This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We have spent the last few posts looking at debt and it can be useful to a corporate borrower; as well as negative impacts debt can pose to the capital structure. There are many different kinds of debt providers: banks, bondholders, hedge funds, etc. Low debt level implies high WACC. High debt level implies lower WACC.

To be explicitly clear, I am recommending the use of the following ranked capital sources when paying for an acquisition: cash (from the balance sheet), debt (at a reasonable level), and equity. Similarly, not all corporate debt instruments are created equal and each comes with pros and cons.

Private equity is an investment asset class that has gained significant prominence and popularity in recent decades. However, private equity can seem complex and intimidating to beginners who are unfamiliar with its fundamentals. The Different Types of Private Equity Firms Private equity firms come in different sizes and strategies.

Whether, as part of the management of your startup, you are tasked with driving an equity or debt financing to closing or with gearing up for an exit event, disclosure schedules will be one of the many documents that you will negotiate and deliver as part of your deal.

In recent years, private credit has emerged as an important financing source for corporations of all kinds, especially for private equity-owned businesses with high financial leverage. Under this structure, banks typically provide committed financing to buyers (in this case, often private equity firms).

Any structural elements that affect the equity value: Typically includes differences between public vs. private valuations, minority vs. control premiums, insider ownership, sizeable equity offerings, etc. Do they have the cash of debt/equity capacity to bid aggressively? What will someone pay for the company?

In the pursuit of attractive equity returns, private equity firms have developed numerous innovative strategies beyond typical leveraged buyouts and take-private transactions. As it happens, this is an industry that has experienced a significant amount of private equity-backed roll-up activity.

By Michael Goodwin on Growth Business - Your gateway to entrepreneurial success Many entrepreneurs’ burning question when considering investment for growth is how much equity to give away. To determine the value of the shares specifically, you need to adjust for the debt and cash in the business.

Let’s start with the elephant in the room: yes, we’ve covered the growth equity case study before, but I’m doing it again because I don’t think the previous examples were great. minutiae about issues like OID for debt issuances ) and did not accurately represent a 1- or 2-hour case study. They over-complicated the financial model (e.g.,

For private equity investors who have been monitoring the situation around inflation for the last few months to a year, many have been disappointed to see the slow trajectory with which inflation has been coming down from highs. Explore the role of private equity now. Currently, inflation in the U.S.

Based in West Palm Beach, Florida, Catera will continue to help lead the investment team and focus on structuring, negotiating and advising portfolio companies on debt and equity financings. The post Siris promotes Catera to partner appeared first on PE Hub.

A term sheet is often used in the early stages of negotiating a venture capital investment or M&A transaction. Since SEG often helps facilitate term sheet discussions, we’ll also share some practical guidance on how to negotiate them and a term sheet template to show you what they look like. What is a Term Sheet?

He explains that when the Small Business Administration (SBA) looks at a business for a loan, they want to make sure that the business can cover its debt service. They do this by giving it a coverage ratio of one dollar and thirty-five cents for every dollar of debt service after certain expenses.

And there may be intense negotiations concerning this number that could delay the closing or impact how much you ultimately take away from the deal. For that reason, it can pay to learn more about NWC, what it might or might not include, and how an M&A advisor can help you negotiate more favorable terms to maximize your proceeds.

Capital is generally grouped into three main classifications: Senior Debt, Mezzanine Capital and Equity Capital. Most entrepreneurs are very familiar with senior debt offered by traditional banks. Senior debt is first in seniority and is often secured by collateral in the form of a lien.

However, for private equity investors, this uncertainty represents a unique opportunity to take advantage of investment opportunities in public markets. A “take-private” transaction in the context of private equity is a process by which a PE firm acquires a publicly listed company and converts it into a privately held entity.

If it makes financial sense and you understand the dilution aspect of selling equity and the potential interference from investors, then yes, go ahead. In this post, we’re going to address what these are, some of the challenges to expect, how to sell the equity, and who to sell it to. Selling equity – the good, the bad, the ugly.

Making equity dollars last is particularly important since they come at a high price. Although the price is high, these precious equity dollars are often a critical factor in an emerging company's success. There is no question that in today's fundraising environment, capital efficiency is paramount.

A local business broker can be invaluable in identifying opportunities, assessing the business’s financial health, and negotiating on your behalf to ensure a smooth transaction. General Partnerships In a general partnership, all partners are responsible for managing the business and are equally liable for debts and legal obligations.

This concept is called rollover equity and is common for private equity transactions. What is Rollover Equity? The offer of ongoing ownership is known as “rollover equity” because the seller chooses to roll a portion of the sale proceeds back into the company’s new ownership structure. How Does Rollover Equity Work?

Since that post, the Delaware Chancery Court has had the opportunity to consider some preliminary issues relating to certain of those jeopardized transactions involving private equity-backed buyers.

The terms of the agreement are set out in a term sheet signed by both of the parties, and it is anticipated that a definitive agreement regarding the transaction will be negotiated and entered into in due course. TORONTO, Feb. As described in greater detail below, ABR is a related party of the Company.

By Dom Walbanke on Growth Business - Your gateway to entrepreneurial success Raising private equity funds is seen as the holy grail for businesses who want to grow quickly, simply because the strength of capital opens the door for rapid growth.

Debt Financing: The Double-Edged Sword Debt financing is a standard route for companies pursuing M&A, offering the allure of leveraging existing assets to fund the transaction. High debt levels can burden the newly formed entity with interest payments, impacting its financial flexibility.

Negotiation Skills Negotiation is an art in itself. Be prepared to negotiate favorable terms to your side while ensuring a mutually beneficial outcome. Good negotiation skills can save you money and reduce post-acquisition conflicts. Debt Financing Debt financing involves borrowing money to fund the acquisition.

Concept 3: Equity in Exchange For Value Equity in exchange for value is a concept that has become increasingly popular in recent years. For consultants, equity in exchange for value can be a great way to increase their income and build wealth. By using our skills and experience, we can help others and ourselves reach our goals.

Negotiating interest rates, equity stakes, and purchase prices is a delicate process that involves convincing the other party that your terms are reasonable and beneficial. Negotiating Interest Rates Interest rates play a pivotal role in the financing of a business acquisition.

Concept 4: Leverage Debt For Multiple Expansion Leveraging debt for multiple expansion is a strategy used by private equity firms to increase their value and profitability. This strategy is used by private equity firms to purchase a platform business, scale it up, and then acquire other ancillary businesses in the same industry.

Venture capitalists Venture capital is finance provided for an equity stake in a potentially high growth company, and is behind some of the best know and most innovative businesses in the UK such as Pizza Express, Centre Parcs, Odeon, UCI cinemas and Spotify. More on venture capital backing How do you know it’s time to raise venture capital?

Private Equity Investment: Private equity firms can be strategic partners for mid-sized businesses looking to finance M&A transactions. In exchange for an equity stake in the company, private equity investors provide capital to fund acquisitions and support growth initiatives.

They act as intermediaries between buyers and sellers, helping to facilitate negotiations, conduct due diligence, and ensure a smooth transition. Whether it is in a specific industry or as a generalist, a skilled advisor can provide valuable insights, facilitate negotiations, and ensure a successful outcome.

Earnouts in M&A deal negotiations are a vital tool, offering sellers of fast-growing companies potential extra compensation and providing buyers with a risk-reduction method. However, negotiations hit a snag when the seller proposed retaining total operational control during the earnout period.

In the US, it is common to adjust the purchase price for cash, any excess or deficit of net working capital relative to a required level of net working capital, unpaid debt, and unpaid transaction expenses of the target business as of the closing, with an adjustment done at closing based on estimates and followed by a post-closing true-up.

It serves as a starting point for negotiations and helps both parties understand the structure of the proposed transaction. As such, it is subject to change and revision during the negotiation process, and the final agreement may differ in some respects from the original term sheet. Thanks, , Pratik S

Virtu’s Triton Valor EMS provides us with a single view that brings together all our workflows including electronic RFQs, automated execution, and negotiated trading and provides us with tools to aggregate real-time feeds, liquidity sources and valuable pre-trade analytics to make trading decisions faster and with confidence.

The funds generated from the sale can be used to finance the M&A transaction, invest in growth opportunities, or pay down debt. This strategy involves a business, private equity owner, or sponsor selling its company-owned real estate that is considered mission-critical to its operations.

With higher interest rates, the same cash flow of years past now supports a lower amount of balance sheet debt. Also buyers like to use mezzanine and senior bank debt. The equity check writer will walk away in these cases because they can’t make the return on equity that they seek without the debt. Next, 12.8%

In addition to the high cost of debt interfering with their bottom line, they also have to contend with a buyer pool that’s larger than ever before , with 50+ buyers in the current pool where there used to be ~5. Although sellers are in a good position to sell, they need to be wary of the equity that’s being offered.

Equity Investment: Seek equity investment from reputable investors with experience in the renewable energy sector and who are comfortable with regulatory uncertainties. Debt Financing: Explore options for debt financing, such as loans from local or international banks, multilateral development banks, or export credit agencies.

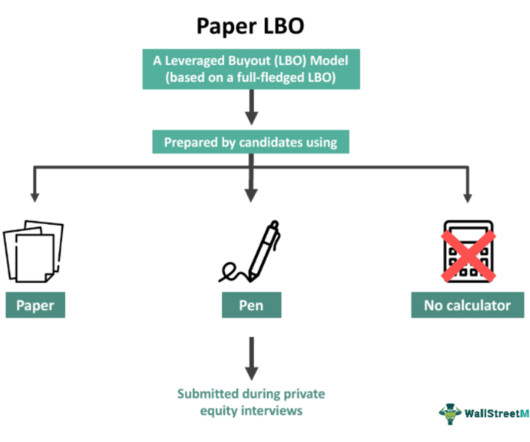

A Paper LBO, also called a Pen and Paper LBO, usually prepared by candidates during private equity interviews, is a miniature paper version of a full Leveraged Buyout (LBO) Model. Further, it helps interviewers assess a candidate’s knowledge of private equity concepts. Determine the mix of debt and equity required to finance the deal.

The seller’s counsel is responsible for negotiating the key legal terms of the purchase agreement. Using an experienced M&A attorney is critical to move the transaction forward while avoiding costly legal fees negotiating on terms that are not critical. The terms of the earn-out can be negotiated with your advisor and buyers.

Lower margins, in many cases, make these businesses unattractive to all but a small handful of financial investors like private equity groups, who look to invest, build a company up and then often sell to a larger private equity group. And by the way, this valuation is always negotiated. continues Beard. “I

By following these guidelines, businesses can make informed decisions, negotiate favorable terms, and mitigate risks to maximize the value of their M&A transactions. It helps the acquiring company to make informed decisions and negotiate the deal’s terms and conditions. Don’t have time to read it now?

That is especially true when the buyer is a private equity group or other type of “financial” buyer, which is the case in seven out of 10 deals that we have closed over the last several years. Strengthen your ratios: working capital, debt-to-equity, “quick,” price-to-earnings, return on equity, etc.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content