This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

E248: Setting Yourself Up for Success: Essential Steps, Tips, and Strategies for a Profitable Exit - Watch Here About the Guest(s): Kip Wallen is a seasoned M&A attorney with over a decade of experience in live mergers and acquisitions deals, primarily within the lower middle market, involving transactions up to $50 million.

Disclaimer: The article below contains a quick and easy method for calculating the ballpark value of an insurance agency using standardized market information. Readers should note that the actual value of your insurance agency may vary considerably from what this estimate might provide.

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. We’ll also detail some of the factors affecting these calculations.

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. Selling an insurance agency book of business has a few advantages over selling the agency in total. Policy Assignment.

Although insurance agencies are not always family affairs, the 2024 insurance landscape reveals that between 50% and 70% of agencies are family-owned. The valuation process has a few additional considerations when selling a family insurance agency. Family-specific financial arrangements.

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

At the core of the debate of business appraisal vs business valuation, both approaches aim to determine a company’s worth. So, what’s the difference between a business appraisal and a business valuation? They indicate a company’s past performance and potential future profitability.

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

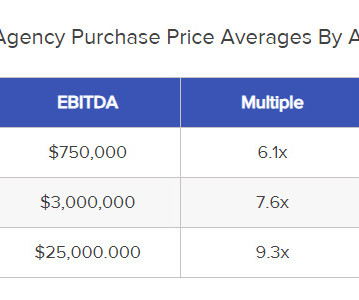

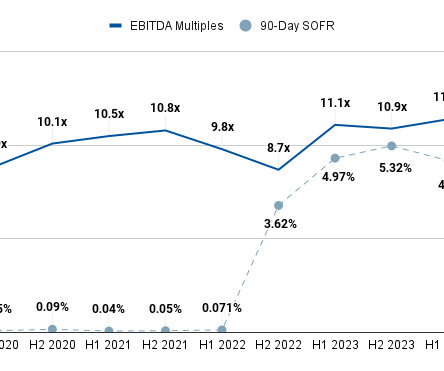

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

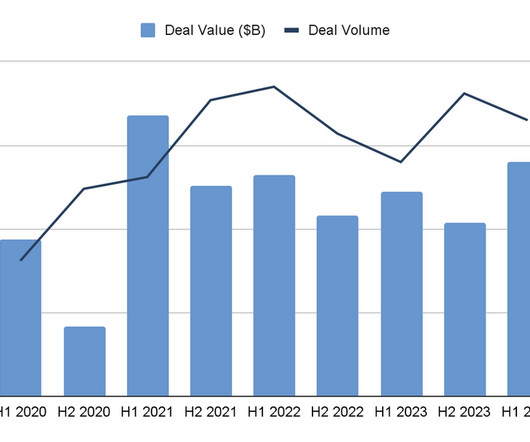

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Agency vs. Company: Which Is The Better Insurance M&A Deal?

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

Selling an insurance brokerage is not altogether that much different than selling an insurance agency or even an insurance company. specialized regulatory and licensing requirements that are different from those of insurance agencies. That being said, brokerage owners need to consider a.)

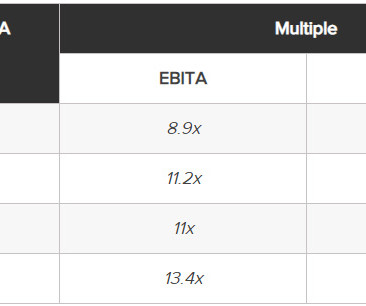

The following report details insurance brokerage M&A multiple averages for H1 2024. Our research team averaged the information using data from our Sica | Fletcher index, which monitors approximately 70% of insurance sector transactions. Because several kinds of insurance are legally required (e.g.,

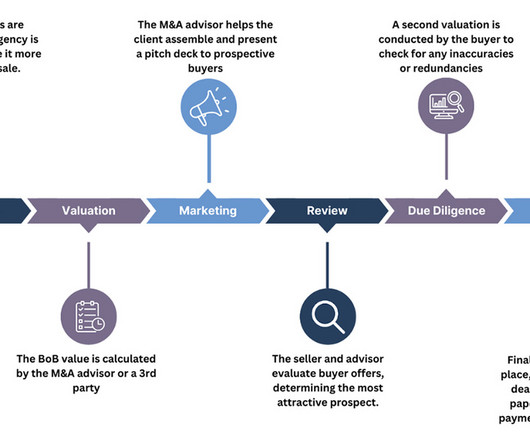

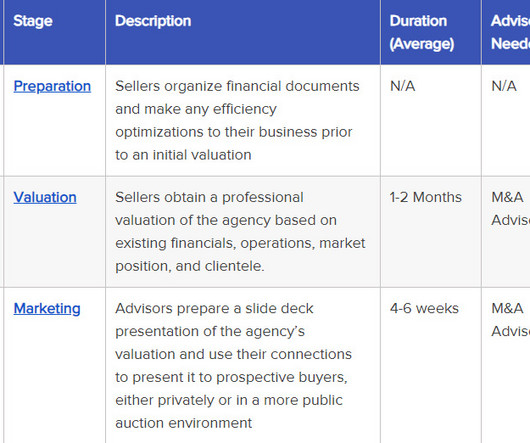

This article outlines how to sell an insurance agency by chronological steps, with a quick overview of the process in the table immediately following. We also include some key insights we’ve gathered over several decades of selling insurance agencies. Valuation is a process in and of itself.

Such expenses are often associated with medical insurance, which does not come under reimbursable once. Table of contents Out Of Pocket Expense Meaning Out Of Pocket Expense Explained What Are Health Insurance Out-Of-Pocket Expenses? What Are Health Insurance Out-Of-Pocket Expenses?

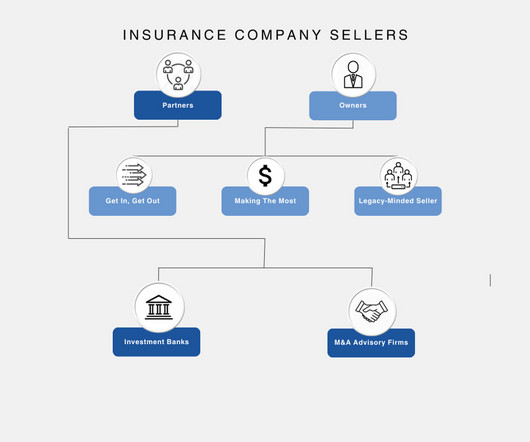

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome.

Many of our clients have asked us about the impact on insurance brokerage M&A of the pandemic and the resultant containment efforts. The Largest Strategic Players Tell Us Full Steam Ahead – The major strategic acquirors have informed us that they plan to continue to aggressively pursue acquisitions of insurance brokers.

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. In other words, you profit based on the company’s dividend s and the potential increases in its stock price over time. The post The Dividend Discount Model (DDM): The Black Sheep of Valuation?

Shifting focus to profitable, reliable customers strengthens cash flowwhat buyers ultimately value. Clearly break out expenses (insurance broken out by auto, health; salaries broken out by owner, employee; and so on.) These are called addbacks, and are extremely important to valuation. product, service and sales channel).

Tax Benefit Explained Forms Examples Eligibility For Family Tax Benefit Health Insurance Tax Benefit Married Vs Single Recommended Articles Tax Benefit Explained A tax benefit refers to the advantages or savings a company gains from utilizing various tax provisions and deductions provided by tax regulations.

Who Performs A Valuation? RIA valuations are typically performed by one of three parties: The M&A Advisor A Third-Party Specialist The Seller Themselves Although many sellers attempt to perform their own valuations, we strongly recommend against this.

Often discussed in the context of bridging a valuation gap, an “earn-out” can be a (seemingly) attractive solution for parties who have reached agreement on everything but the purchase price. Teachers Insurance and Annuity Association of America (TIIA ) , TIAA acquired Nuveen, a mutual fund and advisory firm, from Windy City for $6.25

This differentiation helps identify a company’s profitabilityProfitabilityProfitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs. It is measured using specific ratios such as gross profit margin, EBITDA, and net profit margin.

Business valuation, according to the Corporate Finance Institute , is the “process of determining the present value of a company or an asset.”. In this post, we’re going to answer why you need to conduct a business valuation, how you can determine your business value, and how to find the best business valuation specialists.

Whatever your motivation for selling, we’re sure you want a seamless transition in which you walk away with a decent profit from the sale. billion valuation by 2030. The first step in positioning your HVAC business for a favorable acquisition is increasing its current valuation. Future profit margins. Client base.

And in a lot of cases, these are very profitable services, but that specialization is going to lead to massive efficiencies throughout your organization. There’s also continued insurance challenges and a whole lot more. On average, I’m seeing these shops are 50 to 100% more profitable than their generalist counterparts.

To do this, he obtained his insurance and securities licenses and started helping developers raise money. He realized that if he could buy enough companies, he could exit several of them a year and receive a large amount of profit in one go. He wanted to be able to invest in larger projects and help developers raise money.

Concept 4: Financials Can Be Deceiving The podcast discusses the challenges that arise when buying small businesses, particularly those with sub-$5 million valuations. Despite these challenges, the podcast suggests that it is still possible to invest in small businesses with sub-$5 million valuations.

It’s also the second Black-founded unicorn in the UK, and co-founders and brothers Oliver and Alexander Kent-Braham, along with CTO David Goaté have set their sights on disrupting the insurance industry. And it’s fair to say that for a while some private market valuations became inflated, with predictable consequences for some.

Risk Management Asset Valuation: Proper estimation of salvage value is crucial in ensuring accurate asset valuation, which is fundamental in risk assessment and management. Insurance Purposes: For insurance coverage, the salvage value of assets is often considered to determine the appropriate level of insurance needed.

The lender, in this case, who buys the instrument has to pay the premium like that of an insurance policy, in exchange of which the seller of the instrument will compensate for the loss in case of default faced by the buyer of the instrument from their borrower. Speculators use the difference in prices to trade and make profits.

And it typically boils down to a few common elements that successful SaaS companies do particularly well: High-quality SaaS companies feature predictable, recurring revenues, solid unit economics , and high gross margin and gross profit rates. The firm currently employs 31 professionals. The firm employs 93 professionals.

Preparing Your Manufacturing Business for Sale Conducting a comprehensive business valuation is essential in preparing your business for sale. Conducting a Comprehensive Business Valuation A comprehensive business valuation is crucial when preparing your manufacturing business for sale.

Negotiate favorable terms that align with your business’s cash flow and profitability. Conduct a Thorough Business Valuation: Before moving forward with an M&A deal, conducting a comprehensive business valuation is essential. This could involve risk insurance, contingency plans, or renegotiating the financing terms.

There are several reasons Strandberg thinks single store collision repair shops that fix all vehicles are going by the wayside — insurance challenges, increasing vehicle complexity and OEM certification training requirements chief among them. You are not limiting yourself by specializing by increasing profitability.

In the commercial tire business, the quest for profitability can sometimes feel like a struggle. Consider this scenario: after years of hard work and dedication, your tire business has grown, but its profit margins remain in the 3% to 4% range. Additionally, you generate personal income by leasing the property to the business.

PE refers to a form of investment where institutional investors—such as pension funds, mutual funds, and insurance companies—as well as wealthy individuals, provide capital to PE firms. These firms then acquire, grow, and eventually sell companies at a profit to generate returns. to 6x EBITDA on average.

Insure the Deposits – But this is expensive and is available only up to a certain per-account limit in most countries, such as CHF 100,000 in Switzerland and $250,000 in the U.S. Insuring all deposits or deposits up to $10 million is a bad idea because it will encourage bank executives to be even more reckless.

In the financial services industry, insurance companies use these portfolios to manage their assets and liabilities positions. Replicating portfolios for insurance liabilities is useful to measure the risks associated with the liabilities under consideration. Insurance companies use this tool for risk management and planning.

Despite investment in the first half of 2023 dropping to £4.6bn from 2022’s £10.8bn as a result of rising interest rates, high inflation, a decrease in valuations and geopolitical tensions globally, UK fintechs are still attracting more VC investment than all other EMEA fintechs combined, with a significant percentage coming from US investors.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content