This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

E248: Setting Yourself Up for Success: Essential Steps, Tips, and Strategies for a Profitable Exit - Watch Here About the Guest(s): Kip Wallen is a seasoned M&A attorney with over a decade of experience in live mergers and acquisitions deals, primarily within the lower middlemarket, involving transactions up to $50 million.

Charlie, Tim, and the entire team’s ability to help us understand and navigate the transaction process and negotiate the best possible deal was critical in getting the right deal with the right partner,” Tim Miller, President & CEO of Freestate, stated. “The CCA team was instrumental in helping us achieve this milestone for Freestate.

The project is designed to assist budding entrepreneurs and corporate managers in acquiring and scaling lower middle-market companies. Roger discusses the importance of implementing professional infrastructure and operational systems to render these small businesses attractive to middle-market buyers.

He focuses on lower-middlemarket acquisitions, predominantly involving blue-collar, value-oriented, and baby boomer-owned businesses. rn rn rn Rapport building and active listening are critical skills in negotiation, often determining the success of an acquisition more than the financial offer. anything else in the deal.

After targets are identified and screened, Sun provides advisory services including valuation, drafting and negotiating offer letters, and due diligence support. We work with clients that are interested in the confidential sale, acquisition, or valuation of privately held middlemarket and main street companies.

Throughout his career, Ken has become proficient in contract negotiations of complex business environments, working in a variety of industries throughout the United States. We work with clients that are interested in the confidential sale, acquisition or valuation of privately held middlemarket and main street companies.

Selling your middle-market business is a significant endeavor, requiring meticulous planning, negotiation, and execution. Yet, amid all the intricacies, there's one crucial element that is often underestimated or overlooked: the shareholder agreement.

Execution Rigor: From pre-LOI diligence to managing legal negotiations, execution quality often determines whether a deal closes on favorable terms. For mid-market or lower-middle-market tech companies, they may not be the right fit. Mid-Market Tech Deals ($50M$500M) This is where sector-focused investment banks shine.

Execution Rigor: From pre-LOI diligence to managing legal negotiations, execution quality often determines whether a deal closes on favorable terms. For mid-market or lower-middle-market tech companies, they may not be the right fit. Mid-Market Tech Deals ($50M$500M) This is where sector-focused investment banks shine.

Periculum facilitated and led negotiations with Redwood to ensure the Hope team received both upfront value for its best-in-class operations and future upside to capitalize on the Companys significant growth opportunities. We absolutely could not have done this without them.

He has the unique perspective of being both the seller and the buyer, which provides valuable insight into the complexities and process of negotiations required to successfully complete business transactions. Mike will bring his real-life experiences to the firm and to his own future transactions.

Private Capital Markets is the first book to present a theory of how the private markets work at the lower end of the middlemarkets. Slee’s theory of middlemarket finance is based on empirical evidence, or real world observed activity. And that’s all it took to become an investment banker. Don’t wing it.

David wisely notes that these multiples are specific to the Main Street segment, and he distinguishes this from the lower MiddleMarket segment, where multiples can range from 3.2x Reconciled sets the standard for consistency and quality that you can count on. David does not discuss individual stocks or mutual funds.

Kevin Roberts Senior Advisor, M&A Partners Kevin Roberts has over 25 years of experience growing middle-market sized businesses both as a principal investor and as a strategic advisor.

After targets are identified and screened, Sun Acquisition provides advisory services including valuation, drafting and negotiating offer letters, and due diligence support. We work with clients that are interested in the confidential sale, acquisition, or valuation of privately held middlemarket and main street companies.

The family office especially appreciated CCA’s ability to assist in evaluating targets, construct cash flow models, and negotiate with lenders to successfully obtain debt financing. The CCA team made a huge difference in getting our deal over the finish line.” For more information, visit www.ccabalt.com or call 410.537.5988.

Periculum’s dedicated senior leaders that are involved in each step of a transaction— from buyer identification to final negotiations—culminated in the successful execution of the sale. The team at Periculum was very gratified to have been chosen by the estate’s personal representatives to run this process,” said Fritz Schutte.

Safeguarding Employee Interests after Selling When selling a business, it is crucial for the seller to prioritize the welfare of their employees during the negotiation process. During the negotiation phase, sellers should clearly communicate their expectations about employee welfare to potential buyers.

rn Visit [link] rn _ rn About The Guest(s): Bill Snow is an author and mid-market investment banker with over 20 years of experience in mergers and acquisitions. He is the author of "Mergers and Acquisitions for Dummies" and has worked on various transactions in the middlemarket space.

But navigating this middle-market M&A terrain is anything but simple. Understanding these dynamics is essential to tailoring your positioning and negotiating leverage. These can bridge valuation gaps but require careful negotiation. Earn-outs Contingent payments based on post-close performance.

Private equity firms will continue to be interested in this space, and many times try and approach tire dealers directly so they have the upper hand in negotiations. With a lifetime spent in is family’s automotive business, he now advises and assists privately held middlemarket auto aftermarket companies with mergers and acquisitions.

After successfully opening three new locations in 2020 and 2021, Pet Palace engaged Periculum in late 2022 to run a targeted sell-side process positioning the Company as a premium asset in a highly fragmented market. As one of the leading consolidators of pet resorts in the U.S.,

In addition to designing the customized debt placement solicitation process, Periculum assisted Morgan with information preparation, outreach to and ongoing communication with prospective lenders, negotiation of term sheets, documentation and the closing.

The family office especially appreciated CCA’s ability to assist in evaluating targets, construct cash flow models, and negotiate with lenders to successfully obtain debt financing. The CCA team made a huge difference in getting our deal over the finish line.” For more information, visit www.ccabalt.com or call 410.537.5988.

In M&A, working capital is often a significant area of negotiation between the buyer and the seller. During M&A negotiations, working capital refers to the additional funds required to finance the deal, including items such as cash reserves, inventory, accounts payable and receivable, debt payments, payroll expenses and related costs.

rn As the industry continues to evolve, Peterson Acquisitions aims to bring more sophistication to the lower middlemarket and empower entrepreneurs to make informed decisions about their business ventures. rn The future outlook for the industry is promising, with Peterson Acquisitions leading the way in innovation and expertise.

Maximize success with expert tips on promotion, salary negotiations, and more. That’s the minimum time we recommend allocating to PE prep to be competitive for a megafund or upper middlemarket placement during on-cycle. Our “On-Cycle Kicked” series brings a fresh perspective and innovative approach to professional development.

Their skillful negotiating, creativity, and unwavering commitment to me was so much more than I ever expected to receive from an M&A advisor.” About Periculum Capital Company, LLC Periculum is a leading investment and merchant banking firm serving the corporate finance needs of middlemarket companies.

The scope and detail of these representations and warranties are often heavily negotiated and tailored to reflect not only the nature of the target and its business, financial condition, and operations, but also the relative negotiating strength of the buyer and seller. Observations. ” Observations. ” Observations.

In Q3, the pattern we’ve continued to see is fairly typical of a market reset – bifurcation. The first area of bifurcation is between the large cap and middlemarket Tech M&A markets. This has led to a significant drop in software M&A, with each consecutive quarter showing a decline from the last.

Private Equity Remains a Dominant Buyer Class Private equity firms continue to be the most active acquirers in the software space, particularly in the lower middlemarket ($5M$50M ARR). Our guide on earn-outs in software M&A offers practical advice for navigating these negotiations.

The scope and detail of these representations and warranties are often heavily negotiated and tailored to reflect both the nature of the target and its business, financial condition and operations, but also the relative negotiating strength of the buyer and seller.

Speaking to an experienced M&A CPA ahead of time can save headaches during the negotiation process and potentially millions in taxes owed. With a lifetime spent in is family’s automotive business, he now advises and assists privately held middlemarket auto aftermarket companies with mergers and acquisitions.

“We focused on telling Mark’s story by using the rich data he and his team collected about their customers, projects, market opportunities and dynamic changes occurring in the industry,” said Sean Frazer, a partner at Periculum. The firm was founded in 1998 to provide sophisticated financial advisory and transaction services.

Going to market with credible and reliable financials doesn’t have to be one of them. The buyer negotiates critical price reductions after finding issues in the internal financial statements. However, in the lower middlemarket (company value from $10mm-$250mm), most business owners do not get an audit prepared because of cost.

For example, if the buyer discovers something in diligence that warrants negotiation of enhanced rights and remedies, it may also negotiate for a separate escrow, apart from the standard general indemnity escrow, to ensure funds are available if any of the enhanced remedies are triggered.

Markel specializes in M&A legal issues for middle-market software companies and offers expert insights into the key legal considerations essential for companies entering the M&A arena. Exit Planning Guidance: Getting Your Legal House in Order The consequences of not getting your legal house in order ahead of a sale can be dire.

For example, if the buyer discovers something in diligence that warrants negotiation of enhanced rights and remedies, it may also negotiate for a separate escrow, apart from the standard general indemnity escrow, to ensure funds are available if any of the enhanced remedies are triggered.

As most of the readers know, purchasing power is one of the key drivers of profitably in the industry; adding several hundred locations will only strengthen Mavis’ ability to negotiate pricing and manufacturer programs. Giorgio Andonian is a Managing Director in FOCUS Investment Banking’s Auto Aftermarket Group.

In addition to the general indemnities, the parties to M&A agreements often negotiate separate “stand-alone” indemnities that cover specific topics outside the general indemnities, usually without reference to an underlying breach of the representations, warranties, or covenants.

Transaction parties negotiated expanded or new representations to address the effect of Covid-19 on the target business, as well as the policies and protocols for dealing with those effects. The Covid-19 virus underscored this aspect of M&A practice.

Private equity (PE) groups still have capital to deploy—and strategic acquirers, including large middle-market or public companies, are using their balance sheet s to finance deals. If you receive an unexpected offer to buy your company, you might assume you have a quick, easy deal. The buyer has all the leverage.

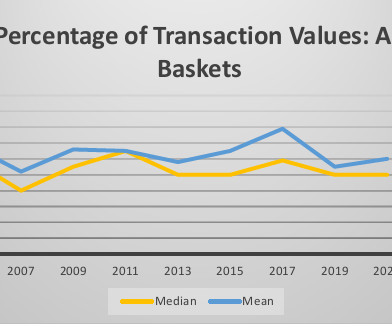

This article examines how buyers and sellers are negotiating indemnity baskets in private company M&A transactions, as shown in the American Bar Association's private target deal points studies. The ABA studies examine purchase agreements of publicly available transactions involving private companies.

We organize all of the trending information in your field so you don't have to. Join 38,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content