This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

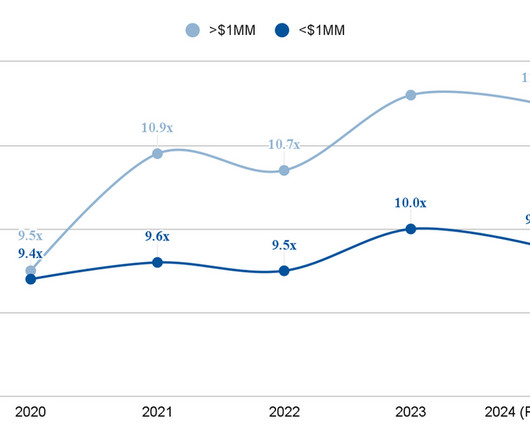

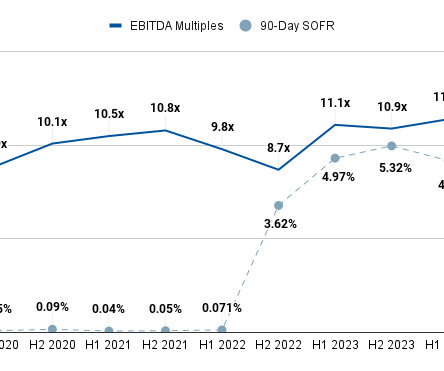

The following report contains our projections for Q3 2024 insurance broker valuation multiples. In addition, we categorize this data according to insurance industry specialization and by brokerage size, as measured by their annual revenue. Since H1 2023, the average insurance brokerage valuation multiple has hovered around 11.6x

As one of the most active M&A firms in the insurance sector, we are frequently asked how insurance agency valuations work. This article discusses the fundamentals of insurance agency valuations, plus a few lesser-known factors that play into these processes before we give an overview of the insurance M&A market in 2024.

Disclaimer: The article below contains a quick and easy method for calculating the ballpark value of an insurance agency using standardized market information. Readers should note that the actual value of your insurance agency may vary considerably from what this estimate might provide.

Insurance agency owners who are considering the prospect of running an M&A deal process often have many concerns about the fate of their agencies, but the most common by far are those surrounding the agency’s purchase price at closing. We’ll also detail some of the factors affecting these calculations.

When insurance agency sellers have already met with prospective buyers, they may have been offered a valuation based on their “adjusted EBITDA.” The following article provides a brief overview of EBITDA and adjusted EBITDA valuations for insurance agencies. What Is EBITDA? What Is Adjusted EBITDA?

This article presents a step-by-step guide on how to value an insurance agency - both in the sense of how a valuation agency/M&A advisor goes about valuation, and also in terms of what insurance agency owners can do to maximize their valuation prior to running an M&A deal.

Although insurance agencies are not always family affairs, the 2024 insurance landscape reveals that between 50% and 70% of agencies are family-owned. The valuation process has a few additional considerations when selling a family insurance agency. Family-specific financial arrangements.

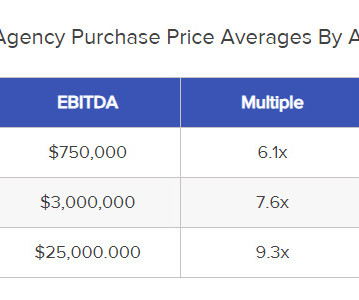

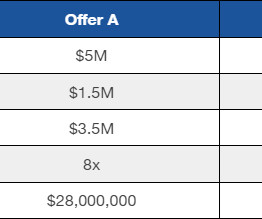

This article breaks down the question, “how much is my insurance agency worth” in further detail, but the table below provides a surface-level overview based on varying degrees of revenue and operating expense: How Much Is My Insurance Agency Worth: A Breakdown Answering the question, “how much is my insurance agency worth?”

The following report examines the health and outlook for insurance M&A deals in 2024. We base this research on several key findings in our proprietary SF database, which observes and records data from the top ~400 insurance M&A buyers. Agency vs. Company: Which Is The Better Insurance M&A Deal?

Quite a few articles already detail the process of “how” to sell an insurance agency (you can read our article on that subject here ), but very few get to the bare bones of “why.” If you’re asking, “ should I sell my insurance agency,” the three big questions you must answer first are: Why Do I Want To Sell?

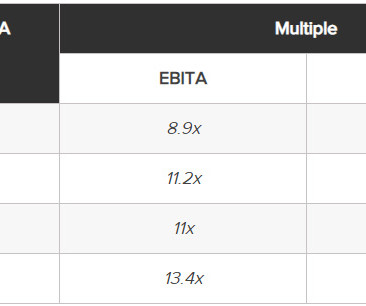

Having advised on a record number of insurance agency M&A transactions, we have used our unusually large dataset in tandem with access to third-party M&A databases to provide up-to-date averages of EBITDA multiples for insurance brokerages in 2024. What Is Affecting Insurance Agency EBITDA Multiples?

The following article details the process of selling an insurance agency book of business in 2024, including deviations from the process of selling an agency, the valuation process, and common payout structures. Selling an insurance agency book of business has a few advantages over selling the agency in total. Policy Assignment.

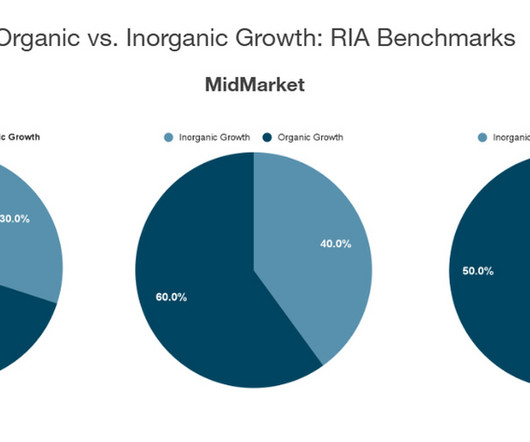

The following article examines valuation multiples for registered investment advisor (RIA) firms as of 2024, based on data gathered from our SF Index and available third-party sources. How these client demographics affect RIA valuations really depends on what the buyer is looking for, as indicated by the table below.

Our research team’s latest report compares the top insurance agency investment banks of 2024. Insurance Agency Investment Banks: Investment banks that specialize in the insurance industry. Insurance Agency Investment Banks: Investment banks that specialize in the insurance industry.

In it, we provide readers with a quick and simple overview of the current insurance brokerage M&A market , after which we discuss several macroeconomic and industry-specific factors that could drastically affect transactions in the next six months. The market is already highly competitive, but it’s also limited to what buyers can afford.

The 2024 insurance M&A market has changed substantially from just a few years ago, with potentially staggering implications for the future of insurance M&A transactions. Insurance M&A Transactions in 2024 The insurance M&A transactions we have observed thus far in 2024 indicate larger trends in the sector.

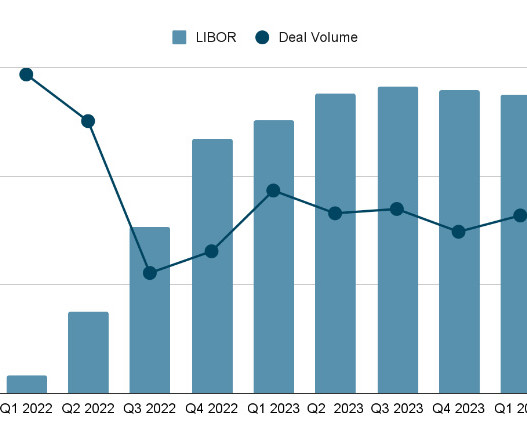

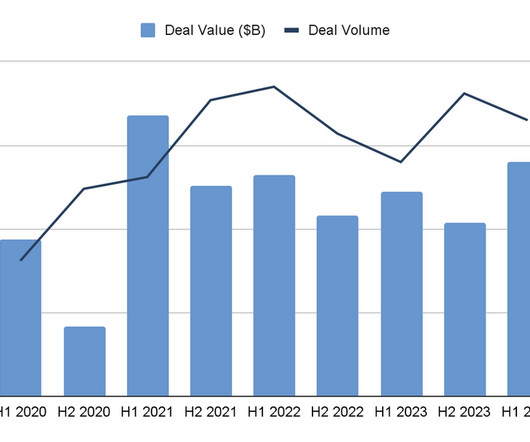

M&A transactions for insurance companies are part of a robust but complicated market that requires ingesting a great deal of data in order to fully understand. While insurance M&A did see slight dips in deal volume and average value (Fig.2) While insurance M&A did see slight dips in deal volume and average value (Fig.2)

The insurance M&A market in 2024 is significantly more complex now than it was 20 years ago. However, this report seeks to make sense of these qualities as a whole to provide an overview of the 2024 insurance M&A market. The table of contents below offers quick links for readers seeking specific information in later sections.

The following report details insurance brokerage M&A multiple averages for H1 2024. Our research team averaged the information using data from our Sica | Fletcher index, which monitors approximately 70% of insurance sector transactions. Because several kinds of insurance are legally required (e.g., Streamlined Operations.

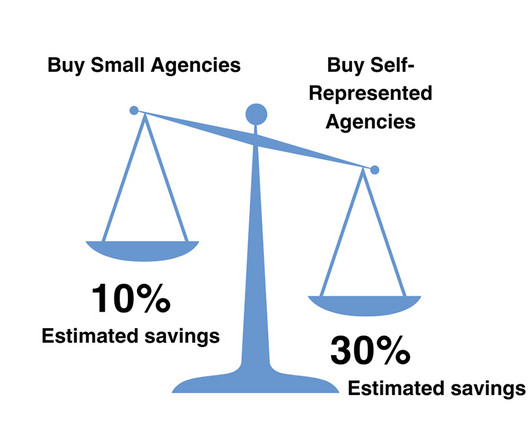

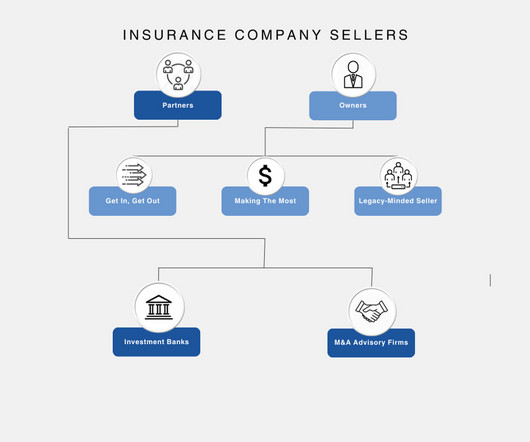

This article examines the most common types of insurance agency sellers, which we break down into two distinct categories: the owners - agency CEOs and founders - and the partners - professionals in charge of overseeing a sale to ensure the best outcome.

Selling an insurance brokerage is not altogether that much different than selling an insurance agency or even an insurance company. specialized regulatory and licensing requirements that are different from those of insurance agencies. That being said, brokerage owners need to consider a.)

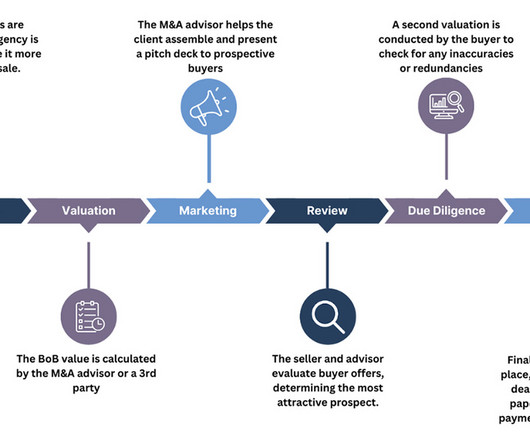

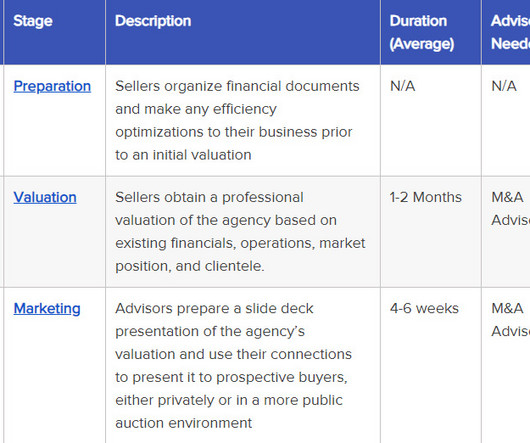

This article outlines how to sell an insurance agency by chronological steps, with a quick overview of the process in the table immediately following. We also include some key insights we’ve gathered over several decades of selling insurance agencies. Valuation is a process in and of itself.

To be fair, in some industries – like commercial banks and insurance within FIG – the DDM is a core valuation methodology. In other words, you profit based on the company’s dividend s and the potential increases in its stock price over time. But outside of those, its status is murkier.

Corporate structure Whether youre a C-Corp or S-Corp can affect taxes at sale. Optimize Working Capital (One Year Ahead) What It Is: Net Working Capital (NWC) is Current assets minus current liabilities (A/R + Inventory A/P + Accrued Expenses), excluding cash, which you keep (in a typical cash-free, debt-free transaction).

S&P Global’s 2023 Market Intelligence League Table Released NEW YORK, NY - February 8, 2024 - Sica | Fletcher, a premier financial advisory firm, retains its commanding presence in the #1 spot on S&P Global’s Market Intelligence League Table, a position the firm has held quarter-over-quarter since 2017.

Who Performs A Valuation? RIA valuations are typically performed by one of three parties: The M&A Advisor A Third-Party Specialist The Seller Themselves Although many sellers attempt to perform their own valuations, we strongly recommend against this.

Peaked market valuations: When market cycle peaks or an industry fully matures, it may be advantageous for shareholders to cash out. Regardless of the base reason(s), the current owners and management of a company looking for a new owner should seek to: Maximize return on investment for current owners.

We know that the formula for valuing high cash-flowing businesses is a multiple applied to profitability, but with lower-margin businesses, it’s likely to be an asset-based valuation comprised of the A/R, inventory and equipment — hopefully with a bump for goodwill. This approach has several advantages: Diversification. Lower costs.

Technical Questions – You could get standard questions about accounting and valuation or VC-specific questions about cap tables, key metrics in your industry, or how to value startups. If you worked at a startup, how did you win more customers or partners in a sales or business development role? Q: Which current startup would you invest in?

With larger physician networks and access to specialist’s hospitals also gain negotiating leverage with insurers and can participate in alternative payment models, such as capitated and bundled payments, through vertical integration. Christopher Majdi, Director of Valuation & FMV Services at Premier, Inc. 2019, May 2).

This includes examining the company’s financials, contracts, and other documents that will help them to determine the value of the business. Having the right documents in place, such as an operating agreement, P&Ls, meeting minutes, and resolutions, can make the process of selling the business much smoother and easier.

Government funded programs include Medicare, Medicaid, Children’s Health Insurance Program, and the Veterans Health Administration. Physicians for National Health Program note that 64% of health spending is paid by the government and most public sector employees are able to get health insurance from the government.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content