This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Will Cava Going Public Set the Table for Other IPOs? By David Braun, Founder and CEO, Capstone Strategic When Washington DC based restaurant chain Cava became a publicly traded company recently, it bucked a trend that has lasted nearly two years, a notable absence of American IPOs.

rn As the discussion progresses, Wells shares his reflections on being the CEO of a public company post-IPO, the unexpected realities, and the learning curve that has come with the territory. rn rn rn Going public as a company involves facing market dynamics and investor behaviors that may not align with pre-IPO expectations.

The fundraising process typically involves multiple stages, starting with initial discussions and due diligence, followed by formal presentations, negotiation of terms, and ultimately securing commitments from investors. The process can be time-consuming, often taking several months or even years to reach the target fund size.

is the increased frequency at which SPAC IPOs are occurring. As reflected in Chart 1 , 102 SPAC IPOs have been announced this year as of September 18, 2020—almost double the number of SPAC IPOs in all of last year (and more than double the number of SPAC IPOs in 2018). A distinct feature of SPAC 3.0 Fewer Redemptions.

Whether there’s a looming threat of a government shutdown or a sudden stock market sell-off, or the auction bids come in below expectations, the alternative track may present a superior exit option. Is the IPO track suitable for (and available to) the business? Is the objective to achieve a partial or complete exit?

For growth-stage companies, you will see plenty of equity offerings: IPOs , SPACs , PIPEs, and follow-on issuances. For a good example, look at this BofA presentation to Green Plains , which was structured as an MLP at the time and treated like a pipeline company in oil & gas.

With M&A deals and IPO activity at their lowest levels since the peak in 2021, the old adage is proving true: “in bull markets, banks tend to over hire, and in bear markets, they over fire.” M&A Deal Volume Fell in Q1 2023 Do not take being laid off as a personal reflection of your ability or worth.

This entails meticulously reviewing a multitude of deals presented by investment bankers. This phase involves seamless collaboration with legal experts, accountants, and other professionals to execute exit strategies, which may involve divestiture or taking the company public through an IPO.

Dig deeper into articles related to Equity markets, IPOs, M&As, Private Equity Fundings, and Startups. This is the perfect time to learn Excel formulas and create visually appealing presentations as they are fundamental to an investment banker's work. News is a gateway to the outside world.

Investment Banking: Deals The basic difference is that in “investment banking” groups, such as technology , TMT , healthcare , or consumer retail , you work on various deal types: sell-side and buy-side M&A, leveraged buyouts, IPOs, follow-on offerings, and bond issuances. or debt offerings (investment-grade or high-yield bonds).

There are compelling rationales for adopting a dual-class structure, but even proponents of the structure generally acknowledge that these benefits are significantly mitigated once the dual-class shares are out of the hands of the founders and/or pre-IPO stockholders. Potential carve outs for M&A voting agreements. Stockholder litigation.

You’re better off developing a broader set of skills , such as how to work in a group, prioritize emails, and give a simple presentation, rather than memorizing technical details. In the scenario above, for example, you wouldn’t want to schedule a VP’s potential client meeting on any of the same days as the IPO roadshow.

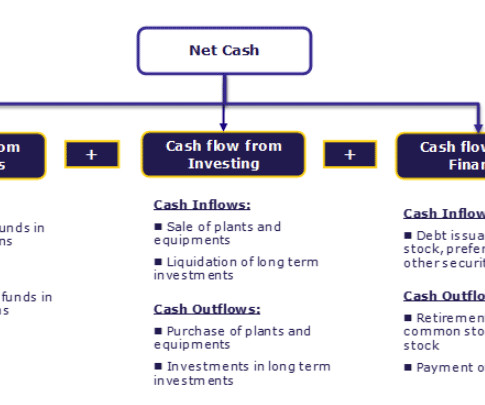

read more and balance sheet Balance Sheet A balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the company at a specific point in time. Thus, a cash statement presents the cash generated and spent on all these activities individually and collectively.

Cava opened the IPO window and showed that a good company can go public in any market. A common theme was present throughout 2023’s dealmaking: strategic buyers were keen on concepts that show strong performance in recent years, especially traffic. Subway sold to Roark Capital for $9.6

Public companies and companies contemplating an IPO are in a trickier situation. It has been common market practice for founders, private equity sponsors and other controlling stockholders to retain governance rights over a controlled company after an IPO, often through a stockholder agreement with the IPO issuer.

For VC, your strengths should include points like “communication/presentation skills,” “networking ability,” and “being able to update your views quickly” (i.e., Q: Tell me about the current IPO, M&A, and VC funding markets. Q: What are your strengths and weaknesses? A: See our walk-through, guide, and examples.

As SPAC IPOs broke records – in both value and volume – in 2020 (and again in 2021), it was inevitable that stockholder litigation would follow. billion IPO in February 2020. In the context of a deSPAC, the court found that a value-decreasing merger would present a unique benefit to the Sponsor given the Sponsor’s promote.

Although there were 104 initial public offerings of biotechnology companies in 2021 that raised nearly $15 billion in funds, 2022 saw only 22 such IPOs collectively raising less than $2 billion. Let’s dig in. Not to be outdone by their US counterparts, regulators outside the US also are taking more interventionist roles in merger review.

Risks and Challenges in the Development and Startup Stage Despite the excitement and potential rewards, the startup stage presents numerous risks and challenges. Choosing the right exit strategy—be it acquisition, Initial Public Offering (IPO), or management buyout—is critical.

It won’t replace Analysts or Associates because it can’t create entire presentations with all the correct details. But it speeds up the process by generating slide templates based on your queries, presentation data, and free examples on the sec.gov site.

For public companies with well-performing stocks (or at least for those doing better than their peers) looking for strategic acquisitions, using stock as acquisition consideration will present a viable alternative to cash.

However, one common point across all the verticals is that IPOs are not common because there aren’t that many publicly traded sports teams, stadiums, or arenas. SPAC IPOs for esports companies were “hot” for a short period in 2021, but they seem to have died off by now.

Strained access to public markets and funding The IPO market remained relatively inactive in 2023, leading many life sciences companies looking to raise funds to turn to other exit strategies. Additional major acquisitions of 2023 included Pfizer’s acquisition of Seagen for $43 billion and Merck’s acquisition of Prometheus for $10.8

Venture capitalists typically have shorter investment horizons and seek quick exits, either through an IPO or an acquisition. Nevertheless, collaborating with venture capitalists in M&A presents its own set of disadvantages. Yet, collaborating with private equity firms in M&A also presents certain disadvantages.

Or perhaps simply, it presents an opportunity where you have a first-mover advantage and it’s a race to success where you are first out of the blocks. When I left parliament, I decided to focus on investing in and mentoring pre-revenue businesses primarily run by young entrepreneurs.

Each method offers different benefits; finding the best option for your software company’s goals is essential to ensure that you clearly understand the landscape and how best to present your business when the time comes to pursue seeking external capital.

At Goldman Sachs, she led the firm’s technology IPO business and became the first female partner of Goldman Sachs’ equity division. She commented that it was probably five years before she was ever in a meeting with another woman present, and there were certainly no women in leadership roles she could look up to.

When a deal becomes “active” in IB, you dive into it and go in-depth into all aspects, from the financials to the buyer/seller outreach to the presentations and more. You can think of it like this: Wealth Management: Broad and long-term/continuous client coverage.

Here it is in the investor presentation: We don’t know the planned valuation for CMS in this spin-off, but let’s assume that Jacobs plans to spin it off at an IPO offering price that implies an 11.5x EBITDA multiple , matching its own. EBITDA since it’s only growing at 2-3% per year vs. 5-10% per year for Jacobs.

Throughout his career, he has been instrumental in underwriting IPOs for family-held businesses and tracking the evolution of private equity. For instance, inflated executive salaries should be recalibrated to match industry norms, thereby presenting a realistic profitability picture.

2020 was also a blockbuster year for special purpose acquisition company (SPAC) activity, as 247 SPAC IPOs raised more than $75 billion (a 525% increase compared to the amount raised by SPAC IPOs in 2019) [3]. Creative deal terms and financing arrangements were also attractive aspects of SPAC deals as compared to their IPO cousin.

We had a chance to discuss cybersecurity and IT due diligence with M&A Leadership Council’s presenters at our various events, and we are pleased to share portions of this discussion with you below. It goes beyond the current state findings though, and goes straight to important strategic implications for the deal.

We recently had a chance to discuss cybersecurity and IT due diligence with M&A Leadership Council’s presenters at our various events, and we are pleased to share portions of this discussion with you below. It goes beyond the current state findings though, and goes straight to important strategic implications for the deal.

As we have previously observed , the use of milestone-based earnouts to bridge a valuation gap is often a short-term solution that presents many long-term complications. 2020 was also the year of the SPACraze , with SPAC IPOs raising more than $75 billion in gross proceeds, a 525% increase compared to 2019.

As the public markets gained traction, IPO activity and venture investment saw a resurgence, signaling renewed investor confidence and reflecting sustained interest in biotech innovation. However, the M&A market presented a mixed picture, with overall deal values declining, but deal volumes remaining robust.

Some sponsors, while unable to present compelling take-private proposals to targets, have deployed capital in private investments in public equity (PIPEs) of public targets, marketing these investments as both a vote of confidence for the incumbent board and much-needed liquidity to help the target weather the downturn.

Communication/presentation skills and technical/modeling/deal skills are all quite important, but “sales skills” are also crucial if you’re interviewing at a firm with significant sourcing. Exits Up Slightly But Still Poor – M&A activity has ticked up modestly, but the IPO market is still mostly shut.

their Enterprise Values are not worth much for a long time): Hedge funds focusing on public biotech companies step into this process after the IPO part, which means they can bet on extreme value inflections based on binary outcomes. Beyond that, we recommend these sites: BioPharmCatalyst For quickly generating stock pitch ideas.

I believe there will be a significant pick up in capital market activity, provided deals are priced realistically, leading to an increase in companies coming to the public markets through IPOs. They need to differentiate themselves and adapt to modern trading conditions.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content