This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

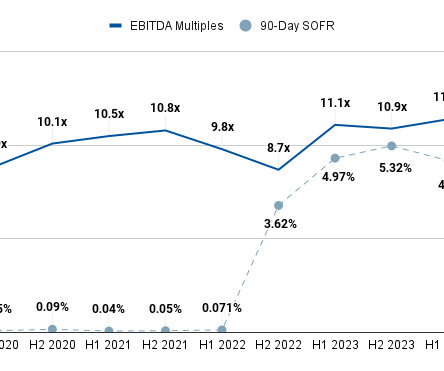

The following report details insurance brokerage M&A multiple averages for H1 2024. Our research team averaged the information using data from our Sica | Fletcher index, which monitors approximately 70% of insurance sector transactions. Because several kinds of insurance are legally required (e.g.,

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

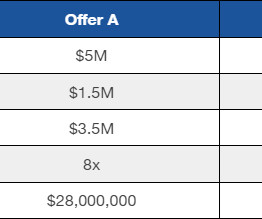

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

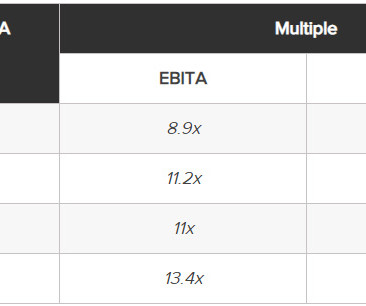

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

What is a Collateralized Debt Obligation? Table of contents What is a Collateralized Debt Obligation? How does Collateralized Debt Obligation (CDO) Work? CDOs provide investors with a diversified portfolio of debt instruments across different risk levels.

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. And Equity Real Estate Investment Trusts (REITs) must distribute almost all their Net Income, so the DDM can work well in REIT valuations. But outside of those, its status is murkier.

In it, we provide readers with a quick and simple overview of the current insurance brokerage M&A market , after which we discuss several macroeconomic and industry-specific factors that could drastically affect transactions in the next six months. The market is already highly competitive, but it’s also limited to what buyers can afford.

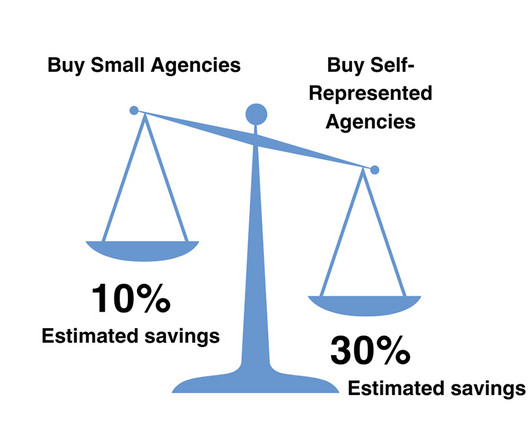

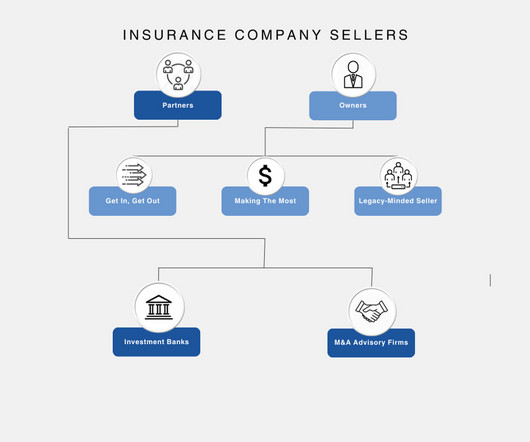

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome. Financial Need. Urgent financial requirements (e.g.,

Yet, taking this equity investment means accepting painful ownership dilution due to the low valuations given to companies at this early stage. From a financial planning point of view, venture loans can be an attractive insurance policy. So, what's the alternative?

Many of our clients have asked us about the impact on insurance brokerage M&A of the pandemic and the resultant containment efforts. The Largest Strategic Players Tell Us Full Steam Ahead – The major strategic acquirors have informed us that they plan to continue to aggressively pursue acquisitions of insurance brokers.

Update on Private Equity and Insurance Brokerages In our ,, previous article , we reported that the COVID-19 pandemic had not diminished the pace of mergers and acquisitions transactions we are seeing in the insurance agency and brokerage sector. The number of transactions we are working on has not abated. The question is, “Why?”.

Optimize Working Capital (One Year Ahead) What It Is: Net Working Capital (NWC) is Current assets minus current liabilities (A/R + Inventory A/P + Accrued Expenses), excluding cash, which you keep (in a typical cash-free, debt-free transaction). These are called addbacks, and are extremely important to valuation.

In recent posts, we outlined the background of and reasons for the dramatic upsurge of private equity investment in the insurance brokerage industry , how the combination of private equity and low interest rates have dramatically raised valuations , and how private equity sponsored agencies increasingly dominate the insurance agency business.

Insurance Agency & Brokerage M&A Update Many of our clients have been asking us “now that the first phase of the coronavirus pandemic seems to be ending, where do things stand with insurance brokerage M&A?” As a result, they had and continue to have large pools of equity and debt capital to deploy in acquisitions.

It’s also the second Black-founded unicorn in the UK, and co-founders and brothers Oliver and Alexander Kent-Braham, along with CTO David Goaté have set their sights on disrupting the insurance industry. And it’s fair to say that for a while some private market valuations became inflated, with predictable consequences for some.

billion valuation by 2030. The first step in positioning your HVAC business for a favorable acquisition is increasing its current valuation. This can be done by paying off as many outstanding debts as possible, renegotiating terms for business loans, securing new clients, and getting your receivables paid up.

The lender, in this case, who buys the instrument has to pay the premium like that of an insurance policy, in exchange of which the seller of the instrument will compensate for the loss in case of default faced by the buyer of the instrument from their borrower. The payment continues till the maturity of the agreement.

Subtract the cash outflows from payments like salaries, dividends, rent, insurance, loan repayment, stock repurchase, taxes, etc. Unlock the art of financial modeling and valuation with a comprehensive course covering McDonald’s forecast methodologies, advanced valuation techniques, and financial statements.

Some of these are banks, NBFCs, investment companies, brokerage firms, insurance companies and trust corporations. It refers to the possibility that the lender may not receive the debt's principal and an interest component, resulting in interrupted cash flow and increased cost of collection.

To do this, he obtained his insurance and securities licenses and started helping developers raise money. As the economy trends towards recession, debt becomes more expensive, making it harder for small businesses to sell. Initially, the company was looking for a valuation of ten million dollars.

Remember that, normally, a bank issues loans and then finds the liabilities (deposits, debt, etc.) Deposits up to $250K are insured in the U.S., If you’re familiar with bank accounting, valuation, and regulatory capital (i.e., to back them. but less than 10% of accounts at SVB were in that category (an unusually low percentage).

Despite investment in the first half of 2023 dropping to £4.6bn from 2022’s £10.8bn as a result of rising interest rates, high inflation, a decrease in valuations and geopolitical tensions globally, UK fintechs are still attracting more VC investment than all other EMEA fintechs combined, with a significant percentage coming from US investors.

There’s also continued insurance challenges and a whole lot more. That valuation depending on how you look at it, boils down to 193% of sales or about 15 times EBITDA. We’ll talk about valuations when we start to talk about selling a little bit. This is a tough business. It’s a big company.

Any stock-for-stock combination of two companies with relatively similar valuations is typically referred to as a merger of equals transaction, and even some stock-for-stock acquisitions where the “acquirer” is valued significantly higher than the “target” share some key elements of a merger of equals transaction. 2.

The client should be familiar with how to work with the professionals, such as lawyers, CPAs, and business valuation companies. Finally, creative insurance products may also be available, but this is an area that requires expert advice and research.

PE refers to a form of investment where institutional investors—such as pension funds, mutual funds, and insurance companies—as well as wealthy individuals, provide capital to PE firms. Lower borrowing costs will make debt-financed acquisitions more attractive, further driving the consolidation of the industry. to 6x EBITDA on average.

Financial risks: credit risk, liquidity risk, market risk, and valuation issues. Risk Mitigation: Develop strategies to mitigate or manage each identified risk: Implement financial hedging and insurance solutions for financial risks. Key Components of an M&A Risk Assessment 1.

Financial risks: credit risk, liquidity risk, market risk, and valuation issues. Risk Mitigation: Develop strategies to mitigate or manage each identified risk: Implement financial hedging and insurance solutions for financial risks. Key Components of an M&A Risk Assessment 1.

“Be clear on your strategy to investors and the type of investor you are looking for, i.e. investors that can provide strategic input and/or opportunities to help grow and develop the business by way of technology or distribution,” said Todd Davison, MD of Purbeck Personal Guarantee Insurance. Here’s where you could get funding.

Financial Role You will need to have very clean books, records and financials as well as a bullet-proof valuation of your business – the purchase price. For example, a buyer may not assume a debt or take over a piece of real estate. As such, your accountant or CFO has to be part of the exit team. This is rare but it does happen.

Concept 3: Document and insure Ownership One of the most important elements of planning for sale is to document and insure ownership. In addition to documenting ownership, it is also important to insure ownership. This means that it is important to have a clear understanding of the business and the contracts that are in place.

Appraisal / Valuation Real estate appraisal is the process of valuing a property, which is essential when it is being sold. But it’s also important when a commercial real estate loan refinancing occurs, as the amount of new debt is based on the property’s value. However, you do not necessarily need full-time experience (i.e.,

Reference any deals you’ve worked on that required analysis of these points and talk about how they affected the valuation or client’s decisions (this is more grounded than just saying, “I like high-growth companies!”). Notice how “price” and valuation are not on this list. Q: Why growth equity?

Highlighted below are some of the key areas where we expect to see more nuanced negotiations and heightened scrutiny during the course of an M&A transaction as a result of COVID-19’s impact: Purchase Price Adjustments/Valuation. Insurance coverage. Cybersecurity.

Matt Stoller has an excellent article summing up the companys problems , but the short version is that it came under severe margin pressure due to pharmaceutical pricing : Health insurance companies in the U.S. Excluding operating leases (which Capital IQ incorrectly adds to Net Debt for U.S. So, what is Sycamores plan?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content