This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

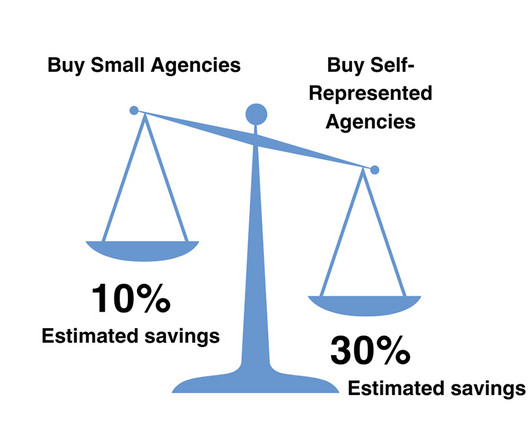

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

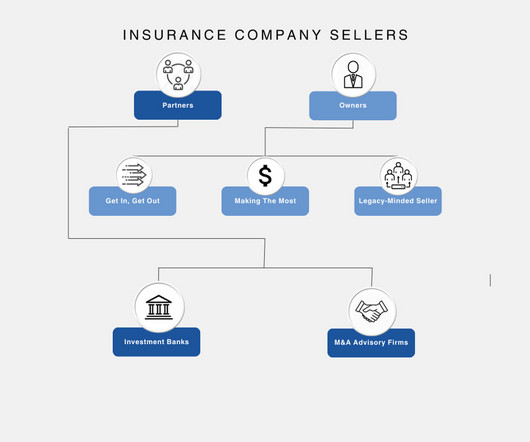

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome. Financial Need. Urgent financial requirements (e.g.,

Remember that, normally, a bank issues loans and then finds the liabilities (deposits, debt, etc.) Deposits up to $250K are insured in the U.S., ” And the FDIC insurance fund will extend to all depositors at SVB and Signature Bank (another failure over the weekend). to back them.

They are thematic investors in fintech (financial services, real estate, insurance) and deep tech (AI enabled transformation, security, IoT), across B2C, B2B and B2B2C businesses. mortgages, insurance) software (e.g. Can provide a mixture of equity and mezzanine debt to businesses mostly at the Series A stage.

Financials are usually in the #1 spot because banks and insurance firms constantly issue debt; other sectors trade places in the rankings. Among the elite boutiques , Moelis has a notable presence, and Rothschild has an office in Mumbai but does not appear to be super-active. Among the bulge brackets, the U.S.-based

A $50 million transaction might include $42 million cash at close (guaranteed), a $5 million seller’s note (where the seller agrees to accept a portion of the purchase price as a series of debt payments), and $3 million in earnouts (which are only paid if the company achieves certain financial metrics over time).

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content