This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Additionally, liquidity is important for governments because it gives them access to debt markets to sell securities to fund deficits. Further, liquidity is important to help funds of all types managerisk and improve market stability. One tool for riskmanagement is hedging.

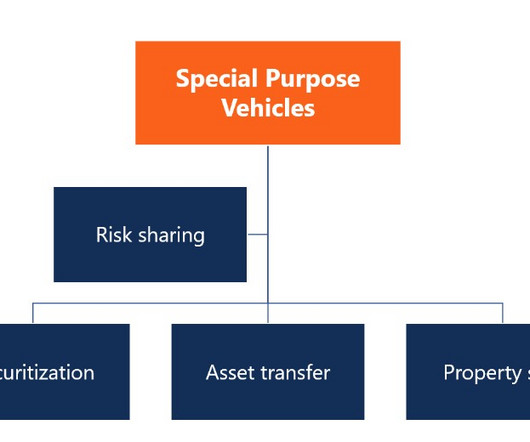

In the event of the parent company's bankruptcy, the SPV remains solvent, and its obligations are not affected. RiskManagement Companies utilize SPVs as a riskmanagement tool by transferring assets and liabilities associated with particular risks to the SPV.

Remember that, normally, a bank issues loans and then finds the liabilities (deposits, debt, etc.) Banks are now incentivized to be even more reckless in their “riskmanagement” since they know this backstop exists. Why bother managing your regulatory capital if the government will save you when too many loans default?

These legacy systems are entrenched in manual processes and siloed data, resulting in costly errors and expensive technical debt. In contrast, Clear Street is building a unified platform using cloud-native, event-driven, and horizontally-scalable technology. This API-first approach lets us seamlessly add new capabilities.

Key Components of an M&A Risk Assessment 1. Create contingency plans for high-impact risks: Develop detailed action plans for responding to riskevents. Engage in ongoing communication with functional areas to gather risk-related information. Use dashboards and reporting tools to visualize risk data.

Debt and liabilities: assess the company’s debt levels and liabilities to determine whether it can manage its obligations during economic uncertainty. Management team: evaluate the management team’s experience and track record to determine whether it can lead the company through difficult economic times.

Professional networks and industry events: Leverage your professional networks and attend industry events to gather insights and identify potential targets. Identify any potential financial risks or red flags. Assess the potential risks or challenges associated with integrating the two companies.

Key Components of an M&A Risk Assessment 1. Create contingency plans for high-impact risks: Develop detailed action plans for responding to riskevents. Engage in ongoing communication with functional areas to gather risk-related information. Use dashboards and reporting tools to visualize risk data.

Principles of Natural Law in Finance In the world of finance, three primary principles derived from Natural Law play a crucial role: Universality : Just as laws like gravity apply everywhere, certain principles in finance, such as risk and reward, are universally recognized. Rationality: Making decisions based on reason and not emotion.

read more that gives the buyer the privilege to swap or transfer the credit risk to the third party. The Credit default swap helps to transfer the credit risk Credit Risk Credit risk is the probability of a loss owing to the borrower's failure to repay the loan or meet debt obligations.

As Jean-Charles Sambor, head of emerging market debt at TT International Investment Management tells The TRADE: “The emerging markets fixed income sphere is recovering, and we expect inflows back to the asset class after years of investor exodus.” But, of course, there is more to come, and the market is prepping.

RiskManagement and Loan Loss Reserves Lending money is a risky business. Provisioning for Bad Debts: Banks use sophisticated models to predict the amount of loan defaults they might experience in a given period. Not all borrowers will pay back, and banks have to be prepared for these eventualities.

After an initial consultation, the private banker assesses John’s financial situation and develops a customized wealth management plan. It also offers investment banking services such as equity underwriting, mergers and acquisitions, debt restructuring, and capital raising.

In a wider sense, Basel III impacted financial market by promoting greater stability, resilience, and riskmanagement within the banking sector. This has resulted in a range of operational and legal challenges, as well as potential basis risk between Libor and RFR-based contracts.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content