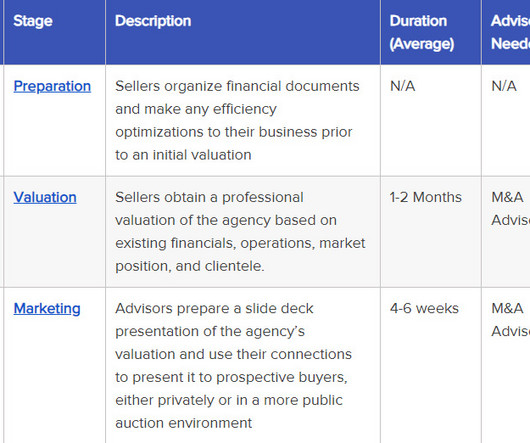

This article outlines how to sell an insurance agency by chronological steps, with a quick overview of the process in the table immediately following. We also include some key insights we’ve gathered over several decades of selling insurance agencies. and EBITDA gives buyers a better sense of the agency's future profitability.

Functions of Merchant Banks A merchant bank’s primary function is to provide financial and advisory services to medium-sized businesses. Morgan Stanley India: Global investment bank with a strong presence in India, offering services such as underwriting, M&A advisory, and equity research.

The following article discusses how to value a Registered Investment Advisory firm (RIA) prior to taking it to market. About Sica | Fletcher: Sica | Fletcher is a strategic and financial advisory firm focused exclusively on the insurance industry. Who Performs A Valuation?

For example, they offer a start-to-finish plan that is targeted towards first-time buyers and provides comprehensive buy-side advisory services. Ad backs refer to expenses that are added back to the business's profits to make it appear more profitable than it actually is. or contract and need help with the due diligence process.

If representation & warranty insurance is available but the buyer instead requires an escrow to cover breaches of representation of warranties or a shortfall in net working capital delivered at closing, suddenly the deal could be worth less than you may have originally anticipated.

Insure the Deposits – But this is expensive and is available only up to a certain per-account limit in most countries, such as CHF 100,000 in Switzerland and $250,000 in the U.S. But that would have happened anyway because of the firm’s plans to spin off its IB group into Michael Klein’s advisory firm, M. Klein & Co.

Teachers Insurance and Annuity Association of America (TIIA ) , TIAA acquired Nuveen, a mutual fund and advisory firm, from Windy City for $6.25 billion dollars, plus an earn-out based on Nuveen’s future profitability. In Windy City Investments Holdings, LLC v.

This includes making sure that the business is properly insured and that all taxes and fees are paid on time. By minimizing perceived risk, entrepreneurs can increase their chances of success and ensure a profitable venture.

Risk Mitigation: Develop strategies to mitigate or manage each identified risk: Implement financial hedging and insurance solutions for financial risks. Enhance operational controls and processes to reduce operational risks. Formulate strategic initiatives to address market competition and regulatory changes.

Risk Mitigation: Develop strategies to mitigate or manage each identified risk: Implement financial hedging and insurance solutions for financial risks. Enhance operational controls and processes to reduce operational risks. Formulate strategic initiatives to address market competition and regulatory changes.

Financial Synergy : Financial synergy involves leveraging combined financial resources, such as capital, cash flow, or risk management capabilities, to achieve cost savings, maximize profitability, and enhance investment opportunities. Sharing risks across entities can lead to reduced insurance premiums and improved financial resilience.

Advisory Role The business sale process is extremely rewarding but equally excruciating. The process will have some of these steps Financial Due Diligence Buyer and his/her team will inspect a minimum of the last 3 years of financial statements, sales and profits by business line, product and service categories and customer segments.

Insurer Lemonade and pasture-raised egg brand Vital Farms each debuted from their respective 2020 IPOs as a “public benefit corporation” (PBC), which is a corporation that places dual consideration on its contributions to social good and the maximization of shareholder profits. 5] Lazard’s Shareholder Advisory Group.

Selling a Repair Shop for Maximum Profit With Giorgio Andonian The tire and auto repair industry is experiencing a wave of consolidation as shop owners consider mergers, acquisitions, and succession planning. Theres a lot of Capital gains and tax advisory that needs to go into it. S Corp as an asset sale. And I think its so important.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content