This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Privateequity is an investment asset class that has gained significant prominence and popularity in recent decades. However, privateequity can seem complex and intimidating to beginners who are unfamiliar with its fundamentals. Privateequity firms also invest in distressed debt or provide privatedebt financing.

In recent years, private credit has emerged as an important financing source for corporations of all kinds, especially for privateequity-owned businesses with high financial leverage. The growth of private credit can be traced back to the Great Financial Crisis of 2008-2009.

In the pursuit of attractive equity returns, privateequity firms have developed numerous innovative strategies beyond typical leveraged buyouts and take-private transactions. As it happens, this is an industry that has experienced a significant amount of privateequity-backed roll-up activity.

To be explicitly clear, I am recommending the use of the following ranked capital sources when paying for an acquisition: cash (from the balance sheet), debt (at a reasonable level), and equity. Similarly, not all corporate debt instruments are created equal and each comes with pros and cons.

For privateequity investors who have been monitoring the situation around inflation for the last few months to a year, many have been disappointed to see the slow trajectory with which inflation has been coming down from highs. Explore the role of privateequity now. Currently, inflation in the U.S.

By Dom Walbanke on Growth Business - Your gateway to entrepreneurial success Raising privateequity funds is seen as the holy grail for businesses who want to grow quickly, simply because the strength of capital opens the door for rapid growth.

However, for privateequity investors, this uncertainty represents a unique opportunity to take advantage of investment opportunities in public markets. A “take-private” transaction in the context of privateequity is a process by which a PE firm acquires a publicly listed company and converts it into a privately held entity.

A term sheet is often used in the early stages of negotiating a venture capital investment or M&A transaction. Since SEG often helps facilitate term sheet discussions, we’ll also share some practical guidance on how to negotiate them and a term sheet template to show you what they look like. What is a Term Sheet?

He explains that when the Small Business Administration (SBA) looks at a business for a loan, they want to make sure that the business can cover its debt service. They do this by giving it a coverage ratio of one dollar and thirty-five cents for every dollar of debt service after certain expenses.

To determine the value of the shares specifically, you need to adjust for the debt and cash in the business. Where you end up in the range (or if you are on outlier outside that) depends on the nuances of your business and the investment process you are running.

And there may be intense negotiations concerning this number that could delay the closing or impact how much you ultimately take away from the deal. For that reason, it can pay to learn more about NWC, what it might or might not include, and how an M&A advisor can help you negotiate more favorable terms to maximize your proceeds.

Concept 4: Leverage Debt For Multiple Expansion Leveraging debt for multiple expansion is a strategy used by privateequity firms to increase their value and profitability. For example, one of the most popular industries for leverage debt for multiple expansion is the collision repair industry.

Since that post, the Delaware Chancery Court has had the opportunity to consider some preliminary issues relating to certain of those jeopardized transactions involving privateequity-backed buyers.

Capital is generally grouped into three main classifications: Senior Debt, Mezzanine Capital and Equity Capital. Most entrepreneurs are very familiar with senior debt offered by traditional banks. Senior debt is first in seniority and is often secured by collateral in the form of a lien.

They act as intermediaries between buyers and sellers, helping to facilitate negotiations, conduct due diligence, and ensure a smooth transition. Whether it is in a specific industry or as a generalist, a skilled advisor can provide valuable insights, facilitate negotiations, and ensure a successful outcome.

PrivateEquity Investment: Privateequity firms can be strategic partners for mid-sized businesses looking to finance M&A transactions. In exchange for an equity stake in the company, privateequity investors provide capital to fund acquisitions and support growth initiatives.

In the US, it is common to adjust the purchase price for cash, any excess or deficit of net working capital relative to a required level of net working capital, unpaid debt, and unpaid transaction expenses of the target business as of the closing, with an adjustment done at closing based on estimates and followed by a post-closing true-up.

With higher interest rates, the same cash flow of years past now supports a lower amount of balance sheet debt. Also buyers like to use mezzanine and senior bank debt. The equity check writer will walk away in these cases because they can’t make the return on equity that they seek without the debt. Next, 12.8%

This concept is called rollover equity and is common for privateequity transactions. These types of deals have become common, particularly when the buyer is a privateequity firm. While taking equity in any business comes with a risk, a rollover equity offer can present a significant upside for the seller.

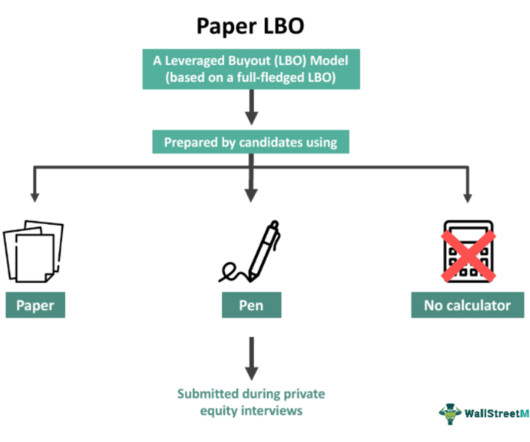

A Paper LBO, also called a Pen and Paper LBO, usually prepared by candidates during privateequity interviews, is a miniature paper version of a full Leveraged Buyout (LBO) Model. Further, it helps interviewers assess a candidate’s knowledge of privateequity concepts. What Is A Paper LBO?

Lower margins, in many cases, make these businesses unattractive to all but a small handful of financial investors like privateequity groups, who look to invest, build a company up and then often sell to a larger privateequity group. And by the way, this valuation is always negotiated. continues Beard. “I

Equity finance Equity finance involves raising capital for a business by selling shares of ownership to investors in exchange for funding. Unlike debt financing, which involves borrowing money that must be repaid with interest, equity financing does not require repayment. What is a venture capital term sheet?

Just because you are getting lots of inquiries from PrivateEquity and other investors, it does not mean you are ready to sell. Focusing your efforts on improving those metrics will make your company more attractive and give you a leg-up in negotiations. If your numbers aren’t up to snuff, you’d be wise to wait.

Just because you are getting lots of inquiries from PrivateEquity and other investors, it does not mean you are ready to sell. Focusing your efforts on improving those metrics will make your company more attractive and give you a leg-up in negotiations. If your numbers aren’t up to snuff, you’d be wise to wait.

The seller’s counsel is responsible for negotiating the key legal terms of the purchase agreement. Using an experienced M&A attorney is critical to move the transaction forward while avoiding costly legal fees negotiating on terms that are not critical. The terms of the earn-out can be negotiated with your advisor and buyers.

In addition to the high cost of debt interfering with their bottom line, they also have to contend with a buyer pool that’s larger than ever before , with 50+ buyers in the current pool where there used to be ~5. Sellers are remaining patient and working with M&A advisosr to identify areas of opportunity. Changes in the buyer pool.

In reaching this order, the court applied the prevention doctrine, finding that the unavailability of buyer’s debt financing did not permit buyer to circumvent its obligation to close because buyer materially contributed to the debt financing being unavailable. All of those demands were rejected by the lenders.

The funds generated from the sale can be used to finance the M&A transaction, invest in growth opportunities, or pay down debt. This strategy involves a business, privateequity owner, or sponsor selling its company-owned real estate that is considered mission-critical to its operations.

People sell business ownership for a variety of reasons: Needing capital to actually start the company; Swapping equity for additional capital to grow the business; Sourcing money to pay down existing liabilities and debts; Raising venture capital to expand into new markets and; Desiring to diversify their own business risk as the sole owner.

That is especially true when the buyer is a privateequity group or other type of “financial” buyer, which is the case in seven out of 10 deals that we have closed over the last several years. Strengthen your ratios: working capital, debt-to-equity, “quick,” price-to-earnings, return on equity, etc.

You can negotiate to retain your salary and benefits throughout the transition. With a leveraged management buyout, the buyer or seller can opt to bring on board a third party in the form of a privateequity firm (PE), venture capitalist (VC), or conventional lender. The business is plunged into debt.

The History of PrivateEquity in Insurance One of the primary forces differentiating the insurance M&A market in 2024 from those of decades past is the presence and dominance of privateequity (PE) firms in the buyer space. It used to be the case that equity structures consisted of senior debt (i.e.,

While there are a few public investment opportunities in the heavy-duty parts and service sector, such as Dorman Products (NASDAQ: DORM) and Ryder Systems (NYSE: R), many investors have turned to PrivateEquity (PE) for investments in the industry. are all on the table to be negotiated.

Let’s start with the elephant in the room: yes, we’ve covered the growth equity case study before, but I’m doing it again because I don’t think the previous examples were great. minutiae about issues like OID for debt issuances ) and did not accurately represent a 1- or 2-hour case study. They over-complicated the financial model (e.g.,

However, he also connects clients with M&A attorneys who can help with drafting an LOI, negotiating closing deals, and other legal aspects of the transaction. rn Ronald shares what he's seeing as the behavior of privateequity firms in the current market.

Big Tech, is often much more susceptible to broader economic swoons and who may rely more heavily on debt for acquisitions, has seen a significant slowdown so far this year in deals over $1 billion in size, with only 15 in the third quarter. The first area of bifurcation is between the large cap and middle market Tech M&A markets.

They stress the need to clearly communicate expectations from the beginning of negotiations, avoiding surprises later on. Finally, the guests discuss the current market trends in privateequity and capital raising. Privateequity firms, strategic buyers, and even competitors are all cautious in their investment decisions.

It is very common for problems and issues to pop up during due diligence, so it’s important to stay proactive and be open to negotiation until the deal is finalized.” Such reports are increasingly common in larger transactions, especially where the buyer is a privateequity firm. “A

Typically, the buyer will be a privateequity or even a partner in your business Asset Purchase This is the most common type of sale where a buyer will buy out all the assets and liabilities of your company. They may exclude some assets and/or liabilities based on mutual negotiations. You will be entitled to interest.

His firm assists a range of clients from first-time acquirers to privateequity firms. This democratization of acquisition financing heralds a maturation phase for e-commerce M&A, bringing a wave of new entrants who can scale their operations rapidly with the backing of judicious debt. Great investment."

However, deal activity fizzled in the second half of 2022, as high inflation, aggressive anti-inflation monetary policies, geopolitical instability, assertive antitrust regulators and tightening financing markets depressed target valuations, reduced strategic acquirer confidence and sidelined privateequity sponsor buyers. trillion. [2]

While people obsess over investment banking and privateequity, other sectors within finance, such as commercial real estate (CRE) , often go ignored. Tasks include getting tenants to renew their leases, negotiating new terms, and handling unit repairs, maintenance, renovations, and new HVAC installations.

Thats why taking the time to put together a compelling narrative for your business before the process gets under way should be a non-negotiable. For a privateequity buyer, we focus on those who have experience in the broader space or with businesses whose business models are similar to yours. For them, its about synergy.

Consumer retail privateequity is so diverse that it almost seems like a paradox. Depending on the firm, a consumer retail privateequity deal might consist of: A leveraged buyout of a struggling offline retailer. On the Job Recruiting Should You Go Shopping for Consumer Retail PrivateEquity Jobs?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content