This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To be explicitly clear, I am recommending the use of the following ranked capital sources when paying for an acquisition: cash (from the balance sheet), debt (at a reasonable level), and equity. Similarly, not all corporate debt instruments are created equal and each comes with pros and cons.

In addition to its equity investment alongside World's existing backer Charlesbank, Goldman Sachs is also leading debt financing in World. The post Goldman Sachs to invest in insurance brokerage World Insurance Associates appeared first on PE Hub.

What is generally less understood is the impact of the pandemic on the debt markets. What is going on in these markets could potentially have significant implications for insurance brokerage M&A, and we want you to understand why. We can see the impact in the debt markets very clearly. to 10.0%.

What Is Medical Debt ? Medical Debt refers to a financial obligation incurred by an individual due to unpaid bills for medical services obtained from a healthcare provider. The debt may be owed directly to a healthcare provider or a third-party agent, such as a collection agency, that bought the debt.

The following report details insurance brokerage M&A multiple averages for H1 2024. Our research team averaged the information using data from our Sica | Fletcher index, which monitors approximately 70% of insurance sector transactions. Because several kinds of insurance are legally required (e.g.,

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

What is a Collateralized Debt Obligation? Table of contents What is a Collateralized Debt Obligation? How does Collateralized Debt Obligation (CDO) Work? CDOs provide investors with a diversified portfolio of debt instruments across different risk levels. read more , etc.

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

In it, we provide readers with a quick and simple overview of the current insurance brokerage M&A market , after which we discuss several macroeconomic and industry-specific factors that could drastically affect transactions in the next six months. The market is already highly competitive, but it’s also limited to what buyers can afford.

In particular, new guidelines from the FDIC and Federal Reserve (among other governmental agencies) made it more difficult for banks to underwrite financings that resulted in debt-to-EBITDA ratios in excess of 6.0x. This capital is released once investors buy the debt off the banks’ balance sheets.

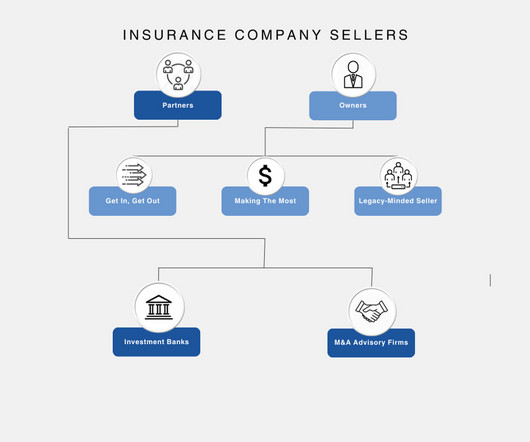

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome. Financial Need. Urgent financial requirements (e.g.,

For owners and executives of private insurance brokers, Brown & Brown's first quarter earnings call provides a treasure trove of information. insurance brokers. Powell Brown, President and CEO of Brown and Brown Insurance commented: “The first quarter was an interesting one until early March. billion of debt given the 6.0x

Many of our clients have asked us about the impact on insurance brokerage M&A of the pandemic and the resultant containment efforts. The Largest Strategic Players Tell Us Full Steam Ahead – The major strategic acquirors have informed us that they plan to continue to aggressively pursue acquisitions of insurance brokers.

From a financial planning point of view, venture loans can be an attractive insurance policy. If there's risk that critical milestones may slip, having the ability to borrow and extend runway so those milestones can be safely achieved insures a trip to the equity fundraising market with a better valuation.

What the Data Is Telling Us In our last few posts, we reported on what we perceived to be the trends in insurance agency and brokerage M&A in light of the pandemic and analyzed the reasons for these trends. They have enormous amounts of dry powder that they must deploy and continue to have access to very inexpensive debt.

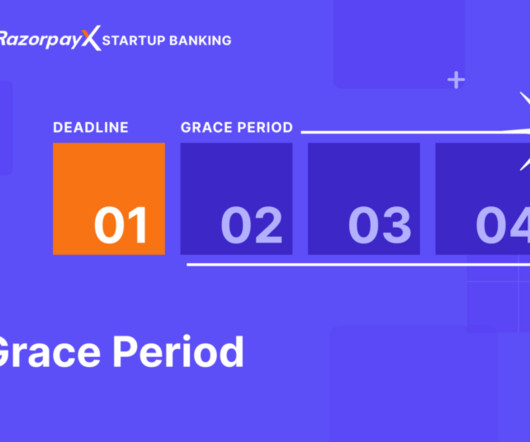

A grace period is the time after the due date of an obligation, typically a loan or insurance contract, during which payment can still be made without penalty. A grace period gives a borrower or insurance customer time to make a delayed payment even beyond the due date without late fees, penalties or cancellation of the contract or loan.

stake in Singapore Life Holdings and two debt instruments to Sumitomo Life for a combined 800 million pounds ($997 million), the British insurer said on Wednesday. Aviva to sell Singlife joint venture stake for $1 billion By Elizabeth Howcroft LONDON (Reuters) -Aviva is quitting its Singlife joint venture, selling its 25.9%

Update on Private Equity and Insurance Brokerages In our ,, previous article , we reported that the COVID-19 pandemic had not diminished the pace of mergers and acquisitions transactions we are seeing in the insurance agency and brokerage sector. However, insurance brokerages remain relatively unscathed from the fallout.

You will need employers’ liability insurance, provide payslips, and manage payroll, though the last two here can be outsourced if you wish. More on sole traders Sole trade budgeting tips to avoid debt How to scale your business quickly The post Can a sole trader employ staff? appeared first on Growth Business.

Acquiring companies need to understand the target’s digital capabilities, potential technology debts, and how well their systems integrate with their own. Consider cyber insurance as an added layer of protection. Data Analytics Integrating advanced data analytics tools has transformed how companies approach M&A.

1,00,000 1% 2% 194D Payment of insurance commission to domestic companies Rs. 15,000 NA 10% 194D Payment of insurance commission to companies other than domestic ones Rs. 15,000 5% NA 194DA Maturity of Life Insurance Policy Rs. 1,00,000 1% 2% 194D Payment of insurance commission to domestic companies Rs.

This acquisition further expands our growing distribution network by over 500 clients, including banks, insurance companies, private debt funds, mutual funds and private wealth managers,” said Anthony Di Ciollo, global head of fixed income at StoneX. Fixed income broker Octo Finances is in Paris.

Insurance Agency & Brokerage M&A Update Many of our clients have been asking us “now that the first phase of the coronavirus pandemic seems to be ending, where do things stand with insurance brokerage M&A?” As a result, they had and continue to have large pools of equity and debt capital to deploy in acquisitions.

In recent posts, we outlined the background of and reasons for the dramatic upsurge of private equity investment in the insurance brokerage industry , how the combination of private equity and low interest rates have dramatically raised valuations , and how private equity sponsored agencies increasingly dominate the insurance agency business.

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. If these add up to more than the company’s Distributable Cash Flow, it issues additional Debt to cover the difference: This setup seems simple, but it’s probably the #1 most common mistake in the DDM.

“We are seeing an increasing number of providers of this type of loan facility in the market,” said Todd Davison, MD of Purbeck Personal Guarantee Insurance. – What is venture debt? Merchant cash advances have been around since 1998, but they’ve made their mark on the alternative finance industry since.

The acquisition of Conning, which has extensive long-standing insurance and institutional client base in the US and Asia, will also expand Generali’s remit in those regions and its capabilities across fixed income, structured and corporate credit, emerging market debt and private real estate.

Develop a risk mitigation strategy for each identified risk, such as structuring contracts to minimize exposure to regulatory changes or securing political risk insurance. Debt Financing: Explore options for debt financing, such as loans from local or international banks, multilateral development banks, or export credit agencies.

Excessive Debt: High levels of debt relative to the industry or the inability to service debt comfortably can severely constrain the company’s financial flexibility. Weak Supply Chain: Reliance on unstable or single-source suppliers can disrupt operations and increase risk.

It’s also the second Black-founded unicorn in the UK, and co-founders and brothers Oliver and Alexander Kent-Braham, along with CTO David Goaté have set their sights on disrupting the insurance industry. Since its launch in 2015, Marshmallow has offered affordable options to those who have recently moved to the UK.

Example of Merchant Banking In 2021, merchant bank Avendus Capital helped the Indian company Piramal Enterprises acquire the debt-ridden assets of Dewan Housing Finance Corporation (DHFL) for ₹34,250 crore ($4.4 They help companies to raise capital in the form of debt or equity. It allows easy accounting software integration.

Optimize Working Capital (One Year Ahead) What It Is: Net Working Capital (NWC) is Current assets minus current liabilities (A/R + Inventory A/P + Accrued Expenses), excluding cash, which you keep (in a typical cash-free, debt-free transaction). Why It Matters: Healthy working capital keeps the business running smoothly day-to-day.

Offerings like the RazorpayX payroll facility enables businesses to automate payments in advance, offer insurance plans to employees and streamline business operation. Further, instances of bad debts and defaulters are managed by a corporate accountant.

Debt and liabilities: assess the company’s debt levels and liabilities to determine whether it can manage its obligations during economic uncertainty. What is the target company’s current debt position, and what is their plan for managing any potential financial risks that may arise due to the economic uncertainty?

Examine debt and credit history. Investigate these aspects to grasp the company’s borrowing history and current debt obligations and gauge financial risks. Review insurance coverage. Examine tax returns for several years to identify any discrepancies or issues. Verify accounts receivables and payables.

The lender, in this case, who buys the instrument has to pay the premium like that of an insurance policy, in exchange of which the seller of the instrument will compensate for the loss in case of default faced by the buyer of the instrument from their borrower. The payment continues till the maturity of the agreement.

Some of the common fixed costs are employee salaries, interest, rent, insurance, lease, insurance, utility payments, phone service, advertising costs, amortization, and more. Tip 2: Conduct research and choose insurance plans that come with lower premiums. Tip 3: Opt for refinancing of debt to minimize interest rate.

Credit Risk Mitigation: Strategies such as credit insurance, stringent customer vetting, and proactive receivables management can help mitigate the risks associated with credit sales. Bad Debt Management: Estimating the likelihood of non-payment and accounting for bad debts is crucial for providing a realistic view of financial health.

Strengthen your ratios: working capital, debt-to-equity, “quick,” price-to-earnings, return on equity, etc. As examples: Make sure your inventory and asset records align with what is physically there.

Debt underwriting had its best week since May 2011 and equity underwriting also improved significantly while M&A activity was quite light Equity underwriting volumes of $17.2 Corporate debt underwriting volumes of $98 billion nearly tripled from the prior week. billion of net outflows in 3Q11. Announced M&A volumes of $16.6

Debt underwriting was again a highlight in the week while completed M&A volumes also improved Equity underwriting volumes of $15 billion declined by 61% from the prior week, though last week’s volumes were boosted by the Treasury’s $20 billion offering of AIG stock. Corporate debt underwriting volumes of $90.2

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content