This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The question was, “Are there positions for lateral partner and counsel moves with and without books of clients today?” I shared that I have more clients than ever looking for that senior attorney (not necessarily partner with or without a book). They are seeing the value of interviewing experienced lawyers without a book.

The New York Times: Mergers, Acquisitions and Dive

JUNE 21, 2023

Two new books offer harsh assessments of private equity firms that specializes in buying up companies only to saddle them with debt and squeeze them for profits.

Ask anyone interested in distressed debt hedge funds for “the pitch,” and they’ll probably mention one of the following: “It’s like long/short equity or credit , but more interesting!” Distressed debt investing offers advantages over other hedge fund strategies , but the marketing often oversells the benefits.

Building a historical 3-statement model and a debt-interest schedule. Building the go-forward debt-interest schedule. Implied Equity Purchase Price = Transaction Value - Debt + Cash. For this table, recall that LBO transactions are heavily financed with debt (it can go up to 90% of the capital structure for some deals).

Calculating cost of debt, cost of equity, and weighted average cost of capital (WACC). While different valuation professionals differ on which multiples to use based on the target’s industry, and so on; a few multiples have became analysts favorites: TEV/Revenue, TEV/EBITDA, and TEV/Tangible Book Value.

The 1st one for today is the Tangible Book Value (TBV) method. TBV is a method often used to establish a low-level valuation for an on-going entity as most companies typically trade for multiples of book value (4Xs TBV or more). The following are common rules of thumb for revaluing the assets: Receivables: at 80-90% of book value.

The concept can be extended to corporation: equity owners (shareholders) own the company alongside debt holders (banks). As we mentioned in the past, equity is the most expensive form of capital (compared to debt with tax-deductible interest). The acquisition will be 100% cash, paid for with debt at 4% interest rate.

Calculate cost of debt, cost of equity, and weighted average cost of capital (WACC). For interest income and expense, I prefer to state them as percentages of the average debt balance of the last two years. It is a good practice to verify the intended debt-vs-total-capital balance post-transaction when possible.

Brooker Kraft was a career soldier who started his own company without writing a book on it. Ali Taraftar left Canada in 2007 to go to the United States and met a couple of investment bankers who put together a firm to do debt restructuring and mortgage modifications.

He explains the concept of open book management and how it can demystify financials for employees. rn Key Takeaways: rn rn Open book management is about demystifying financials and teaching employees how to make money and generate cash.

Barnett is also an accomplished author with multiple books on topics related to investing in local businesses, franchising, and buy-sell strategies, with his latest book set to release in the fall. rn Key Takeaways: rn rn rn Typical leverage for large public companies is between 50-60% debt; anything higher is considered risky.

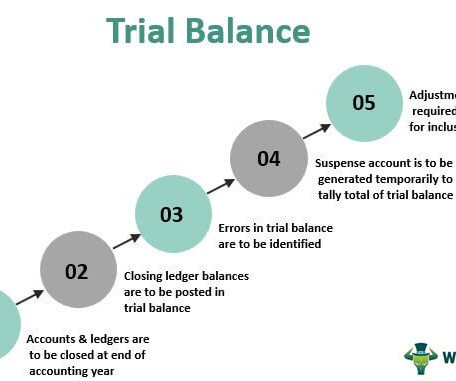

It may also be stated as a statement of the total debit and credit balances extracted from the various accounts in the ledger to examine the mathematical exactness of the books. At the end of every accounting period the accounting books are to be closed and preparing the trial balance is the first step towards it.

Determine Discount Rate: Calculate the discount rate, typically the company’s Weighted Average Cost of Capital (WACC), which reflects the riskiness of the cash flows and the cost of capital from debt and equity sources. This approach provides a clear picture of the company’s worth based on its tangible and intangible assets.

Optimize Working Capital (One Year Ahead) What It Is: Net Working Capital (NWC) is Current assets minus current liabilities (A/R + Inventory A/P + Accrued Expenses), excluding cash, which you keep (in a typical cash-free, debt-free transaction). Consistently book expenses to the appropriate line item.

The slightly low inflow in May compared to the preceding month could be attributed to profit booking. With gold prices still trading at high levels, some investors would have chosen to book profits or take on risk on approach with a view that central banks would pause furthe

You can find the course book here which is a good area to examine an M&A acquistion and how it compares to your fim. Code Quality and Technical Debt Good code should be clean and scalable. Is there a backlog of technical debt that could slow down progress? Everyone has them) Where are the single points of failure?

Lana also co-authored a book about investing in real businesses. The book covers the steps that can be taken to make a business worth buying, such as understanding the market, preparing for the sale, and understanding the legal aspects of the transaction. They work to restructure debt, keep businesses open, and protect personal assets.

In 2018, Walker released his book “By Then Build” which was inspired by this idea. He found a book printing company that was doing eight million in revenue. He wrote a book, By Then Build, and released it in 2018. The book was a success, and Walker was able to gain attention from Forbes.

The lessee records rental payments as expenses in the books of accounts. Since it is an operating lease accounting, the company will book the lease rentals uniformly over the next twelve months, which is the lease term. Since it is an operating lease, ABC Ltd will book the lease rentals uniformly over the next two years.

IFF) has a relatively new debt problem, but its solutions have quickly become old hat. The same month, the company promised more divestitures and operational improvements to reduce debt levels to 3 times Ebitda by 2024 from more than 4.5 International Flavors & Fragrances Inc. DD), nutrition and biosciences, for $26.2

read more is that amount of interest, which is due for a debt or bond but not paid to the lender of the bond. Similarly, a company that has debts in its books will have to report the amount of interest accrued for the bonds it has lent. Still, the same is not received or paid in the same accounting period.

A transaction may start as a debt deal and end up as a hybrid or equity deal, Ramanathan said. I live my life as an open book,” he said. “If You need to be able to be flexible and adapt, and you need the practices to bring to bear that are relevant.” and then to Bain and his unusual candor in talking to potential employers.

Each peer business’ share price, fully-diluted shares outstanding, total debt, total cash, last 12 months (LTM) revenue and EBITDA, book value of equity, and goodwill: Can be obtained from sources such as MarketWatch. longer-term loans (term loans, senior bonds, unsecured debts), and (small portion of) cash on hand.

read more to have parity in the books of accounts of both legal entities. It is required to reconcile the difference between bank balances per bank statement and a bank balance per book of accounts. read more as per bank statement vis-à-vis books of accounts. read more statement is often called a BRS.

And, if somebody else books their time, you could be left high and dry. More on sole traders Sole trade budgeting tips to avoid debt How to scale your business quickly The post Can a sole trader employ staff? A contractor or freelancer may not always have the time or capacity to prioritise your work over their other assignments.

The moves follow the exchange’s launch of a new market-making framework in December last year, aimed at boosting market liquidity, providing depth for order books, and enhancing price efficiency and price formation. The first banks to become market makers for main market stocks were announced earlier this month in quick succession.

Additionally, it is important to ensure that any personal expenses are removed from the books before the business is put up for sale. Additionally, it is important to have the books in order before putting the business up for sale. This includes removing any personal expenses, such as vehicle leases and phone bills, from the books.

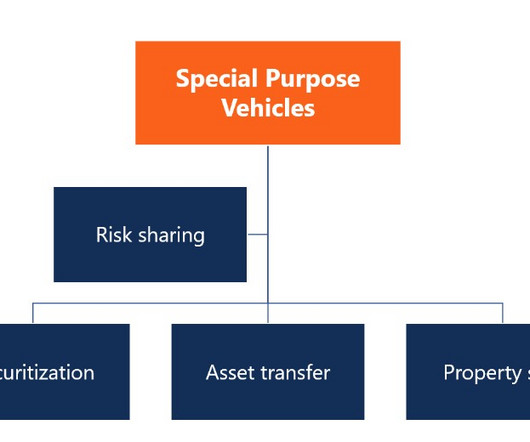

For instance, a company laden with debt could transfer some of it to an SPV, thereby reducing its debt-to-equity ratio. Raising Capital SPVs can also facilitate raising capital for specific projects without raising the parent company's debt levels.

The accounting book reflects that the payments are computed well, managed and cleared out on time. Further, instances of bad debts and defaulters are managed by a corporate accountant. Such responsibility is maintained under corporate accounting.

This is the first time I’ve ever reviewed a book, movie, or TV show multiple times. And yes, there’s even a plot point about debt covenants , of all things. Now it is over. And now I am sad. But unlike Connor Roy at Lester’s funeral , I can write a real eulogy via my final review of this show.

Types The reason for doing Income Tax accounting is arriving at taxable profit and tax payable by making adjustments in the book profit arrived by accounting principles. There are expenses like provision for doubtful debts, which are considered for deduction in accounting in the current year. read more.

You probably couldn't do an ESOP with a small proprietorship because you may not be able to raise the debt involved and there are ongoing expenses to managing an ESOP a business must be able to afford. This tax-exempt status comes into play when structuring and analyzing the debt load the business can carry. continues Beard. “I

A bot might be able to write a term paper, or a song, or even a book, but that bot cannot be considered “intelligent” until it decides by its own volition to write that paper or song or book. In the forward for Gone to Pot, a 2020 book about the early days of the legal cannabis industry, I mentioned “the caravan.”

This helps the buyer to determine how much cash the business will generate and whether they can service the debt to buy the real estate. Another way to achieve success faster is to use the principles outlined in Napoleon Hill's book Think and Grow Rich.

People sell business ownership for a variety of reasons: Needing capital to actually start the company; Swapping equity for additional capital to grow the business; Sourcing money to pay down existing liabilities and debts; Raising venture capital to expand into new markets and; Desiring to diversify their own business risk as the sole owner.

This can be done by paying off as many outstanding debts as possible, renegotiating terms for business loans, securing new clients, and getting your receivables paid up. Once you’ve done this, you can move on to the next step – organizing your books in preparation for business valuation.

Elsewhere, the Cape Town Stock Exchange (CTSE) caters to small to medium -sized businesses, licensed to issue both equity and debt. In certain instances, panellists also noted that if you’re putting flow onto a central order book, there are predatory strategies that will still try to take advantage.

To show your company’s true earnings and book value, we will faithfully recast your financial statements, with an emphasis on removing personal and other non-business expenses that a buyer would not incur. Strengthen your ratios: working capital, debt-to-equity, “quick,” price-to-earnings, return on equity, etc.

The impact of higher interest rates is felt in the form of debt servicing ratios. This is the amount of debt that a business can take on in order to finance an acquisition. When interest rates increase, banks are less likely to provide financing as the debt servicing ratio becomes more difficult to meet.

However, other scenarios, like liquidation, replacement cost, or book value, demand entirely different approaches. Cost of Capital: The cost of capital, a critical factor, combines the cost of equity and debt weighted by the firm’s capitalization. Understanding the premise is the first step towards a successful valuation.

Jim Collins’ book, Built to Last, is a great resource for entrepreneurs looking to create a strong culture that will drive the business forward. Michael Gerber’s book, The E-Myth Revisited, is a great resource for entrepreneurs looking to create a structure that will allow them to scale the business.

rn Concept 6: Tailored Due Diligence Services For Clients rn One key aspect of conducting due diligence is ensuring that the business being acquired is financially stable and can cover its debt. This involves analyzing spreadsheets and considering factors such as the ability to service debt at a lower percentage of current profit or revenue.

Event-Driven Hedge Funds Definition: Event-driven hedge funds bet on specific corporate actions, such as M&A deals, divestitures, spin-offs, bankruptcies, and business reorganizations, and they profit based on changes in the value of a company’s debt or equity after the action.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content