Insurance Broker Valuation Multiples: Q3 2024 Projections

Sica Fletcher

JUNE 11, 2024

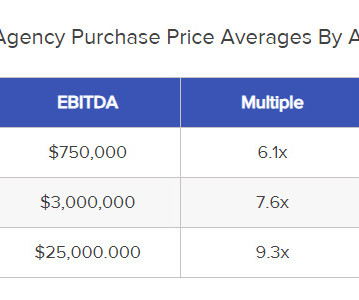

The following report contains our projections for Q3 2024 insurance broker valuation multiples. In addition, we categorize this data according to insurance industry specialization and by brokerage size, as measured by their annual revenue. Since H1 2023, the average insurance brokerage valuation multiple has hovered around 11.6x

Let's personalize your content