This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Traditional banks that don’t prioritise digital inclusion face being left behind By Laura Rae co-founder of Openbox, a premium digital experience partner to the financialservices industry It’s not so long ago that every financialtransaction we wanted to make involved leaving the house and physically handing over notes and coins.

Businesses have financial needs, too. They need to store money, avail loans and manage finances just like individuals. Regular retail banks provide financialservices to individuals but are not equipped to service businesses. Working capital loans provide financing for the daily operations of a business.

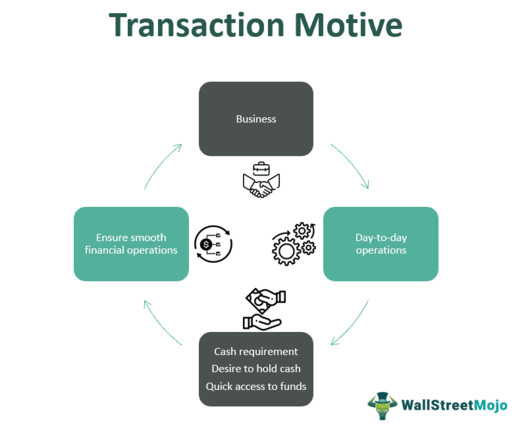

What Is A Transaction Motive? Transaction motive refers to the desire to hold cash to facilitate everyday cash-based financialtransactions such as business and personal needs, covering payroll, purchases, and bill payments. Two major factors drive its functioning: the level and frequency of transactions.

E-banking/Electronic banking allows us to perform financialtransactions and other operations online seamlessly. What are the services provided by E-banking? E-banking allows lesser manual/desk work and even reduces the risk of human error since all financial operations are digital. Let’s discuss how.

Current accounts are just as liquid as regular savings deposit accounts but do not earn as much interest, since the main purpose of a current account is to facilitate convenient transactions, and not earn interest income. Business Banking Services: For businesses, current accounts often come with additional features tailored to their needs.

A key aspect of Mifid II, is the expansion of transparency requirements, namely in the trading of financial instruments. It mandates increased pre- and post-trade transparency for a wide range of asset classes, including equities, fixed income, derivatives, and structured finance products.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content