This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, one common point across all the verticals is that IPOs are not common because there aren’t that many publicly traded sports teams, stadiums, or arenas. SPAC IPOs for esports companies were “hot” for a short period in 2021, but they seem to have died off by now.

During the hold period, the private equity firm can improve operations, management structure, and financial strategies to optimize the business. Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank.

During the hold period, the private equity firm can improve operations, management structure, and financial strategies to optimize the business. Once improved, the exit can then take place, usually in the form of another sale or an Initial Public Offering (IPO), both of which are usually under the advice of an investment bank.

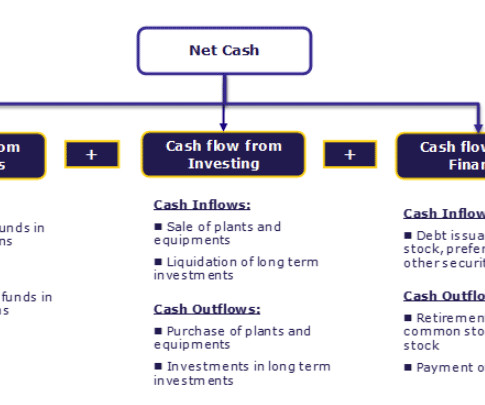

The investing activities comprise the long-term asset purchase or sale. Add to it all the incoming cash from various sources like cash sale of goods or services, proceeds from the sale of assets or investments, the funds acquired by the issue of shares or through bank loans, etc.

They over-complicated the financialmodel (e.g., They invest when companies already have revenue (like PE firms), but they do so by purchasing minority stakes , holding them, and selling in an IPO or M&A exit (like VC firms). So, you can think of this example and tutorial as “Growth Equity Case Study: The Final Form.”

This style is about purchasing minority stakes in cash-flow-negative-but-high-growth companies that want to scale and eventually go public or sell (think: Uber or Airbnb before their IPOs). In the 2010s, startups began to postpone their IPOs, but they still needed funding. There’s usually a long list of previous VC investors as well.

There is some overlap because at the large banks, wealth management clients often get early/privileged access to investment banking products, such as upcoming IPOs, equity/debt offerings, or new investment products. Think: benchmarking portfolios rather than modeling companies. and without a target school or great internships.

In regions like London and Hong Kong , ACs are used for investment banking , sales & trading , and other areas at banks and consulting firms. The questions resemble the ones you might find on the GMAT or the “mental math” questions common in sales & trading interviews. How much would it be worth?

At the time of the deal, it was expected to grow sales at 3-5%: Remember that PE deals do not require “growth.” These roles are for bankers and people with deal experience, such as corporate development professionals; firms care much more about your investment, financialmodeling , and due diligence skills than your scientific knowledge.

Here it is in the investor presentation: We don’t know the planned valuation for CMS in this spin-off, but let’s assume that Jacobs plans to spin it off at an IPO offering price that implies an 11.5x If you want more, there are several Sum of the Parts lessons in the valuation sections of our FinancialModeling Mastery course.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content