This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thus far in the last 10 blog posts, we have discussed what M&A is, its success metrics, types of acquirers and value creations, capital structure, debt, and equity. In Blog #02 of the M&A series, we discussed SWOT analysis. and (4) support long-term business strategy. and (4) support long-term business strategy.

At Accenture’s capital markets team, we’ve completed a research project into the future of capital raising. We discussed some of the findings at a breakfast during Sibos , and I thought, I would share some of the headlines in this blog. What’s actually going on with capital raising? And how exactly is it raised?

Before we move on to the buy-side and sell-side process of M&A next week, I’d like to wrap up this week by discussing the other capital structure component / tool: equity. As we mentioned in the past, equity is the most expensive form of capital (compared to debt with tax-deductible interest). However it is also the most flexible.

In this light, The M&A Lawyer Blog has created an M&A forms database consisting of carefully curated, high quality forms and precedent created by top law firm attorneys, including purchase agreements, merger agreements, escrow agreements, closing certificates, consents and more.

Calculate cost of debt, cost of equity, and weighted average cost of capital (WACC). The 7th step in the DCF method calls for the calculations of the cost of debt, cost of equity, and the weighted average cost of capital (WACC). It is a good practice to verify the intended debt-vs-total-capital balance post-transaction when possible.

Calculating cost of debt, cost of equity, and weighted average cost of capital (WACC). The multiples calculation then proceeded as follow: Market Capitalization = Share Price * Fully-diluted Shares Outstanding. Enterprise Value = Market Capitalization + Total Debt - Total Cash.

In the last two blog posts, we walked through capital structure and how it impacts M&A activities and vice versa. To be explicitly clear, I am recommending the use of the following ranked capital sources when paying for an acquisition: cash (from the balance sheet), debt (at a reasonable level), and equity.

It has been roughly three years since my last blog post at the completion of my fellowship. To pick up where we last left off with valuation, I will cover the topic of a Merger Relative Valuation in this blog post and move on to other non-valuation topics from here. Working Capital deficit. Negative equity balance.

Access to credible sources of information such as SEC EDGAR database , Treasury.gov , OECD GDP Forecast , Mergent Online, S&P Capital IQ, Hoovers, ValueLine, Yahoo Finance , MarketWatch , and Damodaran Online. Inexpensive Excel-plugin simulator such as @RISK are available for download online.

Lack of financial resources to grow: Lack of capital to properly market, R&D, and/or acquire may drive shareholders elsewhere. Normalizing capex versus expenses: to minimize earnings, private companies expense investments that should be capitalized.

A long time ago I wrote a blog post about rehypothecation with brokers. And provided the capital requirements are adequate (and they mostly are) the broker dealer won’t fail. Goldman Sachs claims that they can determine the capital requirements of their broker dealer intra-day. It is - unsurprisingly - relevant again.

The SEC announced that its Division of Corporation Finance is further facilitating capital formation by enhancing the accommodations available to companies for nonpublic review of draft registration statements. By: Stinson - Corporate & Securities Law Blog

For those of us who have borrowed money based on collateral, this blog post will feel familiar. Thus far, we have discussed many aspects around capital structure and debt financing, including how debt levels are determined by a company’s cash flows, enterprise value, and asset values. as a part of a multi-tier capital structure.

The range of value: Typically depends on performance variables (sales, margins, and capital requirements). To answer this question, three things are needed: The company’s intrinsic value: Typically based on cash flow streams available to shareholders, premiums paid in the marketplace, and scarcity associated with the target.

The direct lease business is valued based on cash flow, cost of capital, and residual value. Leasing companies: thanks to directly leasing and originating leases for other leasing companies - is often valued based on a combination of two methods. The lease origination business is valued at a multiple of upfront fees less costs.

Because dividends is a piece of equity, we can use the Capital Asset Pricing Model (CAPM) to calculate the proper Rate of Return (r). For the purposes of this post though, we will keep matters concise by discussing only the most practical and commonly accepted aspects of each step.

Revolver / line of credit This bank-provided credit facility is typically used to finance working capital due to its short duration (1 year) and low cost. We will review how we can determine the availability of this capital through an ABL analysis several posts from now.

For this table, recall that LBO transactions are heavily financed with debt (it can go up to 90% of the capital structure for some deals). Capex as % of Sales = - Capital Expenditures / Revenue. Knowing the amount of money that is needed for the proposed transaction (Total Uses), we proceeded with the building of the Sources table.

In this week’s blog, I will be a bit off base from the instructional content that I try to share every week. Let me be very clear at the outset: my role as Head of Capital Markets Recruiting for H. Next week, we will resume our regular content blog. Harlan publishes a blog every Thursday here.

That’s why I thought the Chancery Court’s recent letter decision in Aldrich Capital Partners Fund, LP v. 5/24), was worth blogging about. Maybe it’s because I hated doing them so much as a junior associate, but whatever the reason, I am always drawn to Chancery Court decisions addressing disclosure schedules.

Note: Although this blog may be a bit more self-serving, I’d implore you to read this and think about what working with a recruiter who knows your industry inside and out for over thirty years can mean for your individual situation. Firms want to capitalize on this deal flow. Harlan publishes a blog every Thursday here.

But what are their implications for capital markets firms? When looking at the concept of Total Enterprise Reinvention in my recent blog , I mentioned that creating compelling technology capabilities—a central digital core—would be key for succeeding in the markets of tomorrow. First, revenue generation.

In my previous blog in this short series on generative AI in capital markets, I gave my perspective on why gen AI is so game-changing for our industry. Here are just a few of the many applications of gen AI that could offer a potential for efficiency gains in capital markets in the operations space.

Here’s a post I recently shared on TheCorporateCounsel.net blog: The Goodwin team that represented the issuer in the first IPO by a traditional venture-backed technology company in more than 18 months recently wrote an alert explaining why the company’s high vote/low vote capitalization structure — which is very common in venture-backed technology (..)

In today’s blog, we’re going to address any issues that potentially come up within the background check. Yes, there’s great movement between firms, but when there is an individual with any sort of character flaws, that will be shared amongst senior capital market individuals; thus, preventing a colleague from making a hiring decision mistake.

Now and then this blog publishes compendiums of bedrock decisions and key principles of which M&A and Corporate Governance practitioners, and their clients, should be aware (e.g., The post Five Delaware Cases All Venture Capital Players Should Know appeared first on Enhanced Scrutiny. here and here ).

Cities, municipalities, special districts, health care, and higher education will always need capital. Harlan publishes a blog every Thursday here. Subscribe to our monthly newsletter here , which is a compilation of our weekly blogs, so you never miss one. That’s what public finance professionals provide.

You can read more about his journey here: [link] To see Agentic AI in action for this post, I hired the blog-writing agent: To write the following section: What is Agentic AI? For VC and PE investors, the rise of Agentic AI presents a massive opportunity to capitalize on the next wave of technological innovation.

Multiple external forces at play… The capital markets industry is no exception. Alongside the forces impacting all sectors, capital markets firms also face a distinct set of sector-specific challenges—economic, technological, client-related and competitive—that are further amplifying the disruption. Far from it.

Among the most critical factors to consider is the capital gains tax rate. An increase in capital gains taxes can directly and profoundly impact the valuation of M&A transactions. Understanding Capital Gains Taxes Capital gains taxes are levied on the profit realized from the sale of an asset held for more than one year.

Read the Entire Blog Piece Where would you rather place to? Private Equity Megafund Growth Equity Venture Capital Hedge Fund Stay in IB Check Out All Our Blog Posts The Path to Success: Building a Thriving Career in Private Equity Congratulations! Prepare well, stay relaxed, and let your confidence shine!

Below, we will explore the role of private equity firms in New York City’s economic landscape, examining their impact on job creation, economic growth, capital allocation, and industry transformation. These firms provide capital, expertise, and strategic guidance to help these businesses grow, expand, and compete on a larger scale.

Today’s blog looks at how to interview with more than one person. With time of the essence, it’s easier to present a panel interview to determine if the candidate is worth using political capital as well as financial capital to get him or her onboard. Harlan publishes a blog every Thursday here.

Venture capital focuses on early-stage companies with high growth potential. VC investors provide capital to startups and small businesses in exchange for equity ownership. These investments are typically made in companies that are seeking capital to fund expansion, acquisitions, or other strategic initiatives.

Below, we will explore the role of private equity firms in New York City’s economic landscape, examining their impact on job creation, economic growth, capital allocation, and industry transformation. These firms provide capital, expertise, and strategic guidance to help these businesses grow, expand, and compete on a larger scale.

Most would say that Private Equity recruiting happens far too early — this year, especially pre-Labor Day On-Cycle 2024 Recruiting started with New Mountain Capital, Carlyle, and Permira, amongst a couple of the initial firms going. Connect with an OfficeHours coach for an update. Because they can get it done.

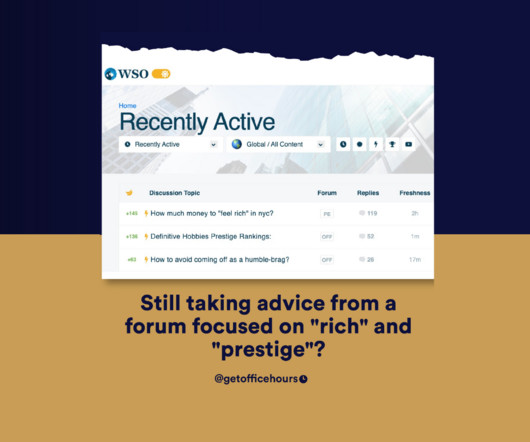

If you’ve ever thought that Buyside might be for you — whether it be Growth Equity, Private Equity, Hedge Funds, Corporate Development, Venture Capital, etc. Learn to interpret anonymous blog critiques as a tool for professional success. Read more blogs Learn how to perform a comprehensive LBO analysis in just a few simple steps!

OfficeHours is an online platform that provides 1-on-1 coaching, training, and advice to help you land a job in competitive finance careers including investment banking , private equity , growth equity , venture capital , and hedge funds. Why You Shouldn’t Take Feedback From An Anonymous Blog Forum For Your Career?

One of the most critical metrics to evaluate the financial health of a target business is its working capital, which measures the company’s operational liquidity. In M&A, working capital is often a significant area of negotiation between the buyer and the seller. What Is Working Capital?

Creativity, color, and fun might not be the first words that spring to mind when you think of capital markets, but I think that’s about to change. Personality matters In recent years, capital markets have learned that digital personality matters. Many capital markets firms could probably compete with big tech firms on compensation.

The experiences consumers expect today rely on unified IT… Read more on Cisco Blogs Over the past few years, connected technologies have shifted into overdrive, causing businesses to reassess their digital infrastructures.

They offer a range of assets, such as Shopify businesses, WordPress blogs, other content sites, and iOS or Android apps. Concept 6: Access to capital is difficult. However, despite all of the tools and resources that Flippa provides, accessing capital is still a difficult process. The blog was sold for $5.2

On Friday 14 August 2009, that is more than twelve years ago, I wrote a little blog post about a fraudulent oil company run by Mr. Massimiliano (Max) Pozzoni. You can find that blog post here. The blog post was titled: Mr Big Wells and the new faster SEC. The name translated from Italian roughly as "Mr Big Wells".

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content