This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

E248: Setting Yourself Up for Success: Essential Steps, Tips, and Strategies for a Profitable Exit - Watch Here About the Guest(s): Kip Wallen is a seasoned M&A attorney with over a decade of experience in live mergers and acquisitions deals, primarily within the lower middle market, involving transactions up to $50 million.

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. We’ll also detail some of the factors affecting these calculations.

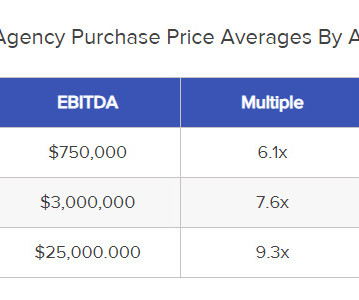

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

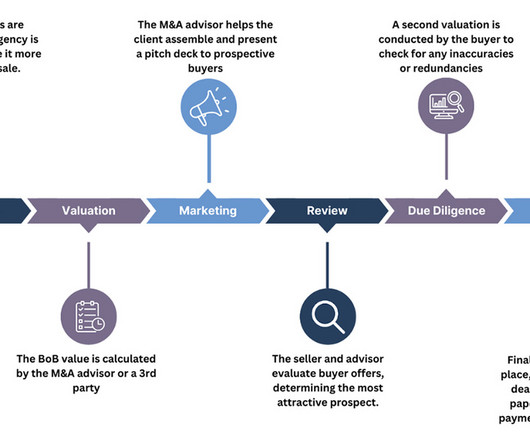

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. Selling an insurance agency book of business has a few advantages over selling the agency in total. Why Sell Just the Book?

For agency owners looking to sell their business in 2024, it’s helpful to know something about the insurance M&A buyer landscape before going in. The following section details the insurance M&A buyer landscape as of Q3 2024. To provide a sense of context for buyers’ current standing, we also include information from 2023.

Although insurance agencies are not always family affairs, the 2024 insurance landscape reveals that between 50% and 70% of agencies are family-owned. The valuation process has a few additional considerations when selling a family insurance agency. In particular, sellers should be aware of: Family Reputation as an Asset.

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Agency vs. Company: Which Is The Better Insurance M&A Deal?

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. for insurance agencies.

This article outlines how to sell an insurance agency by chronological steps, with a quick overview of the process in the table immediately following. We also include some key insights we’ve gathered over several decades of selling insurance agencies. and EBITDA gives buyers a better sense of the agency's future profitability.

-Ron Concept 1: Explore Business Acquisitions and Mergers Business acquisitions and mergers are an increasingly popular way for entrepreneurs to grow their businesses and increase their profits. Once the evaluation is complete, the buyer and seller must then negotiate the terms of the transaction.

To do this, he obtained his insurance and securities licenses and started helping developers raise money. He realized that if he could buy enough companies, he could exit several of them a year and receive a large amount of profit in one go. He wanted to be able to invest in larger projects and help developers raise money.

Analyze the company’s income, balance sheets, and cash flow statements to get an overview of its performance, profitability, and financial stability over time. Review insurance coverage. The report will keep your key stakeholders informed and guide negotiations. Negotiate the terms and conditions.

Shifting focus to profitable, reliable customers strengthens cash flowwhat buyers ultimately value. This target is negotiated and agreed upon, and the investment banking advisor will play a large role here. Clearly break out expenses (insurance broken out by auto, health; salaries broken out by owner, employee; and so on.)

They are set for a specific span of time and might impact profitability if not managed well. Some of the common fixed costs are employee salaries, interest, rent, insurance, lease, insurance, utility payments, phone service, advertising costs, amortization, and more. The other side of fixed costs is variable costs.

Enterprise Insurance Policies. Internal Profit & Loss Statements (dating back two to three years). They are verifying the claims made in the initial negotiation stages. Business’ Professional Certificates. Existing Vendor/Client Contracts. Employment Agreements. Letter of Intent. Post-Closing Agreement.

Buyers will look for consistent revenue growth, healthy profit margins, and a solid balance sheet. Buyers who see a well-documented financial history are more likely to feel confident in your business’s stability and profitability. This trust is crucial in negotiations and can lead to a smoother and more prosperous sale process.

Ad backs refer to expenses that are added back to the business's profits to make it appear more profitable than it actually is. While some ad backs are straightforward, such as personal health insurance costs, others can be more difficult to navigate.

During negotiations and discussions with advisors or potential buyers, an understanding of key financial and operational metrics is crucial. GPM: Gross Profit Margin or Gross Margin Gross profit margin looks at gross profit as a percentage of total revenue and is the amount available to pay operating expenses and reinvest into the business.

It also opens the door for savvy buyers to talk them out of millions of dollars when it comes time for negotiations. How much higher, however, depends on the marketing process, due diligence, and negotiations as handled by your M&A advisor. Determine Valuation Methodology There are three traditional valuation methods for RIAs.

Whatever your motivation for selling, we’re sure you want a seamless transition in which you walk away with a decent profit from the sale. Future profit margins. This way, you’ll be able to fully justify your asking price and walk away knowing that you negotiated from an informed point of view. Client base.

Healthcare costs are generally high, and even those with insurance can face unexpected bills or gaps in coverage, leading to debt. It is important to note that all kinds of medical costs are not covered by health insurance. Also, insurance premiums for patients with debt problems are usually high. What Happens If Left Unpaid?

In other words, Adjusted EBITDA is used to illustrate the true underlying profitability of the business. The company made a provision for this amount, which was later added back to EBITDA during negotiations with potential buyers of BP assets. BP: In 2010, BP had to pay $20 billion for the 2010 Deepwater Horizon oil spill.

The emphasis here is on profit “add-backs” – i.e., discretionary or peculiar expenditures that can be added back to the profits of the business. The emphasis here is on profit “add-backs” – i.e., discretionary or peculiar expenditures that can be added back to the profits of the business.

Negotiate favorable terms that align with your business’s cash flow and profitability. A well-thought-out growth strategy can enhance the business’s profitability and, consequently, your ability to meet the financing terms. This could involve risk insurance, contingency plans, or renegotiating the financing terms.

Economies of scale help businesses with competitive strategy, enabling them to lower prices, improve profitability, and dominate markets. However, as production scales up, these fixed costs are spread over more vehicles, and the manufacturer can invest in robotic assembly lines and negotiate better deals for materials.

This insures that you will not need to start the process over again should negotiations terminate for any reason with a lead acquirer. Should sellers negotiate with more than one buyer simultaneously? Working with an investment banker better enables a seller to actively negotiate with numerous buyers independently.

That’s a situation ideal for private equity, which thrives on opportunities for consolidating far- flung businesses in order to create economies of scale to increase efficiencies, reduce costs, boost profitability and enhance the value of the enterprise.

As a seller, brokers have the expertise and experience to help you find potential buyers, negotiate terms of the sale, and handle all the various paperwork that’s involved. A shrewd business broker will be able to facilitate negotiations if a strategic buyer is identified. 3. Sell to a Financial Buyer. 4. Sell to your Employees.

PE refers to a form of investment where institutional investors—such as pension funds, mutual funds, and insurance companies—as well as wealthy individuals, provide capital to PE firms. These firms then acquire, grow, and eventually sell companies at a profit to generate returns. are all on the table to be negotiated.

This in turn allows you to price correctly, negotiate confidently, and settle on a just amount. Knowing the current fair market value of the business also gives you leverage to improve its profitability before listing. Check out these links: Mitigating Post-Closing Risks Through The Rep and Warranty Insurance.

By following these guidelines, businesses can make informed decisions, negotiate favorable terms, and mitigate risks to maximize the value of their M&A transactions. It helps the acquiring company to make informed decisions and negotiate the deal’s terms and conditions. Don’t have time to read it now?

Call it a compromise, call it delayed gratification, but do not call it simple: earn-out payments often give rise to disputes because the interpretation of what qualifies as the achievement of previously negotiated milestones can differ wildly once viewed through the muddied lens of time. In Windy City Investments Holdings, LLC v.

It is obvious that a very high cost of labor will affect the profitability of the business. The company has to bear the cost of insurance policy related expenses, and they are often given various healthcare benefits and short-term disability benefits as direct cost of labor. Therefore, it is necessary that it should be under control.

And it typically boils down to a few common elements that successful SaaS companies do particularly well: High-quality SaaS companies feature predictable, recurring revenues, solid unit economics , and high gross margin and gross profit rates.

With larger physician networks and access to specialist’s hospitals also gain negotiating leverage with insurers and can participate in alternative payment models, such as capitated and bundled payments, through vertical integration. Christopher Majdi, Director of Valuation & FMV Services at Premier, Inc.

It is very common for problems and issues to pop up during due diligence, so it’s important to stay proactive and be open to negotiation until the deal is finalized.” It shows a buyer the business’s true profitability by adjusting EBITDA to reflect any non-recurring revenues and expenses.

Market Trends: What You Need to Know “Sandbagging” concepts are often the subject of intense negotiation in M&A transactions. does a passing comment by the company's president about an employment issue as the buyer's team is rushing to grab a taxi after a full day's negotiation impart knowledge of that issue?

And I’ve been over 20 years already with BSF in the automotive industry in different segments of the automotive industry from different perspectives, different businesses in different countries as well in Mexico, US, Germany, back in the US on the sales part, marketing also on the other side of the negotiation table in procurement as well.

Financial Synergy : Financial synergy involves leveraging combined financial resources, such as capital, cash flow, or risk management capabilities, to achieve cost savings, maximize profitability, and enhance investment opportunities. Sharing risks across entities can lead to reduced insurance premiums and improved financial resilience.

They may exclude some assets and/or liabilities based on mutual negotiations. Remember, everything is negotiable up to the point of accepting or rejecting the deal. However, there are many times where we have been successful in negotiating a non-exclusive LOI with a buyer. You will be entitled to interest.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content