This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In recent years, private credit has emerged as an important financing source for corporations of all kinds, especially for privateequity-owned businesses with high financial leverage. The growth of private credit can be traced back to the Great Financial Crisis of 2008-2009. What impact has this had on privateequity?

Compared to other medical fields like dentistry and dermatology, privateequity involvement in orthopedic practices has been relatively small. Scale can also allow practices to negotiate better contracts with insurers and get better deals on supplies and equipment.

We are seeing an increasing amount of privateequity entering the veterinary space, both at the clinic level and the pet product level. During times of economic uncertainty, people tend to look for something safe and secure to invest in. making it highly competitive to get into.

For top privateequity firms, there’s a lot to like about SaaS. And it typically boils down to a few common elements that successful SaaS companies do particularly well: High-quality SaaS companies feature predictable, recurring revenues, solid unit economics , and high gross margin and gross profit rates.

After all, we are still faced with the COVID pandemic, now in an economic environment with the highest inflation we have experienced since the 1980s, and likely increases in interest rates. Will we see transaction multiples at last year’s levels? Or will the multiples decrease?

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

M&A transactions for insurance companies are part of a robust but complicated market that requires ingesting a great deal of data in order to fully understand. While insurance M&A did see slight dips in deal volume and average value (Fig.2) While insurance M&A did see slight dips in deal volume and average value (Fig.2)

While representation and warranty (R&W) insurance continues to be used across a broad range of M&A transactions, its use has cooled as dealmakers navigate challenging market conditions. As deal flow has dwindled, competition has increased among carriers, and minimum floors largely have fallen away. of the policy limit.

What is going on in these markets could potentially have significant implications for insurance brokerage M&A, and we want you to understand why. While we can’t predict the future, our certainty level regarding the impacts on insurance brokerage M&A has increased over the past several weeks. billion at yields between 5.1%

Many of our clients have asked us about the impact on insurance brokerage M&A of the pandemic and the resultant containment efforts. The Largest Strategic Players Tell Us Full Steam Ahead – The major strategic acquirors have informed us that they plan to continue to aggressively pursue acquisitions of insurance brokers.

Kip, an experienced M&A attorney, shares his expertise on how business owners can prepare their companies for acquisition by privateequity firms and strategic buyers, ensuring they are poised for a successful exit. Expect thorough negotiations even if it's a smaller deal, especially with a privateequity buyer."

Update on PrivateEquity and Insurance Brokerages In our ,, previous article , we reported that the COVID-19 pandemic had not diminished the pace of mergers and acquisitions transactions we are seeing in the insurance agency and brokerage sector. The number of transactions we are working on has not abated.

What the Data Is Telling Us In our last few posts, we reported on what we perceived to be the trends in insurance agency and brokerage M&A in light of the pandemic and analyzed the reasons for these trends. Privateequity firms continue to drive transaction pace and value.

Think from the perspective of a privateequity player (even if your deal was not a PE deal), and implement important facets such as cash flow generation, ability to add leverage, growth levers, a strong management team, and a business that operates in an attractive, large, and growth industry. Make sure you have your story down cold!

Insurance Agency & Brokerage M&A Update Many of our clients have been asking us “now that the first phase of the coronavirus pandemic seems to be ending, where do things stand with insurance brokerage M&A?” Insurance brokerage businesses can normally be viewed as predictable, basically “annuity-like” cash flows.

Many of these causes have their equivalences to the reasons behind the sale of a company (also known as a divestiture): Liquidity: As the equity holding period matured, investors (privateequity funds behind companies) will look to sell.

Unsought Products Items consumers do not generally think of buying but purchase due to sudden events or perceived needs , like insurance or funeral services. MetLife, a leading insurance company, falls into this category.

On April 23 a group led by privateequity firm TPG agreed to acquire OneOncology, the nation’s largest independent community oncology network, in a deal valued at $2.1 While the biggest recent deal, OneOncology is hardly the first oncology platform to be sold to a privateequity group. But if you've got a [PE] backer.

It is important to understand the different types of buyers that may be interested in the business, such as privateequity, family offices, strategic acquisitions, competitors, and strategic partners. For example, privateequity companies are looking for businesses that they can ultimately sell to a strategic buyer.

If you're interested in breaking into finance, check out our , PrivateEquity Course and , Investment Banking Course , which help thousands of candidates land top jobs every year. Fixed Costs are expenses that remain constant, such as rent, salaries, and insurance. This may simply be the price of the unit.

They are thematic investors in fintech (financial services, real estate, insurance) and deep tech (AI enabled transformation, security, IoT), across B2C, B2B and B2B2C businesses. mortgages, insurance) software (e.g. They invest in verticals that include marketplaces (e.g. deposits, lending, tax, auto, legal), security (e.g.

While there are a few public investment opportunities in the heavy-duty parts and service sector, such as Dorman Products (NASDAQ: DORM) and Ryder Systems (NYSE: R), many investors have turned to PrivateEquity (PE) for investments in the industry. In other words, they look for businesses that are resilient during economic downturns.

If you're interested in breaking into finance, check out our PrivateEquity Course and Investment Banking Course , which help thousands of candidates land top jobs every year. This approach requires careful consideration to ensure that reported revenues accurately represent economic reality.

The Importance of Brokerages in the Financial Ecosystem Economic Function Brokerages provide liquidity to the market by connecting buyers and sellers. If you're interested in breaking into finance, check out our PrivateEquity Course and Investment Banking Course , which help thousands of candidates land top jobs every year.

Q: Why not privateequity, growth equity, hedge funds, or entrepreneurship? A: For this one, you should find highly specific markets – such as P&C insurance technology rather than “fintech” – and argue that others have overlooked them for reasons X, Y, and Z, but they could potentially create billion-dollar startups.

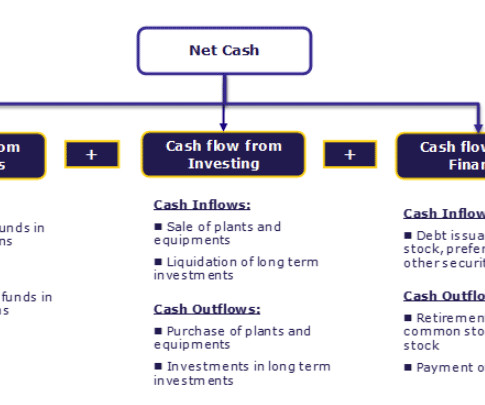

Further, statement of cash flow analysis is essential for corporate planning in the short run Short Run A Short Run in economics refers to a manufacturing planning period in which a business tries to meet the market demand by keeping one or more production inputs fixed while changing others. In 2015, Box came up with its IPO.

If you're interested in breaking into finance, check out our PrivateEquity Course and Investment Banking Course , which help thousands of candidates land top jobs every year. Reduced Paid-Up Insurance: Allows the policyholder to apply the cash value towards a fully paid-up policy with a reduced benefit.

Equity purchase Here you sell the equity of your business. It could be a 100% equity purchase or a minority or even a majority equity purchase. In this section you should discuss about the conditions of your industry – impacts of legal, regulatory, political, technological, economic and environment on your business.

As we have reported throughout the year, the M&A market for insurance brokers remained at peak, pre-pandemic levels despite all of the public health, political, social, and economic dislocations. S&P reported that the number of insurance brokerage transactions closed in 2020 slightly exceeded those in 2019.

This site has already covered investment banking interview questions , privateequity interview questions , and venture capital interview questions , so the next topic on the list seemed to be growth equity interview questions. Q: Why growth equity?

So of course insurance companies were not happy with it and customers were not happy with, with the cycle time. If it’s, if it’s help with getting paid and, you know, it’s talking to the insurance companies to, to make sure that they can get their claims processed properly. We, we get involved in that.

Consumer retail privateequity is so diverse that it almost seems like a paradox. Depending on the firm, a consumer retail privateequity deal might consist of: A leveraged buyout of a struggling offline retailer. On the Job Recruiting Should You Go Shopping for Consumer Retail PrivateEquity Jobs?

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content