This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

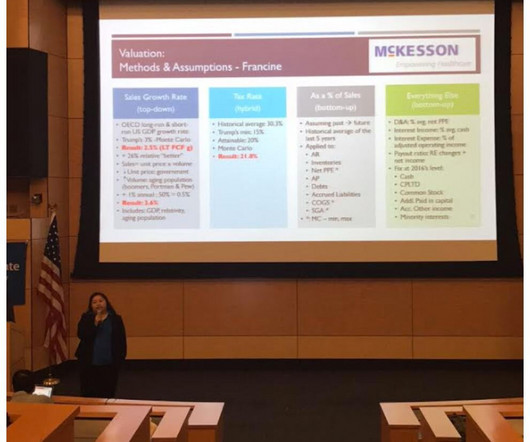

On this very last valuationblog post, I'd like to walk us through a presentation I made back in April 2017 as a part of my master in finance fellowship Capstone presentation. The sound quality is much better this way. I hope you enjoyed the walk through. I appreciate your outreach and will reply as soon as possible!

Thus far, we have covered four popular valuation methods in M&A (DCF, Comparable Company, Precedent Transaction, and LBO) and one less known one that is making its way out of the academic realm into the business world (Dividend Discount Method, DDM). The 2nd valuation method for today is the Liquidation Value method.

As I mentioned in my valuation preparation post , Comparable Company is a valuation method that uses metrics of other similar businesses (same industry, size, geography, valuation multiples, etc.) Calculating the Equity Value and the per-share Equity Value - this number would serve as the base case share price valuation.

As I mentioned in my valuation preparation post , Precedent Transaction is a valuation method that uses the price paid for similar businesses in the past as indicators to a company’s value. The 1st step in Precedent Transaction is to derive the appropriate market multiples (or range of multiples) and control premium for the valuation.

The core element of M&A is company valuation. Strategy, due diligence, financing, purchase price, and buyer-seller alignment all revolve around valuation and the enterprise value for the buyer and the seller. Valuation focuses on two questions: 1. It drives prices, ROI, and financing. What is the company worth?

Just as any home appraiser or credit officer does before going through the analytical exercise to produce a score for a home or a borrower, valuation professionals go through several steps of preparation before the actual exercise of producing a number that can be used as a value of a company. A 5- or 10- year historical data is preferable.

It has been roughly three years since my last blog post at the completion of my fellowship. To pick up where we last left off with valuation, I will cover the topic of a Merger Relative Valuation in this blog post and move on to other non-valuation topics from here. Please send me your thoughts and questions.

Thus far, we have discussed five valuation methods: DCF, Comparable Company, Precedent Transaction, LBO, and Dividend Discount Model (DDM). So, a good valuation model has to take into account the possibilities of a variable having multiple values along with each value’s probability of occurring. To-date, we have lumped them together.

For this valuation post, I wanted to talk about a valuation method that is making its way out of academia and into the real world, a method that is gaining popularity in the world of portfolio management. Because this step is similar in this method as it is in the other valuation methods (DCF, Comparable Company, etc.),

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Calculate the Equity Value and the per-share Equity Value - this number would serve as the base case share price valuation.

Thus far, we have discussed three common valuation methods that most strategic and financial acquirers use when valuing a company for acquisitions or investments. This current post about Leveraged Buy Out (LBO) is about a valuation method used by a very specific type of financial acquirer: private equity (PE) firms.

Thus far in the last 10 blog posts, we have discussed what M&A is, its success metrics, types of acquirers and value creations, capital structure, debt, and equity. In Blog #02 of the M&A series, we discussed SWOT analysis. Consultants’ valuation, deal-structuring, and deal-financing expertise. Any unions?

After the prospective buyers review the CIM and conduct their own preliminary diligence analyses to determine their level of interest and initial valuation of the sale, they will typically solicit internal support for the acquisition. We have discussed the sell-side of an M&A transaction in the last two blog posts.

Peaked market valuations: When market cycle peaks or an industry fully matures, it may be advantageous for shareholders to cash out. Lack of financial / strategic progress: Shareholders’ frustration with the lack of growth of a company’s stock price / dividends / earnings per share / other financial metrics may drive exits.

In this blog, we posit that “before” refers to the “bull market” that ended in January 2022, and “after” refers to everything that – happened, is happening, and will happen – next. History is often written by reference to “before” and “after.” By: Foley & Lardner LLP

Earnouts are perhaps the most contentious of deal terms, and over the years, disputes about earnout provisions have provided us with a rich source of blog topics. Despite all the problems with them, earnouts continue to be a popular tool for bridging valuation gaps.

Valuation lies at the heart of every successful M&A transaction, providing a framework to determine the worth of a target company. Valuation techniques in M&A involve a comprehensive assessment of financial, operational, and market factors. Discounted Cash Flow (DCF) analysis is a commonly used income-based valuation technique.

Valuation is the process of determining the worth of a business, and it plays a pivotal role in M&A transactions. In this blog post, we will dive into different market value methods and strategies used in M&A, shedding light on the secrets to successful M&A transactions.

As you meticulously evaluate financial statements, assess market conditions, and fine-tune your pitch, it’s crucial not to overlook the less conspicuous elements that can significantly influence your business’s valuation in mergers and acquisitions (M&A).

He and the Merit Harbor team work with middle-market business owners looking to grow, acquire or sell companies in the $10mm to $100mm valuation range. With recent high company valuations and other general macro-economic factors, investors need to get far more involved with a company in order to expect any type of fast growth.

Here is a beginner’s guide to understanding valuation for family businesses. Identify Your Valuation Goal: Before getting started, you must identify the overall objective you are trying to achieve with this process. Doing research ahead of time will help determine which valuation methods are best suited for your needs.

Learn to interpret anonymous blog critiques as a tool for professional success. A Few Reads to Digest Valuation Simplified: How Discounted Cash Flow Modeling Drives Financial Analysis Harness Discounted Cash Flow (DCF) modeling for financial analysis. Master valuation, drive decisions, and understand market dynamics.

One aspect that is often talked about and significantly impacts the business landscape is the relationship between interest rates, private equity groups, and business valuations. Impact on Business Valuations: The fluctuation in interest rates not only influences PE activities but also affects how businesses are valued.

In our latest blog installment, we define and outline the key elements involved in valuing a target company. What is Valuation? Valuation can be simply defined as the process of assigning an estimated dollar amount or range to the worth of an item, good, or service.

DO NOT let yourself fall victim to such a ploy – instead, follow the tips outlined below to stand out in the interview process: Understanding the Purpose of an LBO As you have likely heard time and time again, knowing WHY you are using a valuation method is just as important as knowing HOW to use a valuation method.

A widely circulated blog post claiming knowledge of the matter said Wang had been diagnosed with depression, sparking discussion on entrepreneurs’ mental health issues in China’s tech community. With no product, Light Years Beyond had a valuation of $200 million at inception, as noted in one of Wang’s Jike posts.

Imagine crunching historical data to identify potential synergies or using social listening tools to understand brand sentiment – all crucial information for making informed decisions about valuations and deal structures. Valuation Precision: Financial modeling software powered by advanced algorithms can improve valuation accuracy.

In our latest blog installment, we define and outline the key elements involved in the process of raising capital. Yet, taking this equity investment means accepting painful ownership dilution due to the low valuations given to companies at this early stage. So, what's the alternative?

In the dynamic realm of direct-to-consumer (DTC) businesses, a clear hierarchy emerges in private equity valuations, largely based on the perceived stability, scalability, control over supply chains and customer experiences. The hierarchy in DTC business valuations reflects a balance between risk and reward.

In our latest blog installment, we outline the eight basic steps involved in the buy side M&A process and related insights to assist in a successful execution. Establish Preliminary Valuation. As investment bankers, RKJ Partners, LLC possesses a breadth of knowledge and experience in advising buyers on business acquisitions.

Careful preparation and advanced planning can significantly increase the likelihood of a successful business sale and have a positive effect on valuation. Independent Valuation. The following are proactive steps a business owner should take prior to beginning the business sale process: Recasting Financial Statements.

In this blog post, we’ll explore four keys to running a successful M&A due diligence and offer some insights for navigating this complex terrain. Valuation is a fundamental aspect of any M&A deal. However, relying solely on financial models and estimates can lead to inaccurate valuations.

In our latest blog installment, we define and outline the key elements involved in the process of raising capital. For those that do, the amount of stock or warrant received is based on the valuation of the company at the time of the investment. Advisors often take additional compensation in the form of stock or warrants.

In this blog post, we’ll explore how digital transformation is shaping M&A strategies, revolutionizing due diligence processes, and redefining digital asset valuation. Traditional valuation methods, such as discounted cash flow analysis and comparable company analysis, may not adequately capture the value of digital assets.

Furthermore, if the portfolio company’s revenue is not able to increase with or outpace the rate at which inflation is rising, its valuation will ultimately be impacted. Visit the OfficeHours Blog and follow us on our social media accounts: Instagram , LinkedIn , YouTube , TikTok , and Twitter for our latest updates.+

At the junior level, running the model and valuation analyses will be one of your primary workstreams as a private equity professional. To do so, you can either get experience at your job or supplement it by taking relevant courses or certifications on LBO modeling, valuation techniques, and general investment analysis.

Find a Dependable Broker Advisor When selling a small business, a good business advisor is your ally from valuation to closing. Understand the Business’s Value A valuation analyzes a business for its financial worth. Read more about our business valuation process in this blog post.)

It can sometimes happen that you’re hit with a lawsuit after you’ve completed a business valuation. This is incredibly inconvenient because, following valuation, most owners will have already worked out a reasonably just price for the business. Issue #2 Anticipation of a lower price offering. When to Sell a Business.

In a roll-up strategy, a private equity firm will attempt to consolidate a large number of smaller firms into a single, professionalized company with numerous benefits, including economies of scale and fixed cost leverage, valuation uplift (so-called “multiple arbitrage”), and acquisition expertise, among others.

Business valuation, according to the Corporate Finance Institute , is the “process of determining the present value of a company or an asset.”. In this post, we’re going to answer why you need to conduct a business valuation, how you can determine your business value, and how to find the best business valuation specialists.

Situations in which an earnout may apply include: If the price gap between buyer and seller valuation is significant, an earnout can be a reasonable method to bridge this difference based upon actual future results.

Specific Modeling Courses for Various Industries and Stages of Growth While technical proficiency in financial modeling is essential, industry knowledge plays a crucial role in enhancing the accuracy and effectiveness of valuation.

Increase the company’s market valuation. billion to $15 billion and raised the company’s market valuation from $14 billion to $400 billion. Secondly, conducting the business valuation will be less challenging. Why would anyone sell off a part of their business anyway? Well, divesting business units can be advantageous.

Cultural differences, integration difficulties, and valuation discrepancies can complicate the process. Challenges and Considerations While M&A can be a powerful tool for growth and transformation in the digital age, it has its challenges.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content