This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In that time, we’ve represented thousands of clients and quickly became one of the most active boutique M&A advisory firms in the market today. The sections below outline what insurance agency investment banks typically provide for clients, to help readers determine whether they are actually needed.

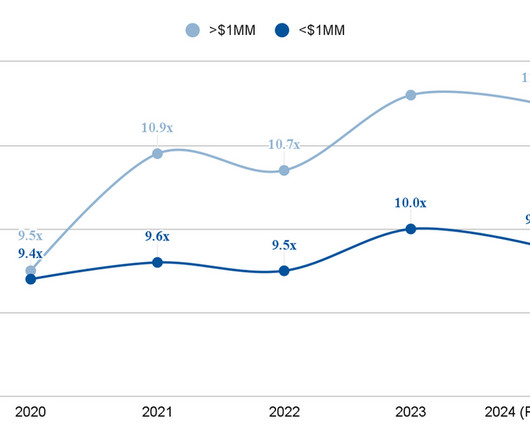

The following report contains our projections for Q3 2024 insurance broker valuation multiples. In addition, we categorize this data according to insurance industry specialization and by brokerage size, as measured by their annual revenue. Since H1 2023, the average insurance brokerage valuation multiple has hovered around 11.6x

Our research team’s latest report compares the top insurance agency investment banks of 2024. Insurance Agency Investment Banks: Investment banks that specialize in the insurance industry. Insurance Agency Investment Banks: Investment banks that specialize in the insurance industry.

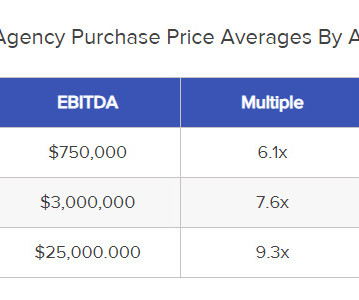

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. We’ll also detail some of the factors affecting these calculations.

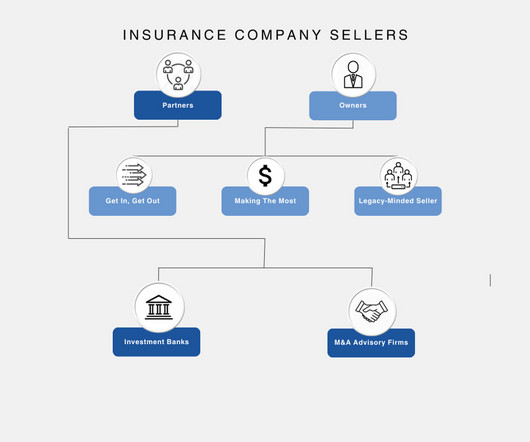

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome.

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

M&A transactions for insurance companies are part of a robust but complicated market that requires ingesting a great deal of data in order to fully understand. While insurance M&A did see slight dips in deal volume and average value (Fig.2) While insurance M&A did see slight dips in deal volume and average value (Fig.2)

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

Benefits: Finally, you’ll get health insurance, vacation days, and potential participation in the firm’s profit-sharing or 401(k) retirement plans. Meanwhile, some elite boutique banks , such as Centerview, went up to $130K for Year 1 Analysts (!). These are useful in the U.S. Investment Banker Salary and Bonus Levels: Analysts.

Insure the Deposits – But this is expensive and is available only up to a certain per-account limit in most countries, such as CHF 100,000 in Switzerland and $250,000 in the U.S. Before this deal, I had expected that “CS First Boston” would become another elite boutique and a strong competitor to the likes of Evercore, Lazard, and Moelis.

TM is the firm’s third acquisition of a boutique specialist since 2018. In May 2018, the privately held subsidiary of Penn Mutual Life Insurance Co. 8, Janney made a splash with a deal for New York-based middle market investment bank TM Capital Corp., which has a focus on founder-led and family business clients.

Prior to joining TD, he was president and chief executive of London Life and London Insurance Group. The Group said the move will help it to reap the benefits of a “global multi-boutique model” as well as a global distribution team in asset management.

billion provision for long-term care insurance claims, which was excluded from its adjusted EBITDA. If the company is not an FX boutique or exchange, FX gains and losses typically are not part of the company's EBITDA. GE: In 2017, GE made a $6.2

Deposits up to $250K are insured in the U.S., ” And the FDIC insurance fund will extend to all depositors at SVB and Signature Bank (another failure over the weekend). And the middle-market and boutique investment banks don’t have much presence in commercial lending anyway, so they’re not at risk of bank runs.

They are thematic investors in fintech (financial services, real estate, insurance) and deep tech (AI enabled transformation, security, IoT), across B2C, B2B and B2B2C businesses. mortgages, insurance) software (e.g. They invest in verticals that include marketplaces (e.g. deposits, lending, tax, auto, legal), security (e.g.

Financials are usually in the #1 spot because banks and insurance firms constantly issue debt; other sectors trade places in the rankings. Among the elite boutiques , Moelis has a notable presence, and Rothschild has an office in Mumbai but does not appear to be super-active. or Europe and recruiting there.

If representation & warranty insurance is available but the buyer instead requires an escrow to cover breaches of representation of warranties or a shortfall in net working capital delivered at closing, suddenly the deal could be worth less than you may have originally anticipated.

Delving into the how, Mark Austin, pension and insurance executive, EMEA, at Northern Trust, highlighted that these reforms should eventually allow pools of LGPS and DC assets to become more self-determined in terms of the oversight of their managers and the oversight of their assets against their liabilities.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content