This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Just as any home appraiser or credit officer does before going through the analytical exercise to produce a score for a home or a borrower, valuation professionals go through several steps of preparation before the actual exercise of producing a number that can be used as a value of a company.

As I mentioned in my last post, Discounted Cash Flow (DCF) is a valuation method that uses free cash flow projections, a discount rate, and a growth rate to find the present value estimate of a potential investment. Calculate cost of debt, cost of equity, and weighted average cost of capital (WACC).

To pick up where we last left off with valuation, I will cover the topic of a Merger Relative Valuation in this blog post and move on to other non-valuation topics from here. A discussion of the target’s financials typically starts with the P/L or Income Statement, followed by the Balance Sheet, and then the Cash Flow Statement.

The Verdict is In on the Sell Side: Business Valuation Basics By Brian Goodhart Valuation is a fundamental aspect of the complex and intricate world of mergers and acquisitions. Today, we will delve into the intricate art and science of valuation, exploring its various components and purposes.

Accurate and appropriate valuation is one of the pillars of maximizing the profits from a business sale. It’s integral to ensuring that the sale benefits all stakeholders and should be one of your priorities before advertising it to potential buyers.

middle market valuation multiples and deal volume are down slightly through Q2 of 2023. The S&P 500 Index is up 16.5% this year through June 2023, but middle market valuations are down approximately 8% based on the TKO Miller analysis. Packaging Trends Q2 M&A Update U.S.

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. In other words, you profit based on the company’s dividend s and the potential increases in its stock price over time. But outside of those, its status is murkier.

Corporate structure Whether youre a C-Corp or S-Corp can affect taxes at sale. Optimize Working Capital (One Year Ahead) What It Is: Net Working Capital (NWC) is Current assets minus current liabilities (A/R + Inventory A/P + Accrued Expenses), excluding cash, which you keep (in a typical cash-free, debt-free transaction).

A profit and loss (P&L) statement, sometimes called as an income statement, is a financial report that provides investors and outsiders with a financial overview of a company. The P&L outcome plotted on a trendline assists investors in understanding the organization’s performance over time.

Financial Modeling & Valuation Courses Bundle (25+ Hours Video Series) –>> If you want to learn Financial Modeling & Valuation professionally , then do check this Financial Modeling & Valuation Course Bundle ( 25+ hours of video tutorials with step by step McDonald’s Financial Model ).

Other times, they are hoping to use their share of the sale to alleviate personal debt. Once you get into the valuation stage (which is usually done by your M&A advisor or a 3rd party valuation agency), you will need a large swath of documentation. Manageable Debt. Are looking for a career change.

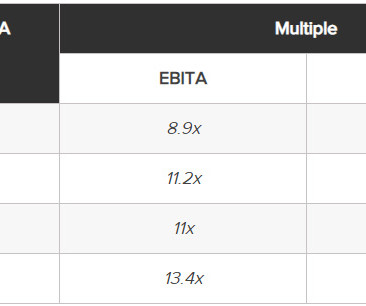

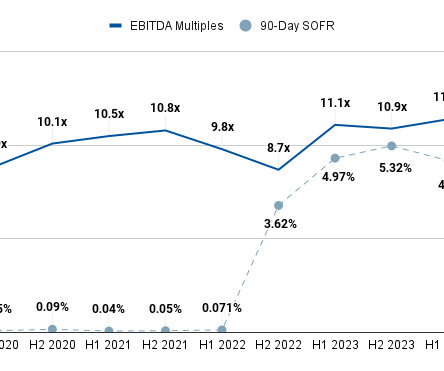

Starting in H2 2022, the insurance M&A market has seen a notably difficult 18-month period, afflicted with high interest rates, lowered deal volumes, and lowered valuations. If they do, then we can expect to see valuations and, by extent, EBITDA multiples for insurance agencies rise. Learn more at , ,, SicaFletcher.com.

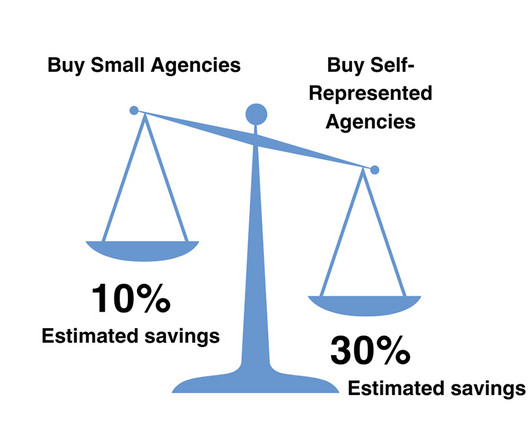

In addition to the high cost of debt interfering with their bottom line, they also have to contend with a buyer pool that’s larger than ever before , with 50+ buyers in the current pool where there used to be ~5. Sellers are remaining patient and working with M&A advisosr to identify areas of opportunity.

The S&P 500 has recently traded near 4800, close to its record at the end of 2021. While the company generated over $260 million in revenues through the first three quarters of 2023, its stock price is trading under a dollar a share, as the company is burdened with substantial debt. As 2024 starts, the U.S.

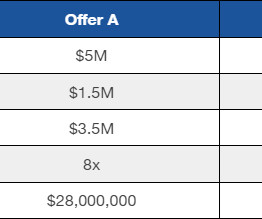

essentially boils down to three major steps: Determine your insurance agency’s EBITDA Determine the standard valuation multiple for an agency of your size Multiply your EBITDA by the multiple to determine your expected payout (i.e.,

While the cost of debt has increased to the point that buyers often acquire brokerages at an initial loss, insurance brokerage M&A multiples have not only held steady but are actually seeing all-time highs. Equity used to consist of senior debt (i.e., This means brokerages are generating more revenue now than ever before.

They might have separate teams for specific strategies or markets, but everything is run under a single Profit & Loss statement (P&L). There are very few real “requirements” besides the single PM / single P&L one above and the standard Limited Partner / General Partner structure that all hedge funds use.

About Loan [P*R*(1+R)^N]/[(1+R)^N-1] Wherein, P is the loan amount R is the rate of interest per annum N is the number of period or frequency wherein loan amount is to be paid Loan Amount (P) The loan Amount $ ROI per annum (R) Rate of Interest per annum % No. How to Calculate? Each of such points cost 1% of the loan amount.

PE firms rely on leveraged buyouts (LBOs) for the lion's share of their deals, which often involve using the acquired company’s assets as collateral to insure the loan used to purchase it. Conversely, when interest rates are high, valuations are supposed to decrease because buyers will try to make up what they are losing to interest.

It quickly became uneconomical for exploration and production companies to keep on drilling, meaning there was no need for the equity and debt capital that was typically raised on a quarterly basis. The same thought process can be used when deciding whether it makes sense to take out debt or instead finance an expenditure with your savings.

They have their investment thesis and valuation, and the earnings announcement is the event that unlocks value… …but this is not what “event-driven” means in most cases. But if we’re wrong, and the spin-off doesn’t happen or gets done at a lower valuation, the parent company’s share price would fall by only 10%.”

Since H2 2022, industries across the board (including insurance) have seen declines in deal volume as prospective buyers have withheld their funds for more favorable conditions in which the cost of debt is not so high. Consult data sources like S&P Global data to get an idea of a firm’s activity within the industry.

In the early days of institutional private equity, many industrial companies were perceived to be stable, cash-flow-generation machines with significant hard assets that could be used as collateral for debt. billion with Debt of $2.1 No Debt has been repaid, so the Exit Equity Proceeds are $3.6 billion – $2.1 billion = $1.5

personal debt, business/legal liabilities, time-sensitive investment opportunities) may prompt owners to sell quickly. Your agency valuation will play a large role in influencing how buyers perceive your agency’s worth. Financial Need. Urgent financial requirements (e.g., Market/Business Environment.

Metals & Mining Investment Banking Definition: In metals & mining investment banking, professionals advise companies that find, produce, and distribute base metals, bulk commodities, and precious metals on debt and equity issuances and mergers and acquisitions. What Do You Do as an Analyst or Associate in the Group?

Equities and the S&P 500 At the onset of each new year, like clockwork, we’re asked for our near-term view. benchmark equity index, the S&P 500. Consequently, by the end of July 2023, the S&P was up more than 20% for the year. This year was no different.

Sports Investment Banking Definition: In sports IB, bankers advise on equity and debt issuances, mergers, acquisitions, and restructuring deals for sports teams and leagues, sports-adjacent technology and services firms, and facilities such as arenas, stadiums, and racetracks. What is Sports Investment Banking?

This happened for a few reasons: 1) Soaring Valuations – Many sources say that sports team valuations “outperformed” the S&P 500 over the past 20 years, which is a polite way of saying that many teams are now valued at extremely high multiples. only a handful a decade ago). Examples include Ares (now with a $3.7

As the world headed into the uncharted territory of a worldwide pandemic, investors in both debt and equity markets reacted to shifts and changing conditions in several interesting ways, and the lessons they learned and the actions they take this year will set the stage for everyone’s access to capital in the years to come.

This includes examining the company’s financials, contracts, and other documents that will help them to determine the value of the business. Having the right documents in place, such as an operating agreement, P&Ls, meeting minutes, and resolutions, can make the process of selling the business much smoother and easier.

2023’s much-discussed downturn in mergers & acquisitions – with global M&A volume and value down 6% and 17%, respectively, from 2022 – was largely driven by the slowdown in the tech sector, with global tech M&A volumes down 51% year over year, while other sectors saw marked increases. [1] in 2022 to 5.9x

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content